As the investment migration industry evolves rapidly, the MENA region is expanding investor-residency and “golden visa” programs as part of broader economic diversification efforts away from oil dependence1. Countries such as Saudi Arabia, alongside Oman and Kuwait, reflect this shift. In doing so, the Gulf is quietly redefining global mobility by using long-term residency, rather than citizenship as a core economic tool, a strategic reorientation this article examines.

The Gulf Cooperation Council (GCC)2 states comprising Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates (UAE) are located on the Persian Gulf with a combined population exceeding 61 million,3 known for their vast oil and natural gas reserves that have historically driven growth and fiscal revenues.

Saudi Arabia, with approximately 35.3 million people, has by far the largest population in the Gulf, while Bahrain, at about 1.6 million, has the smallest.

The Gulf is also increasingly positioned as a global hub for investors, entrepreneurs, and high-net-worth individuals, supported by investor-friendly residence and a favorable tax environment. In recent years, the region has increasingly pursued economic diversification into sectors such as tourism and immigration, finance, logistics, and technology to reorient the economy from its dependence on oil.

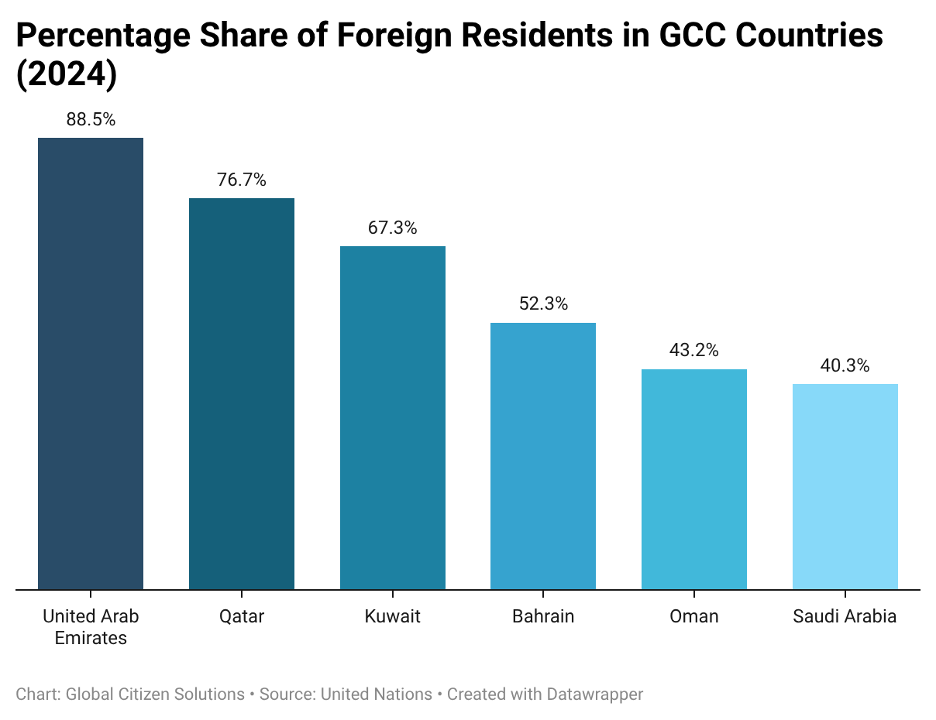

One defining feature of Gulf demographics is the extraordinarily high proportion of foreign-born residents, which ranks as the highest globally. This phenomenon is most pronounced in countries like the UAE, Qatar, and Kuwait. In the UAE alone, foreign residents make up around 88.5% of the population. As a result, these nations exhibit unique social and economic dynamics shaped by their diverse, expatriate-heavy societies.

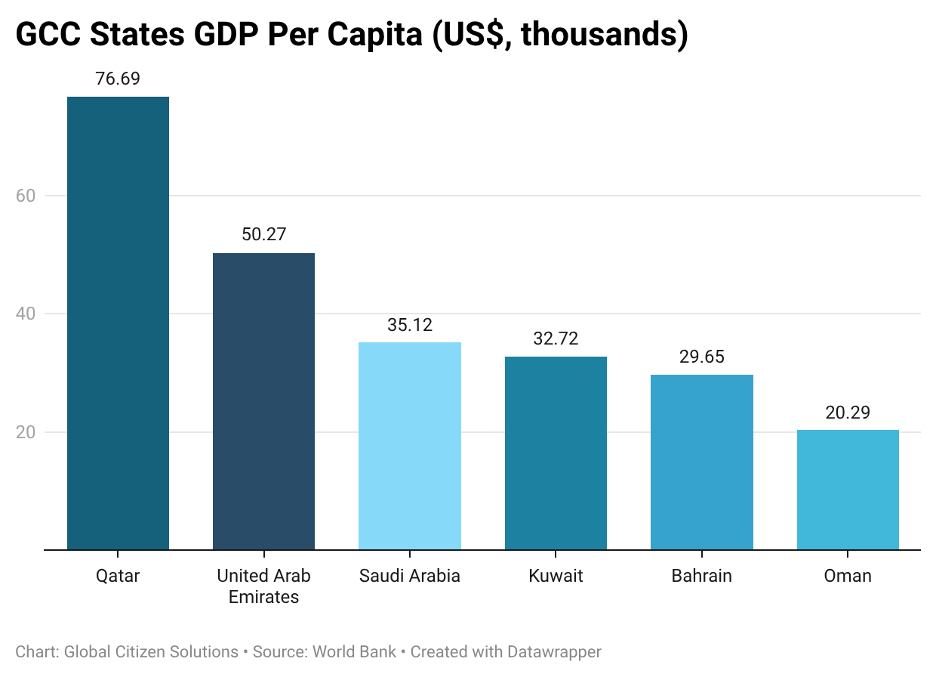

As for economic indicators, according to the World Bank’s Gulf Economic Update, economic growth across the Gulf Cooperation Council (GCC) is expected to strengthen in the medium term, rising to about 3.2% in 2025 and 4.5% in 2026. This acceleration is anticipated as Organization of the Petroleum Exporting Countries (OPEC+) oil production cuts are rolled back and non-oil sectors continue to expand robustly, reflecting both improved oil market conditions and diversification efforts among member states4.

According to the World Bank’s latest Gulf Economic Update5, non-oil sectors are now key drivers of growth, strengthening economic resilience and supporting medium-term expansion despite oil market volatility, supported by national strategies such as Saudi Vision 2030 and similar reform agendas across the region.

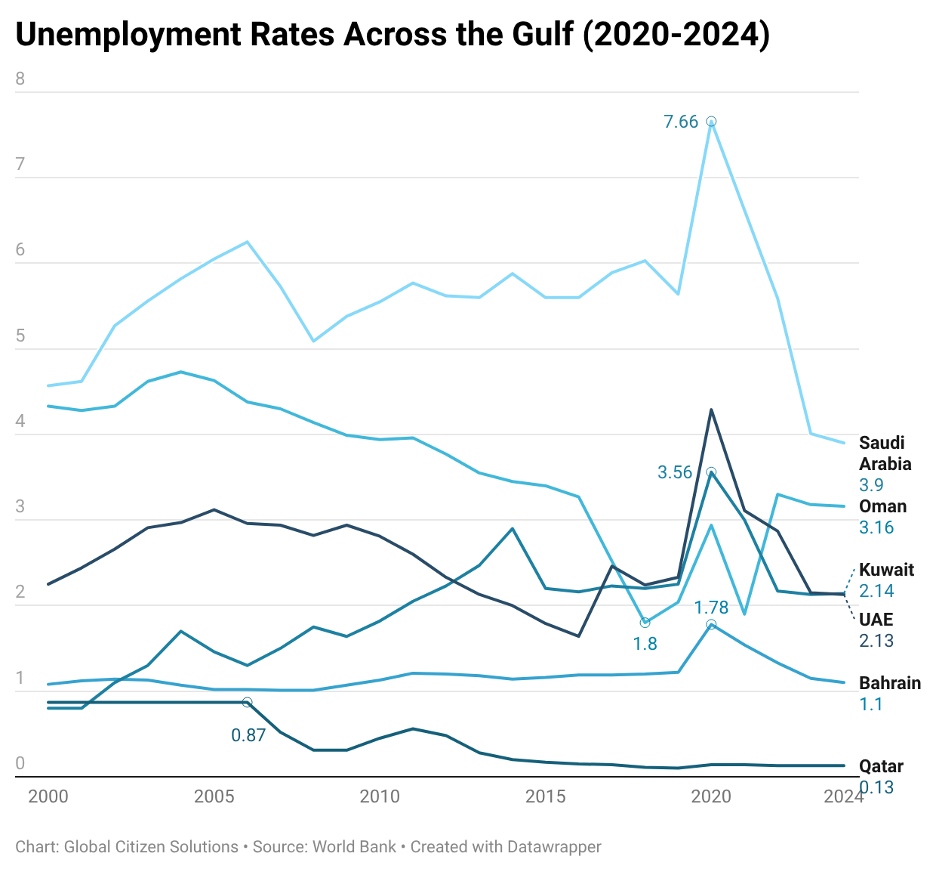

As displayed above, unemployment across Gulf Cooperation Council (GCC) countries has remained consistently low, averaging below 4% between 2000 and 2024, with Qatar typically below 1% due to its expatriate-heavy workforce. Although rates rose temporarily in 2020 amid the COVID-19 shock, they declined quickly and returned to pre-pandemic or lower levels by 2024 as economies recovered and diversification advanced. Compared with global unemployment averages of around 5–6%, GCC unemployment remains significantly lower, reflecting oil wealth and labor market structures.

Despite some of the lowest unemployment rates globally, Gulf Cooperation Council (GCC) economies face acute labor supply constraints driven by small national populations, rapid economic diversification, and rising demand for highly skilled workers. Persistently tight labor markets have consequently increased reliance on foreign talent as a structural input to growth rather than a cyclical adjustment mechanism. This dynamic has led to the expansion of long-term residency, golden visa, and premium residency programs across the region, aimed at attracting and retaining high-value human capital essential for sustaining productivity, innovation, and economic transformation6.

In assessing efforts toward economic diversification and reduced reliance on oil, a key development in recent years has been a growing number of Gulf states that have emerged as new destinations within the investment migration industry. Of particular interest is not only the introduction of new residency programs, but also the continuous adjustments these frameworks undergo as they mature.

What was once a migration system largely defined by short-term, employer-sponsored visas has evolved into a layered landscape of long-term, sponsor-free residency options. Prior to 2019, residency across GCC countries was almost entirely tied to employment and sponsorship, but the UAE’s introduction of the Golden Visa marked a turning point by offering long-term residency to investors and skilled professionals7. Since then, similar programs have emerged across the region.

This evolution reflects a clear strategic shift across the Gulf region: residency is no longer treated merely as a temporary labor instrument, but rather as a policy lever designed to attract capital and most importantly draw talent without extending political membership through eventual citizenship.

Recent scholarly publications situate the rise of residency-by-investment programs in the Gulf within a broader shift in how the region manages migration, rather than viewing them as standalone visa products.8 Governments are increasingly using these programs as part of wider reforms linked to economic diversification, migration management, and evolving relationships between citizens and non-citizens – signaling a more flexible and pragmatic approach to residency policy.

While attracting capital remains an important objective, these programs also mark a move away from the region’s long-standing reliance on strictly temporary labor systems. Citizenship remains tightly controlled, but long-term residency has emerged as a strategic middle ground: a tool to attract talent, investment, and economically active residents without fundamentally reshaping national identity or citizenship frameworks9.

According to migration scholar Noora Lori, investor migration has expanded rapidly in the Gulf in response to several long-standing structural realities. Most non-citizens, regardless of how long they reside in the region, are classified as temporary, with no pathway to permanent status or citizenship. Restrictive nationality laws further limit legal belonging, affecting not only long-term residents but, in some cases, individuals born locally. Against this backdrop, combined with sharp global inequalities in passport strength and travel freedom, demand has grown for alternative forms of legal security10.

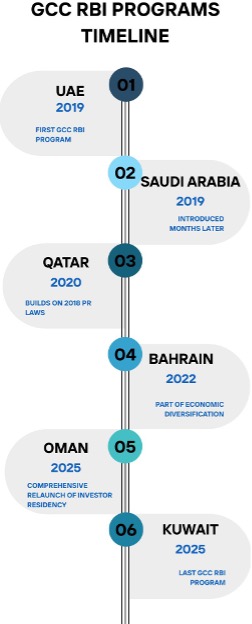

As of today, all six Gulf Cooperation Council (GCC) countries offer residence-by-investment (RBI) options, marking a significant and relatively rapid evolution in regional migration policy.

Notably, all major GCC RBI programs were introduced between 2019 and 2025, highlighting the pace of institutional adoption within a short six-year period.

The UAE set the regional benchmark with its Golden Visa framework, in both policy design and branding, which has since influenced similar initiatives across the Gulf. At their core, these programs are driven by a shared strategic objective: supporting economic diversification away from oil dependence under national transformation agendas such as Vision 2030 and Vision 2040.

Recent policy changes across the Gulf Cooperation Council (GCC) point to a shift away from rigid, high-cost residency-by-investment models toward more competitive and targeted frameworks. Earlier programs tended to rely on high financial thresholds and limited differentiation, whereas newer approaches focus on adjusting price points, expanding eligibility, and tailoring residency options to better support national economic priorities.

Cases:

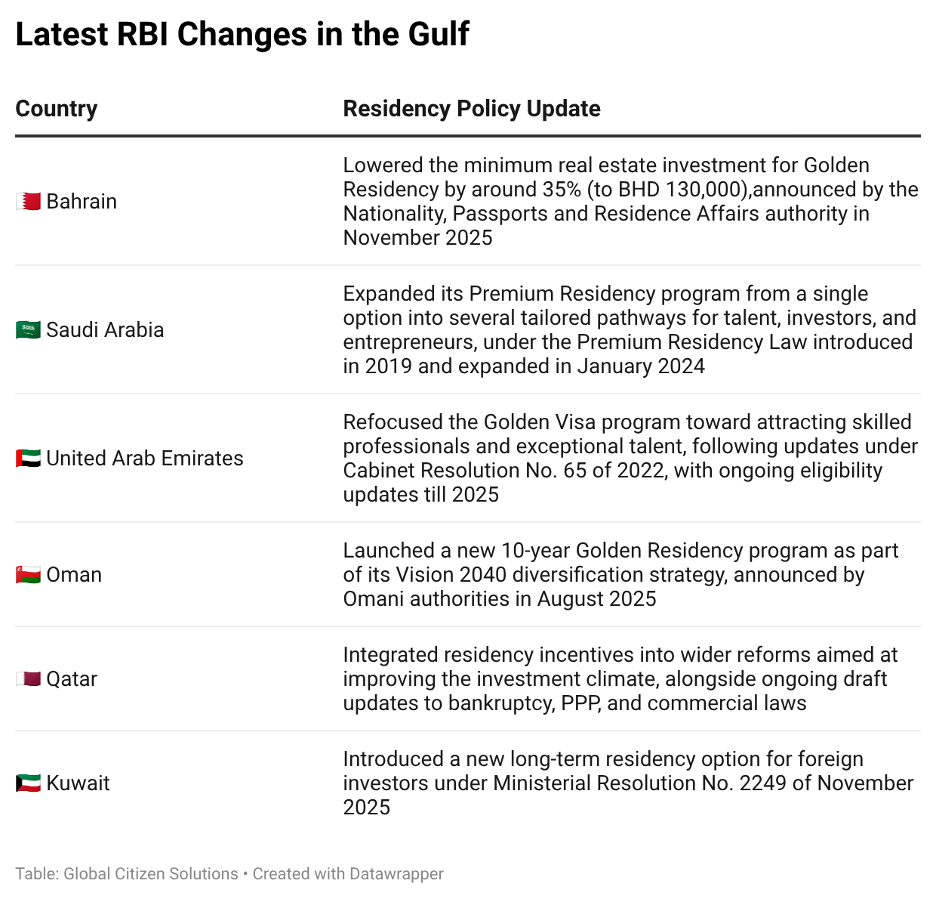

- Bahrain: To start with recent changes, Bahrain is the first notable example. In November 2025, Bahrain adjusted its investment-linked residency framework by reducing the minimum real estate threshold for the Golden Residency Visa from BHD 200,000 to BHD 130,000 (approximately USD 345,000), a reduction of about 35 %11, signaling a strategic shift toward broader eligibility and increased competitiveness within the Gulf’s long-term residency market.

- Saudi Arabia: By contrast, the country has not lowered financial thresholds for permanent residency but has fundamentally reshaped its residency offering. The Premium Residency scheme has evolved from a single “golden visa” concept into a structured portfolio of residency options targeting talent, entrepreneurs, business investors, and real estate owners, each with clearly defined eligibility criteria. This redesign aligns closely with Saudi Arabia’s Vision 2030 agenda, which aims to shift the Kingdom from an oil-dependent economy toward a more diversified and globally competitive investment hub12.

- United Arab Emirates: Between 2024 and 2025, the UAE recalibrated its Golden Visa framework, shifting from a predominantly investment-led model toward a clearer focus on talent attraction. While capital-based pathways remain available, authorities expanded and prioritized eligibility for doctors, PhD holders, scientists, specialized professionals, athletes, creatives, and high-achieving graduates – signaling a stronger emphasis on human capital as a central pillar of long-term residency policy. The strategic aim13 is to support economic projects and foster innovation and entrepreneurship by attracting investors, entrepreneurs, and highly skilled talent, thereby strengthening a sustainable and dynamic business environment. Through long-term, sponsor-free residency options, the UAE seeks to reinforce its position as a global hub for knowledge, investment, and long-term economic growth.

A comparative study of Gulf visa frameworks14 shows that while several states have introduced residency and citizenship pathways primarily targeting wealthy investors, the United Arab Emirates stands out for pairing wealth-based routes with qualification-based residency options. This dual approach broadens the applicant pool to include younger skilled professionals and high-potential talent who may lack significant capital but possess qualifications, expertise, or specialized skills aligned with the UAE’s economic diversification and knowledge-economy objectives.

- Oman: Oman formally launched its 10-year Golden Residency program on 31 August 2025 as part of its broader economic diversification agenda under Vision 204015. The program brings together multiple investment pathways, including real estate, company formation, and capital investment, within a fully digitalized application system, signaling a focus on administrative transparency, efficiency, and regional competitiveness.

- Qatar: Qatar has taken a distinct approach, placing less emphasis on residency thresholds and more on broader legal and institutional reform. As reported by Reuters16, the government is revising key laws on bankruptcy, public–private partnerships, and commercial registration, explicitly linking these changes to its foreign direct investment strategy. Within this framework, residency incentives operate as part of a wider effort to strengthen the overall investment climate, rather than as a standalone policy tool.

- Kuwait: Kuwait was the last country in GCC to introduce a long-term residency pathway for foreign investors in as announced in November 202517. Eligibility is assessed holistically with emphasis on technology transfer, non-oil diversification, export potential, productivity gains, and job creation for Kuwaiti nationals, rather than fixed investment thresholds.

Furthermore, according to a World Economic Forum analysis18, GCC countries are increasingly using long-term residency instruments such as golden licenses and visa residency permits as strategic tools to attract investment and strengthen their competitiveness as they transition toward diversified, non-oil-based economies. The result of these changes is a more competitive, diversified, and strategically integrated residency landscape, where long-term residence is positioned not as an end, but as a tool to attract capital, talent, and economic activity aligned with national development goals.

This approach stands in clear contrast to many European residency programs, which are often implicitly linked to eventual citizenship. In the Gulf, long-term residency is introduced as a sufficient value.

Furthermore, the introduction of the GCC Unified Visa19 (also known as the GCC Grand Tours Visa), anticipated for 2026, is another factor enhancing the attractiveness of Gulf residency programs by establishing the region as a strategic hub facilitating connectivity between Asia, Europe, and Africa for both business and leisure travel.

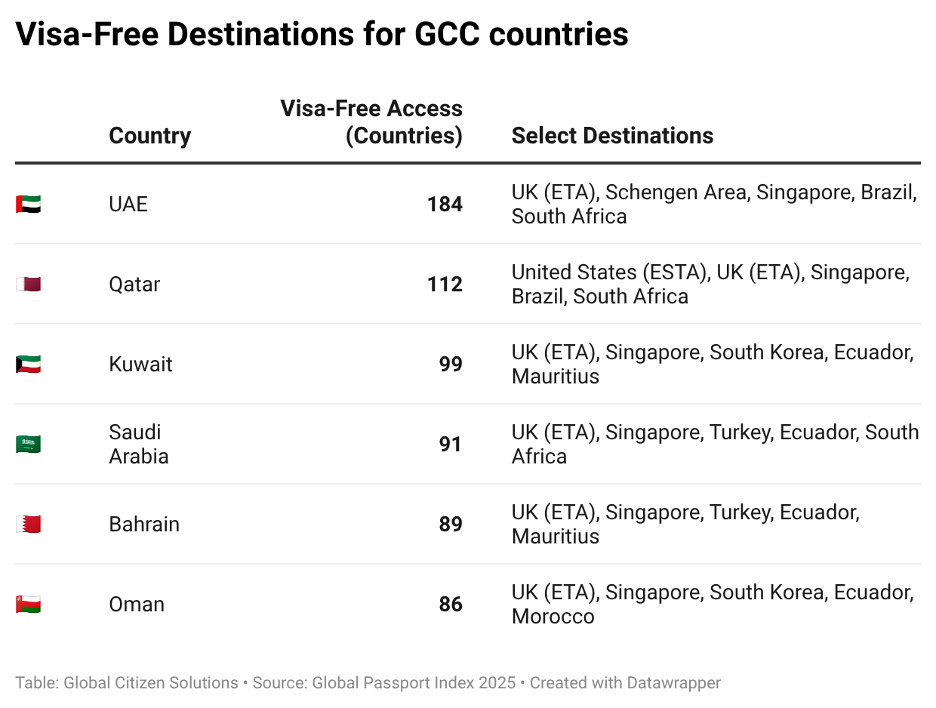

Currently, the UAE offers the highest number of visa-free destinations across the GCC countries.

Across the Gulf, residency-by-investment and long-term residency programs are not designed for a single type of applicant. Typical beneficiaries include real estate investors, for whom property ownership often provides the most standardized and administratively straightforward route; business investors and entrepreneurs, whose eligibility is tied to capital deployment, company formation, or job creation; and high-earning professionals or individuals with specialized skills, reflecting the rise of more merit-based pathways alongside traditional capital-driven models.

In addition, these programs appeal to mobile families and long-term regional expatriates seeking greater stability, access to education, and improved quality-of-life outcomes through permanent or semi-permanent residence.

- United Arab Emirates (UAE) – The UAE is most suitable for HNWIs, entrepreneurs, business owners, and highly mobile professionals, reflecting the breadth and flexibility of its Golden Visa structure. Multiple qualifying routes across capital investment, innovation, and talent indicate a framework capable of accommodating both financial investment and human capital. As a result, the UAE is particularly attractive to investors seeking long-term residency combined with regional and global mobility.

- Saudi Arabia – Saudi Arabia is best aligned with large-scale investors, strategic entrepreneurs, and corporate investors with long-term operational objectives. Higher capital thresholds and employment-linked criteria point toward a preference for investment associated with structural economic activity. Consequently, the program is less oriented toward passive or highly mobile investors and more toward anchored, growth-driven profiles.

- Qatar – Qatar is particularly suitable for HNWIs, real estate investors, and international families seeking residency with the lowest financial entry point in the Gulf. The availability of both renewable residency and permanent status reflects a system oriented toward stability and permanence. It therefore appeals to investors prioritizing security, clarity, and long-term presence over active business expansion.

- Bahrain – Bahrain is well suited for mobile HNWIs, retirees, and professionals seeking long-term residency with minimal financial commitment. The low investment threshold and absence of strict stay requirements indicate a residency model emphasizing flexibility and accessibility. This makes Bahrain attractive to investors focused on lifestyle positioning rather than scale.

- Oman – Oman is most appropriate for long-term investors, family-based HNWIs, and entrepreneurs with a preference for measured, sustainable engagement. The structure and duration of its residency options imply an emphasis on continuity and economic substance. It is therefore well aligned with investors seeking stability and gradual integration.

- Kuwait – Kuwait is primarily suitable for strategic investors and corporate entities operating within approved sectors. The project-based nature of its investment pathways and sector-specific incentives suggest a selective and targeted residency framework. This positions Kuwait as less relevant for lifestyle-driven investors and more appropriate for commercially focused profiles.

For a tech entrepreneur from India, Qatar’s USD 200,000 (approximately) residency pathway offers a tax-efficient regional base closer to home, with direct access to Gulf markets and fast-growing Asia–Africa trade corridors.

In the United Arab Emirates, demand for long-term residency has surged in recent years. Dubai’s General Directorate of Residency and Foreigners Affairs (GDRFA) issued 158,000 Golden Visas in 2023, nearly double the number granted in 2022 and more than three times the total issued in 202120. The sharp increase reflects the UAE’s expanding focus on long-term residence for investors, professionals, and skilled talent.

Saudi Arabia has also seen strong uptake following changes to its Premium Residency program. Between January 2024 and July 2025, the scheme received more than 40,000 applications21. The growth followed a major reform in early 2024 that introduced multiple residency tracks and, for the first time, opened long-term residency options to foreign real estate and business investors, with around 8,000 approvals granted in 2024.

It is also important to note that demand does not come exclusively from foreign nationals. Local long-term residents also apply for these programs, often seeking a legal status that navigates restrictive citizenship frameworks and mitigates the political uncertainty associated with temporary migration regimes. However, another interesting observation in this context are the case studies showing that long-term Gulf residents from countries such as Lebanon, Iran, and Yemen have increasingly turned to citizenship-by-investment programs in other jurisdictions to secure alternative passports that allow them to maintain residence and employment in GCC states amid more restrictive citizenship frameworks22. We can suggest that demand for Caribbean citizenship is growing, including among individuals residing in the Gulf, who increasingly use it as a tool for global mobility and flexible residence.

For these individuals, external citizenship functions as a stabilizing mechanism that complements GCC residency rather than replacing it. These dynamics underscores the growing strategic value of the investment programs, illustrating how it enables lawful mobility within evolving Gulf residency systems while creating new pathways for economic and personal security.

Across the Gulf, long-term residency is increasingly positioned not simply as a mobility right, but as a form of platform access, providing entry to markets, infrastructure, lifestyle, and regional connectivity. What ultimately distinguishes the Gulf model is its clear separation between residency and citizenship. Long-term residence is framed as sufficient value in itself, rather than as a stepping stone to nationality.

At the same time, long-term residence in the Gulf is emerging as a strategic Plan B and regional base for globally mobile individuals and families. Its geographic position between Europe, Asia, and Africa, favorable time zones, and, in some cases, attractive tax environments (with appropriate structuring) make Gulf residency a practical anchor for international business and personal mobility.

In this context, demand for investment migration does not arise solely from new foreign investors. Long-term residents in the region are increasingly engaging with residence by investment frameworks to navigate existing less flexible citizenship laws and reduce uncertainty linked to temporary migration systems. Evidence shows that individuals from countries such as Lebanon, Iran, and Yemen have turned to citizenship-by-investment programs in other jurisdictions, particularly in the Caribbean, to secure alternative passports that support continued residence, employment, and mobility within the GCC. For these individuals, external citizenship functions as a stabilizing complement rather than a substitute for Gulf residency, highlighting the strategic role of investment migration within the region’s evolving mobility landscape.

Another notable observation is that rather than relying on a single, standardized “golden visa,” Gulf countries are increasingly segmenting residency offerings by applicant profile, including real estate investors, business owners, entrepreneurs, high-earning professionals, and financially independent individuals. Pricing structures, eligibility criteria, and residency durations are continuously refined to reflect national priorities.

Finally, the evolution of Gulf residency programs reflects a broader shift in objectives. The focus is no longer solely on attracting capital, but increasingly on attracting talent. Equally important, the emphasis has moved away from citizenship as the primary marker of value toward residency and the benefits that accompany it. This signals a more open and flexible residency policy framework, situating investment migration within a wider transformation in how the region manages mobility, economic growth, and long-term residence.