The acquisition of holiday homes among high-net-worth individuals (HNWIs) represents one of the most visible intersections of wealth, mobility, and lifestyle preference in contemporary real estate markets. As private wealth has expanded globally, second-home ownership has evolved from a marker of affluence into a deliberate, multi-functional asset decision, which is shaped by location desirability, ownership conditions, and the broader life priorities of a globally mobile ownership class.

This briefing examines the most desirable locations for HNWIs to buy holiday homes. To do so, it constructs a comparative index across 20 well-known markets worldwide, evaluating each against three pillars: Prime Property, Lifestyle & Desirability, and Accessibility. A key distinction of this framework lies in its deliberate emphasis on lifestyle-led indicators over purely financial metrics, reflecting how second homes are experienced.

The analysis also engages the motivational dimension of acquisition, introducing four buyer typologies grounded in behavioral and economic literature. Together, the index and the typologies offer a dual lens: one quantitative and one behavioral, designed for globally mobile investors evaluating prime residential markets across investment performance, lifestyle quality, and accessibility.

The result is a practical decision-making tool: a ranked shortlist of the world’s most compelling holiday-home markets, structured to help HNWIs identify where their capital, lifestyle priorities, and ownership conditions align most effectively.

A High-Net-Worth Individual (HNWI) is typically defined in financial and economic literature as a person who holds investable (or liquid) assets valued at US$1 million or more, excluding the value of their primary residence, collectibles, consumer durables, and other illiquid or personal-use assets (Capgemini, 2024).

As of 2026, second-home ownership represented 28% of global luxury property transactions. Regional variation was limited, although proportions were higher in Asia (34%) and the Caribbean (33%), with more pronounced patterns observed in specific local markets. Additionally, international demand remains substantial, with 82% of agents reporting sales to foreign buyers, particularly in Africa/Middle East, Europe, and the Caribbean (Sotheby’s International Realty, 2026).

HNWI motivations for second-home ownership are not monolithic. They are multi-layered, including financial strategy, family utility, and personal wellbeing. Moreover, in practice, these rationales frequently overlap and reinforce one another.

- Wellbeing & Lifestyle – Second homes occupy a distinctive position in the literature on elite consumption. On one hand, architect-designed, amenity-rich properties in high-desirability locations operate as markers of social distinction, communicating wealth, taste, and elite identity through both overt display and the subtler registers of materials, views, and design (Hjalager et al., 2023; Walters & Carr, 2019). On the other hand, owners consistently frame these same properties as spaces of escape, ease, and continuity. Environments where the pressures of professional life recede and shared domestic routines generate accumulated layers of memory, belonging, and family identity (Walters & Carr, 2019). This duality is well-documented: second homes simultaneously function as vehicles of multi-property investment and as privately narrated worlds of emotional security and intimacy (Paris, 2009).

Apart from academic evidence, The Julius Baer Global Wealth and Lifestyle Report (2024) notes that more than half of HNWIs plan to increase leisure travel and continue to spend on experiences such as fine dining and luxury hospitality, while remaining willing to “spend on and invest in their lifestyles, families, and futures.” This is consistent with findings from Savills (2025), which identify lifestyle appeal as a key factor in residential decision-making. Together, this evidence suggests that lifestyle consumption is one of core components of wealth allocation, supporting its inclusion as a key analytical indicator.

- Financial – For HNWIs, holiday home acquisition operates across several distinct but overlapping financial logics. As a tangible hard asset, residential real estate has demonstrated consistent inflation-hedging properties: Fehrle (2023) finds that housing at least partially hedges against inflation over 1, 5, and 10-year horizons, and hedges perfectly in the long run during the post-war period – performing at least as well as, and in most periods better than, equity as an inflation shield.

Beyond individual asset performance, the geographic diversification logic is also well-supported: analyzing direct real estate markets across 16 OECD countries from 1999 to 2018, Candelon et al. (2021) find that international diversification in real estate portfolios generally dominates sectoral diversification as a risk-reduction strategy. This claim is positioning cross-border holiday home acquisition as a rational portfolio decision rather than a purely lifestyle one.

- Legacy & Family – Financial and family rationales are deeply intertwined for HNWIs, and real estate sits at the center of both. Drawing on interviews with first-generation ultra-wealthy parents and their wealth managers, Higgins (2022) documents how these families construct strategies to manage intergenerational transfers of wealth – treating the controlled handover of assets as a deliberate dynastic project. Within this context, real property occupies a prominent position as a preferred vehicle for intergenerational transfer. Moreover, the Coldwell Banker Global Luxury 2026 Trend Report, drawing on three years of luxury sales data and global wealth research, finds that Gen X and Millennials are set to be the two largest cohorts to inherit USD 4.6 trillion in global real estate wealth over the next decade, with the United States expected to capture 52% of that property transfer. A holiday home in a well-chosen jurisdiction thus functions simultaneously as a family gathering asset, an intergenerational holding, and a wealth-preservation instrument.

This briefing identifies the most attractive destinations globally for HNWIs to own holiday homes, combining real estate fundamentals with a strong lifestyle-driven lens. Unlike traditional property rankings focused on pricing or returns, the framework is built around how second homes are actually used, prioritizing experience, usability, and ecosystem quality alongside ownership conditions.

The dataset covers 20 countries, selected to reflect geographic and market diversity. The 20-market sample includes established HNWI demand corridors. European markets are proportionally represented in the sample, since that is where documented HNWI second-home activity is concentrated. Thus, their subsequent dominance in the ranking reflects this real-world demand pattern rather than a structural bias in market selection.

Each country is represented by its flagship luxury holiday-home market, ensuring the analysis reflects prime second-home destinations rather than national averages. Market-level variables, such as climate, infrastructure, and connectivity, are assessed at the destination level, while institutional factors, including quality of life, safety, ownership regulations, and tax environment, are assessed nationally.

Index Structure

The model is structured around three pillars, each weighted to reflect its relative role in HNWI second-home decision-making:

The deliberate emphasis on Lifestyle & Desirability reflects a central premise of this briefing: that for HNWIs, the lived experience of a second home is at least as important as its financial profile.

Pillar Detail

Prime Property (40%) captures investability and ownership conditions through four indicators: prime property price per sqm (scored inversely to reward accessibility), annual market appreciation, the ownership tax environment (assessed on structure and effective burden, with lighter regimes scoring more favorably), and foreign ownership ease (across ownership rights, transaction complexity, and property-linked migration pathways).

Lifestyle & Desirability (45%) captures the experiential dimension of each destination, combining quality of life (GCS Global Quality of Life Index), safety (Global Peace Index, inverted), annual sunshine hours (Global Climate Normals Database), and a composite luxury infrastructure score, reflecting Michelin-starred dining, superyacht marina capacity, luxury hospitality presence, and world-class leisure offerings.

Quality of life and luxury infrastructure carry greater weight; safety and sunshine act as supporting differentiators.

Accessibility (15%) is measured through total annual passenger traffic at the primary international airport, an indicator of route density, connection frequency, and ease of reach.

Scoring & Aggregation

All continuous indicators are normalized using min–max normalization prior to aggregation, ensuring comparability across different units and scales. Following pillar aggregation, a geopolitical risk adjustment is applied as a multiplicative overlay to each country’s weighted score. This captures risks not fully reflected in standard indicators, including proximity to active conflict zones and broader regional instability. It combines a country-level assessment with a regional exposure component to produce a final risk factor between 0 and 1. Geopolitical risk scores are sourced from Global Guardian’s Global Risk Map 2026.

Limitations

Some limitations that should be noted are that the destinations without Michelin Guide coverage may be understated on luxury infrastructure despite strong local offerings. Moreover, the geopolitical adjustment involves a degree of qualitative judgement and should be interpreted as directional. Finally, pricing and appreciation data are time-sensitive and may shift in dynamic markets.

Overall, market dynamics are better understandable in the context of people buying them. Before ranking, it is worth understanding who that buyer is, and why.

The use of behavioral typologies helps capture the diverse motivations of HNWIs. As described in the literature above, property decisions among HNWIs are shaped by a range of motivations that go beyond financial considerations, including status, lifestyle, investment strategy, and family legacy. The typologies were developed by synthesizing these recurring patterns identified across the literature, grouping them into distinct but overlapping behavioral profiles. While not mutually exclusive, they reflect common ways in which HNWIs approach property acquisition. As such, these typologies provide a useful framework to explain why different indicators, particularly lifestyle and desirability, are relevant and how they influence the evaluation and weighting within the index.

The Conspicuous Investor: Property acquisition oriented toward social distinction, peer signaling, and the communication of elite taste and status. This profile is grounded in Veblen’s theory of conspicuous consumption, as well as housing studies literature (Hjalager et al., 2023; Walters & Carr, 2019).

The Patrimonial Buyer: Property acquisition shaped by intergenerational wealth transfer, family continuity, and the establishment of a durable legacy asset. This perspective draws on Higgins (2022) and the broader literature on dynastic wealth.

The Amenity Migrant: Property acquisition motivated by lifestyle enhancement, access to natural amenities, and the pursuit of wellness-oriented, restorative environments beyond the primary urban residence. The concept of amenity migration was introduced by Laurence A.G. Moss (1994) and further developed in subsequent work. It refers to the relocation of individuals to areas perceived to offer superior environmental quality and distinct cultural attributes.

The Portfolio Allocator: Property acquisition guided by financial considerations, including capital preservation, inflation hedging, income generation, and cross-border diversification. This approach is informed by Fehrle (2023) and Candelon et al. (2021).

These behavioral profiles provide a conceptual lens through which the weighting of indicators, particularly the emphasis on lifestyle and usability, can be interpreted. Each of these profiles map differently onto the index pillars, shaping how destinations are evaluated in practice.

The ten markets that follow, represent the strongest overall performers across the index. The resulting ranking serves as a measure of overall destination attractiveness for second-home ownership, not as a pure investment performance index. Higher-ranked markets reflect a stronger balance across lifestyle quality, ownership conditions, and accessibility, rather than dominance in any single dimension.

This matters for interpretation. Individual markets may outperform meaningfully on specific variables, such as capital appreciation, tax efficiency, or lifestyle depth, even where their composite score places them lower in the ranking. Thus, the index is best used as a directional tool for identifying well-rounded destinations, where lifestyle quality, ownership conditions, and accessibility align most effectively.

Table 1. Top 10 Markets for Holiday Home Acquisition with Scores

01/ Spain

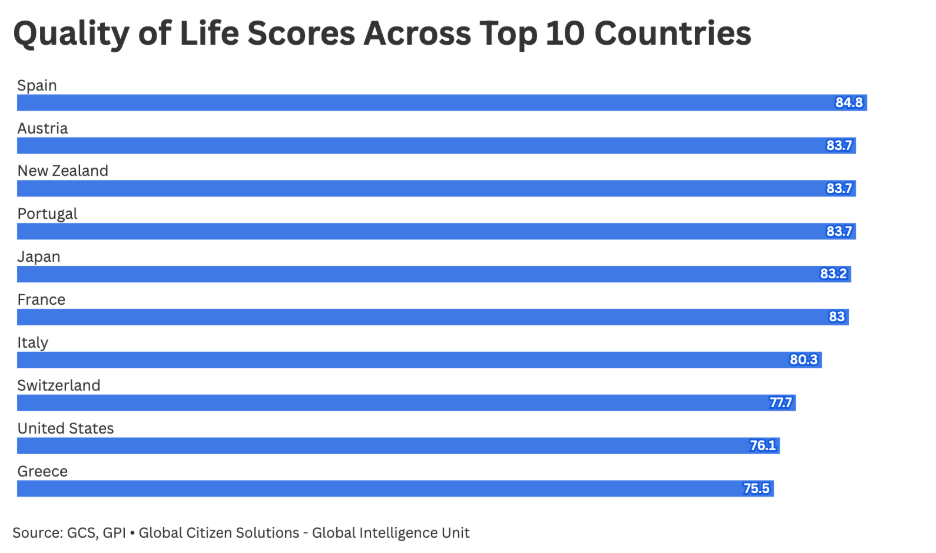

Mallorca / Ibiza: Spain ranks first through a combination of factors, among them strong price growth (12.5%), the highest quality of life score in the dataset, generous sunshine (2,789 hours per year), deep luxury infrastructure, and a market large enough to absorb serious capital without losing its character.

What the numbers do not fully capture is that the two islands serve meaningfully different buyers. Ibiza draws a globally connected ownership class for whom the social ecosystem is of vital importance. Mallorca has quietly matured into something else – a market of considered permanence and long-season residency, where buyers increasingly prioritize quality of tenure over seasonal intensity.

When it comes to general property purchases, Madrid stands out as one of Spain’s top cities in terms of demand, with a median listing price of €603,784. In the luxury segment, international buyers play a dominant role, accounting for over 70% of transactions nationwide and exceeding 80% in prime coastal and island locations (Idealista, 2026).

Primary archetype: Amenity Migrant, with strong secondary appeal to the Portfolio Allocator.

Notable observation from the dataset: Spain combines the second-highest market appreciation rate (12.5%) in the top 10 with the highest quality of life score (84.8) in the entire dataset (as displayed in Chart 1) – the only market where those two variables converge at that level.

Chart 1. Quality of Life Indicators of Top 10 Countries

02/ Portugal

Algarve: Portugal follows closely, and its proximity to the top position is itself the finding, as the Algarve is not regarded as a famous luxury market. It earns its ranking through consistency: the highest appreciation rate in the dataset (17.7%), strong safety, over 3,100 sunshine hours, and entry pricing that remains accessible relative to its performance profile. As noted by the National Statistics Institute of Portugal (INE), the Algarve accounted for 29.9% of all housing purchases by non-resident buyers in Portugal in 2023, highlighting its position as the country’s primary destination for international demand.

The current Golden Visa framework no longer grants a direct property-linked residency pathway, but the underlying appeal is structurally intact. The region has diversified into a year-round residency market, attracting a more internationally diverse ownership class and a corresponding investment in hospitality and infrastructure. For a buyer whose primary question is where returns, climate, and ownership conditions align most efficiently, the Algarve remains a difficult market to argue against.

Primary archetype: Portfolio Allocator, with strong secondary appeal to the Amenity Migrant.

Notable observation from the dataset: At 17.7%, the Algarve records the highest annual appreciation rate in the dataset, sustained alongside top-quartile safety and quality of life scores, no other market in the top 10 combines growth of that magnitude with institutional stability of that quality.

03/ France

Côte d’Azur / St-Tropez: France ranks third, and the gap between its cultural primacy and its index position is analytically meaningful. The Côte d’Azur achieves the maximum luxury infrastructure score in the dataset and serves over 70 million air passengers annually – infrastructure depth that takes generations to accumulate. Its global recognizability as a second-home address is essentially uncontested.

The constraints are largely structural, with high entry pricing, relatively modest recent appreciation (~1.1%), and a comparatively robust tax environment. France has traditionally been supported by strong demand rather than purely return-driven dynamics, a distinction that becomes more visible when usability is considered alongside prestige.

Primary archetype: Conspicuous Investor, with secondary appeal to the Patrimonial Buyer.

Notable observation from the dataset: France is the only market in the top 10 to achieve the maximum luxury infrastructure score.

04/ Italy

Lake Como / Costa Smeralda: Italy ranks fourth, reflecting its long-standing appeal. Prime pricing at around €10,000 per sqm remains below levels seen in France or Switzerland, despite the market occupying a comparable position in the global prestige hierarchy.

The two flagships serve the proposition differently. Lake Como offers contemplations – long vistas, historic palazzi, a residential culture built around return rather than arrival. Costa Smeralda is more socially charged: one of the Mediterranean’s most established luxury coastal ecosystems, defined by its marina infrastructure and the density of its international ownership network. Together they give Italy a dual lifestyle register that few markets can match.

Primary archetype: Patrimonial Buyer, with secondary appeal to the Conspicuous Investor.

Notable observation from the dataset: At €10,000 per sqm, Italy prices at less than a third of Monaco’s entry point and less than half of France’s – for a market that competes directly with both on cultural prestige and global name recognition.

05/ Japan

Niseko: Japan ranks fifth through a combination of factors that don’t map neatly onto the conventional holiday-home playbook. Niseko is not a sun destination or a heritage cultural market. It rather offers a world-class alpine environment with high institutional quality, strong safety, and an ownership profile that has become genuinely international over the past two decades. Academic research has documented a dramatic increase in foreign investment and ownership activity, underpinning what is widely referred to as the Niseko boom – a structural transformation driven by foreign direct investment rather than domestic demand growth (Staples, 2014).

Limited sunshine hours and a relatively concentrated luxury infrastructure beyond ski and hospitality may be considerations for some buyers. At the same time, as the only Asia-Pacific market in the ranking, it offers a distinct layer of geographic and regulatory diversification.

Primary archetype: Portfolio Allocator, with secondary relevance for the Amenity Migrant.

Notable observation from the dataset: Japan has the second-highest air connectivity score in the entire dataset.

06/ United States

Aspen / Palm Beach / Hamptons: The United States ranks sixth, supported by a strength few other markets can match: connectivity: with around 108 million annual passengers.

Factors moderating its position are more structural in nature. Safety metrics rank lower relative to other examined countries, reflecting broader national dynamics rather than location-specific conditions, while entry pricing, at approximately €45,300 per sqm (which is the median of three markets presented), is at the upper end of the ranking. Overall, the U.S. combines exceptional accessibility and market depth with somewhat less favorable conditions from a holding efficiency perspective.

Primary archetype: Portfolio Allocator, with secondary appeal to the Conspicuous Investor.

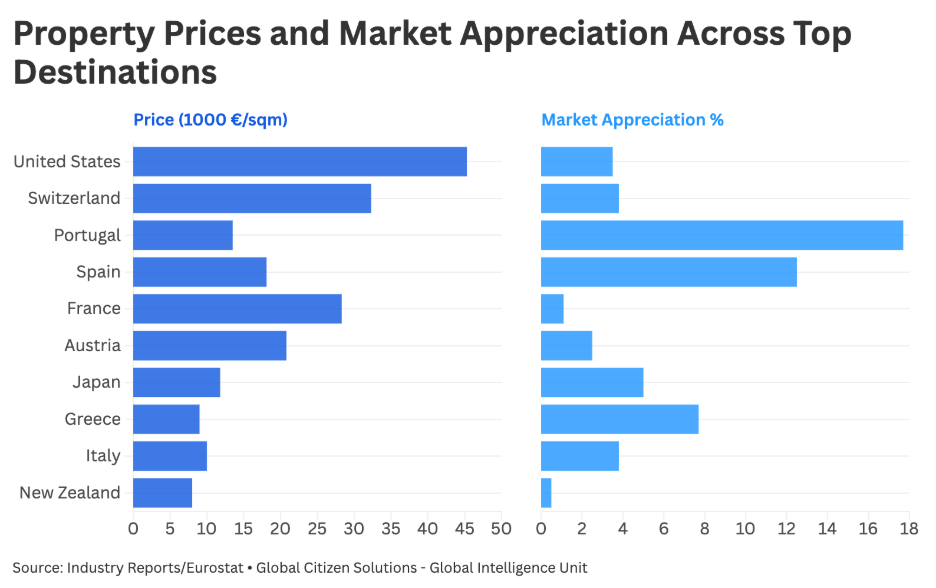

Notable observation from the dataset: The United States holds the highest air connectivity score in the ranking by a considerable margin – yet simultaneously records the highest entry price point in the top 10, producing the widest gap between accessibility and affordability of any market assessed, as also shown in Chart 2 below.

Chart 2. Property Prices and Market Appreciation Rates Comparison Across Top 10 Markets

07/ New Zealand

Queenstown: New Zealand ranks seventh as the index’s clearest retreat market, combining the highest safety score in the ranking with strong quality of life and relatively accessible pricing at around €8,000 per sqm. Its value proposition is grounded in institutional stability rather than return-driven dynamics or infrastructure density. Queenstown, in particular, has seen rising activity from high-net-worth international buyers, especially in the luxury segment, with foreign demand strengthening following recent policy changes and the amendments of Active Investor Plus Visa (New Zealand Herald, 2026).

Certain structural characteristics shape the market, including more moderate appreciation, lower sunshine levels, restrictions on foreign ownership, and relatively limited connectivity compared to other destinations in the ranking. However, these factors are closely tied to its positioning. For buyers seeking long-term stability and a high-quality living environment, Queenstown offers a distinct and differentiated proposition within the global landscape.

Primary archetype: Amenity Migrant, with secondary relevance for the Patrimonial Buyer.

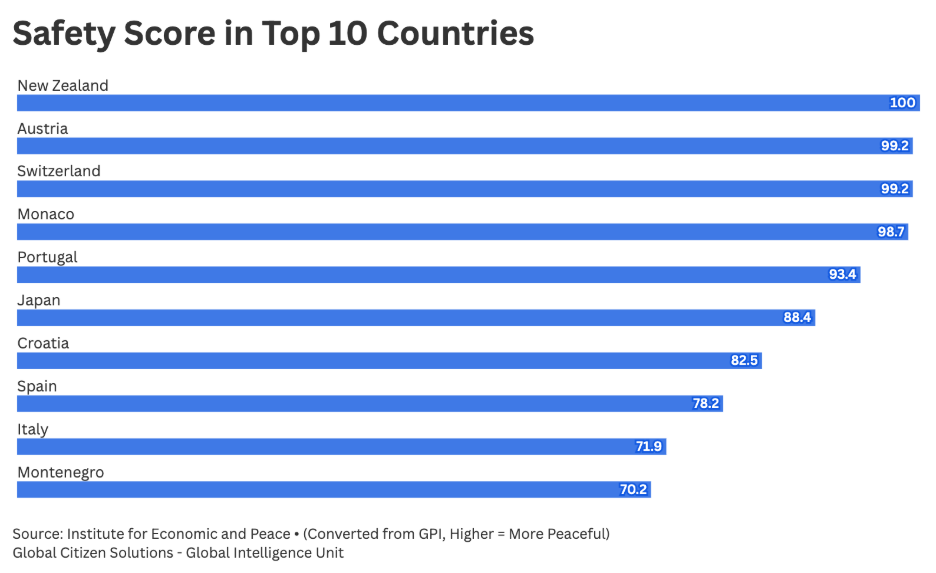

Notable observation from the dataset: New Zealand is the only market in the ranking to achieve the maximum safety score, and the only top 10 market where this level of safety is combined with sub-1% annual appreciation, reinforcing its positioning as a pure retreat profile.

Chart 3. Safety Indicators Across Top 10 Markets

08/ Austria

Kitzbühel / Lech: Austria ranks eighth as the index’s clearest stability play, underpinned by near-maximum safety and consistently high quality of life.

Kitzbühel and Lech stand among Europe’s most established alpine markets, with prime pricing in the €18,000-€23,000 per sqm range supported by tightly controlled supply and sustained international demand. Their appeal lies in long-term ownership stability, where limited inventory and multi-generational holding patterns reinforce value preservation over time.

Primary archetype: Amenity Migrant and Patrimonial Buyer.

Notable observation from the dataset: Austria’s safety score of 99% is joint-highest in the ranking alongside Switzerland, but unlike Switzerland, it carries a materially lighter foreign ownership restriction, making it the more accessible of the two top-tier alpine safety markets.

09/ Greece

Mykonos: Greece ranks ninth, supported by a climate proposition that is unmatched within the ranking. With 3,637 annual sunshine hours, Mykonos offers more usable outdoor time than any other destination assessed, a factor that meaningfully enhances the second-home experience. This is complemented by solid market appreciation at 7.7%, accessible pricing at around €9,000 per sqm, and a notably open environment for foreign ownership.

The market’s characteristics are distinct. Luxury infrastructure remains more concentrated around hospitality and marina offerings with moderate connectivity. Mykonos is best understood as a high-intensity seasonal destination, where the strength of the summer proposition, the combination of climate, lifestyle, and maritime access forms the core of its appeal.

Primary archetype: Amenity Migrant, with secondary appeal to the Conspicuous Investor.

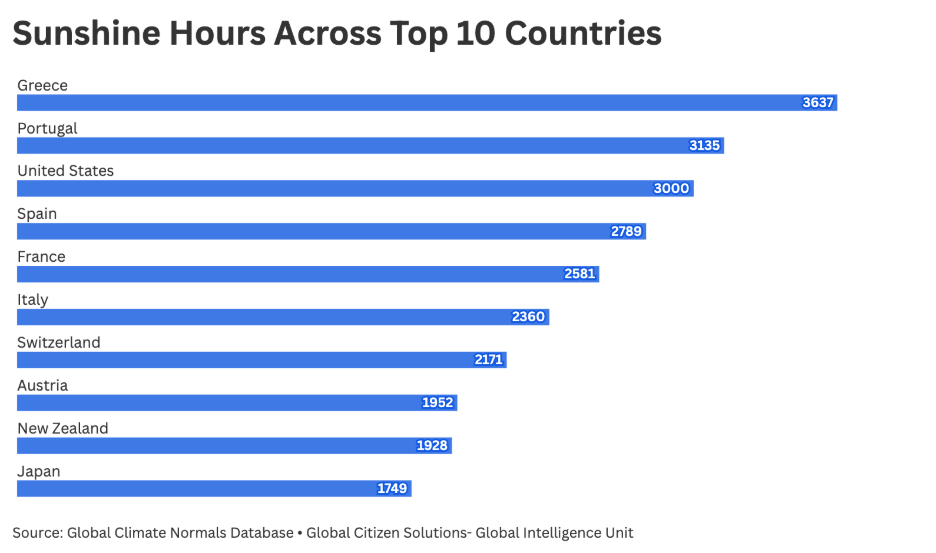

Notable observation from the dataset: At 3,637 annual sunshine hours, Mykonos records the highest solar exposure in the ranking, roughly the equivalent of an additional month of full sunshine per year relative to the top 10 average, presented below in Chart 4.

Chart 4. Sunshine Hours of Top 10 Countries

10/ Switzerland

Verbier / St. Moritz: Switzerland completes the top 10 as one of the most structurally constrained yet fundamentally strong markets. Its core fundamentals are exceptional, with near-maximum safety, high quality of life, stable appreciation, and flagship destinations such as Verbier and St. Moritz that hold enduring global prestige.

Access conditions are more selective, shaped by deliberate policy frameworks that limit foreign ownership and contribute to a tightly controlled supply environment. This, alongside high entry pricing and more limited sunshine, defines the market’s positioning. For buyers able to navigate these constraints, Switzerland offers a highly secure and prestige-driven long-term holding environment.

Primary archetype: Patrimonial Buyer.

Notable observation from the dataset: Switzerland pairs the joint-highest safety score in the ranking with the most restrictive foreign ownership framework in the Western European cohort – the sharpest tension between quality of holding conditions and ease of access of any market assessed.

A few additional markets in top 10 countries to consider, beyond those covered in this briefing, include Comporta in Portugal, Montenegro’s Bay of Kotor, and emerging resort areas in Japan’s Hokkaido. Comporta is gaining traction as a low-density alternative to the Algarve, valued for its preserved landscape and proximity to Lisbon. The Bay of Kotor offers an increasingly attractive framework for international buyers, supported by its strategic positioning and evolving market structure. Meanwhile, Japan’s expanding resort corridors beyond Niseko present opportunities for geographic diversification, with entry pricing that remains relatively accessible.

This briefing explored the global landscape of holiday home acquisition among high-net-worth individuals through a dual lens: the motivational frameworks that drive purchase decisions, and the market and lifestyle attributes that make certain destinations consistently compelling. Using a three-pillar index: Prime Property, Lifestyle & Desirability, and Accessibility, applied across 20 markets globally, a top 10 emerged that is, notably, overwhelmingly European in composition.

Seven of the top ten markets are located in Europe, a concentration that is not incidental. It reflects a structural alignment between the continent’s comparative advantages, being a mature luxury infrastructure, favorable climate corridors, strong institutional quality, and relatively open ownership environments. The two non-European entries, Japan and New Zealand, each occupy distinct niches: Niseko as a high-quality alpine and portfolio diversification destination, and Queenstown as the index’s clearest retreat proposition, defined by exceptional safety and institutional stability rather than return-driven or prestige dynamics.

The ranking confirms a straightforward but often underappreciated truth: the most attractive holiday-home markets for HNWIs are not those that lead on any single dimension, but those where lifestyle quality, ease of ownership, and investment logic reinforce one another. Spain and Portugal illustrate this convergence most clearly, while France and Italy demonstrate an alternative pathway, where prestige attributes sustain demand even where appreciation is more modest or entry pricing is elevated.

A divide also emerges between two broad market archetypes. Southern European markets – led by Spain, Portugal, and Greece, offer higher growth, greater sunshine, and more intensive seasonal usability. Alpine markets, particularly Austria and Switzerland, orient toward long-term stability, multi-generational holding patterns, and tightly controlled supply environments. These are not competing propositions so much as distinct expressions of what a second home is for: one cluster optimizes for experience, the other for permanence.

The briefing also engages a dimension of HNWI behavior that real estate analysis frequently underweights: the role of lifestyle not merely as a preference, but as a primary acquisition rationale. To that end, four buyer typologies are introduced – the Conspicuous Investor, the Patrimonial Buyer, the Portfolio Allocator, and the Amenity Migrant, each grounded in behavioral and economic literature. Among these, the Amenity Migrant is perhaps the most analytically interesting, and the most underrepresented in conventional property discourse.

This profile captures buyers for whom the second home is fundamentally a quality-of-life asset: a vehicle for accessing natural environments, restorative settings, and a pace of living that the primary residence cannot provide. Destinations that score highly on quality of life, safety, and climate – Spain, Portugal, New Zealand, Greece, map directly onto this profile. The Amenity Migrant is not indifferent to financial considerations, but those considerations are secondary to the lived experience of the asset.

Looking ahead, as HNWIs increasingly optimize not just for returns but for time, wellbeing, and optionality, the most competitive holiday-home markets will be those that function seamlessly as both lifestyle assets and strategic capital allocations.

References (in text order)

Capgemini. (2024). World Wealth Report 2024. Capgemini Research Institute. https://worldwealthreport.com

Sotheby’s International Realty. (2026). 2026 luxury outlook report: Prime numbers. https://www.luxuryoutlook.com/2026-luxury-outlook-report/prime-numbers

Candelon, B., Fuerst, F., & Hasse, J.-B. (2021). Diversification potential in real estate portfolios. Économie Internationale, 166, 126–139. https://doi.org/10.2139/ssrn.3831041

Fehrle, D. (2023). Hedging against inflation: Housing versus equity. Empirical Economics, 65(6), 2583–2626. https://doi.org/10.1007/s00181-023-02449-z

Coldwell Banker Global Luxury. (2026). 2026 trend report: Gen X, Millennials to inherit $2.4 trillion in U.S. real estate wealth over the next 10 years [Press release]. PR Newswire. https://www.prnewswire.com/news-releases/coldwell-banker-global-luxury-2026-trend-report-gen-x-millennials-to-inherit-2-4-trillion-in-us-real-estate-wealth-over-the-next-10-years-302663032.html

Higgins, K. (2022). Dynasties in the making: Family wealth and inheritance for the first-generation ultra-wealthy and their wealth managers. The Sociological Review, 70(6), 1267–1283. https://doi.org/10.1177/00380261211061931

Hjalager, A.-M., Sørensen, M. T., Steffansen, R., & Staunstrup, J. K. (2023). Sales prices, social rigidity and the second home property market. Journal of Housing and the Built Environment, 38(3), 1205–1228. https://doi.org/10.1007/s10901-023-09969-9

Paris, C. (2009). Re-positioning second homes within housing studies: Household investment, gentrification, multiple residence, mobility and hyper-consumption. Housing, Theory and Society, 26(4), 292–310. https://doi.org/10.1080/14036090802300392

Julius Baer. (2024). The global wealth and lifestyle report 2024. https://www.juliusbaer.com/fileadmin/publications/The_Julius_Baer_Global_Wealth_and_Lifestyle_Report_2024.pdf

Savills. (2025). New locations, new priorities: HNWIs adapt their property portfolios. https://impacts.savills.com/market-trends/new-locations-new-priorities-hnwis-adapt-their-property-portfolios.html

Walters, T., & Carr, N. (2019). Changing patterns of conspicuous consumption: Media representations of luxury in second homes. Journal of Consumer Culture, 19(3), 295–315. https://doi.org/10.1177/1469540517717778

Idealista. (2026, March 9). Spain’s most competitive property markets in 2025. https://www.idealista.com/en/news/property-for-sale-in-spain/2026/03/09/887675-spain-s-most-competitive-property-markets-in-2025

Idealista. (2026, February 23). Spain’s prime properties poised for 10% growth in 2026. https://www.idealista.com/en/news/luxury-real-estate-in-spain/2026/02/23/881539-spain-s-prime-properties-poised-for-10-growth-in-2026

Staples, A. (2014). Foreign direct investment and economic revitalization in Japan: The role of the foreign firm in Niseko. In C. G. Alvstam, H. Dolles, & P. Ström (Eds.), Asian inward and outward FDI. Palgrave Macmillan. https://doi.org/10.1057/9781137312211_7

New Zealand Herald. (2026, March). Foreign buyers rush into Queenstown luxury property as rules ease. NZME. https://www.oneroof.co.nz/news/queenstown-gazillionaires-ultra-wealthy-foreign-buyers-chasing-resort-towns-luxury-homes-48833