For crypto investors, the core question has changed. It is no longer just what to invest in, but where to base digital-asset activity as regulatory frameworks mature. Crypto becomes embedded in national tax, licensing, and reporting systems; thus, jurisdictional planning has shifted from a theoretical consideration to a practical requirement.

This briefing analyses the jurisdictions that offer the most secure environments for crypto capital, examining how regulation, infrastructure, and mobility options interact to support compliant, scalable digital-asset strategies. It reflects crypto’s evolving role not only as an investment asset, but also as an enabler of international relocation and asset diversification, increasingly integrated into formal financial and legal systems.

It argues that the next generation of digital-asset hubs is defined less by tax incentives or adoption metrics and more by regulatory clarity, institutional-grade infrastructure, and predictable compliance pathways, particularly in custody, tokenization, and reporting. As initiatives such as the EU’s MiCAR framework and expanded U.S. enforcement demonstrate, digital-asset activity is no longer insulated from territorial jurisdiction but is being re-embedded within national regulatory regimes.

Despite this shift, mobility remains under-examined in crypto strategy. This analysis addresses that gap by showing how investment migration acts as a core enabler of crypto infrastructure, positioning residency and citizenship as instruments of risk management and strategic optionality – and crypto itself as an enabler of international relocation.

This briefing analyzes 22 jurisdictions drawing on leading crypto adoption and regulatory indices, including Chainalysis, Global Citizen Solutions, and CCN. Instead of identifying a single “best” jurisdiction, it evaluates regulatory clarity, tax treatment, and digital-asset infrastructure to assess investors’ suitability across different contexts. Jurisdictions are grouped into distinct hub archetypes to highlight comparative strengths and trade-offs, reflecting the diverse roles countries play within the global digital-asset ecosystem.

Crypto-assets

A broad category of digital assets recorded using cryptography and distributed ledger technology. They can perform economic functions similar to traditional financial instruments and are subject to international regulatory scrutiny to address financial stability, investor protection, and market integrity (Financial Stability Board and International Monetary Fund, 2023).

Stablecoin

A subset of crypto-assets designed to maintain a stable value relative to a reference asset, such as a fiat currency. Their rapid growth and use in trading and payments have prompted evolving regulatory frameworks globally, as stablecoin regulation directly affects liquidity and settlement mechanisms in digital-asset markets (Tobias, et al., 2025).

Tokens / Tokenized Assets

Digital representations of rights, claims, or ownership that can include traditional financial assets or other economic interests. Tokenization bridges crypto with traditional finance and is increasingly recognized in regulatory discussions as foundational to future digital finance infrastructure (Tobias, et al., 2025).

International bodies such as the Financial Stability Board1 stress the need for consistent regulatory and supervisory frameworks for crypto-assets and stablecoins, given their potential to create financial stability risks when regulated unevenly across jurisdictions. Jurisdictional choice therefore functions as a primary investment variable, shaping risk, scalability, and long-term viability.

Cryptocurrencies have expanded rapidly from zero in 2008 to a peak market value of more than USD 4 trillion nowadays, as explained below.

Since Bitcoin’s launch in 2009, cryptocurrencies have developed from a small technology-led concept into a recognized asset class. By 2019, total crypto market capitalization increased from around USD 125 billion to over USD 370 billion, reflecting renewed market confidence and growing participation from both retail investors and early institutional players.

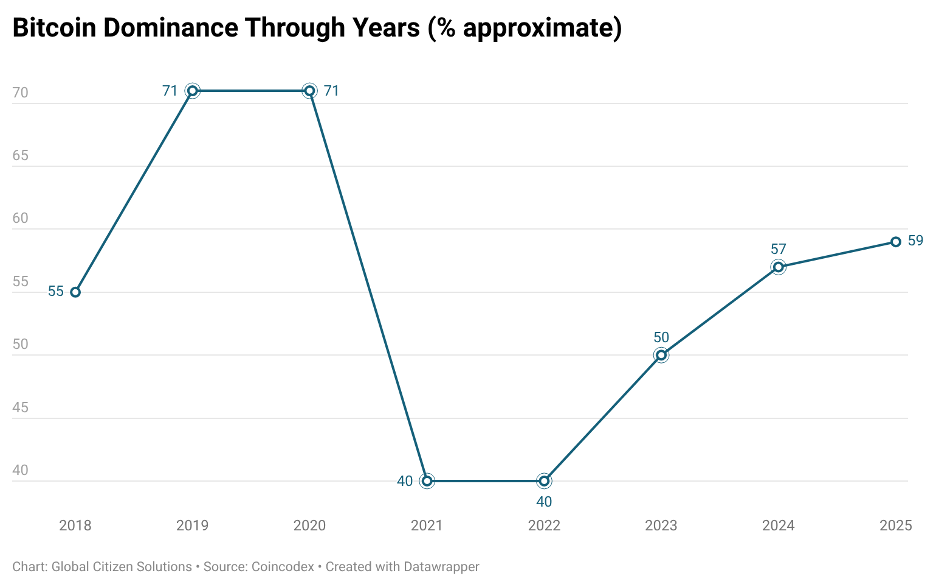

Growth has accelerated further in recent years. IMF data shows that total crypto-asset market capitalization exceeded USD 3.5 trillion in Q2 (International Monetary Fund, 2025) 2025 and reached approximately USD 4.2 trillion by Q3, while Bitcoin’s market share declined modestly as the broader ecosystem expanded.

Bitcoin reached approximately USD 125,184 in October 2025, before entering a sustained correction phase over the following months. By February 10, 2026, the cryptocurrency’s price had declined to around USD 70,464 reflecting a significant market drawdown. (CoinMarketCap, 2025). Deutsche Bank explains that Bitcoin declined by more than 40% from its peak, partly due to reduced institutional exposure and capital shifting to other assets (Deutsche Bank, 2025).

Despite ongoing volatility, market capitalization remains a key indicator of crypto’s economic relevance and scale. Furthermore, as of August 2025 stablecoins comprised 30% of all on-chain crypto transaction volume, recording the highest annual rate to date (TRM Labs, 2025).

As cryptocurrencies have grown in scale and adoption, tokenization has emerged as a related and increasingly relevant development. It is now viewed by global standard-setters not as a niche crypto application, but as part of the future financial infrastructure.

The Bank for International Settlements (BIS) defines tokenization as the digital representation of traditional financial assets, such as bank deposits and government bonds, on shared or interoperable ledgers, enabling greater automation and efficiency.

For investors, tokenization matters because it can reduce intermediaries, lower transaction costs, and speed up cross-border payments and settlement. The BIS notes that future financial systems are likely to combine tokenized central bank money, commercial bank money, and government securities, pointing to hybrid markets where digital and traditional finance increasingly converge (Bank for International Settlements, 2025).

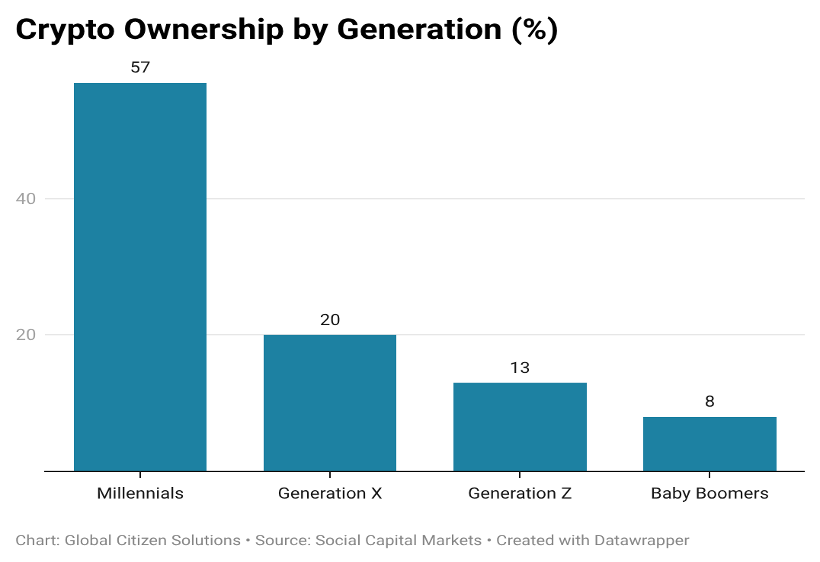

Millennials continue to represent the largest share of cryptocurrency owners, accounting for approximately 57% of total holders, followed by Generation X (20%), Generation Z (13%), and Baby Boomers (8%), reflecting the strong presence of younger cohorts in the digital asset space (Social Capital Markets, 2025) (chart below). Beyond age, participation varies across gender, income, and geography, revealing broader patterns in global adoption.

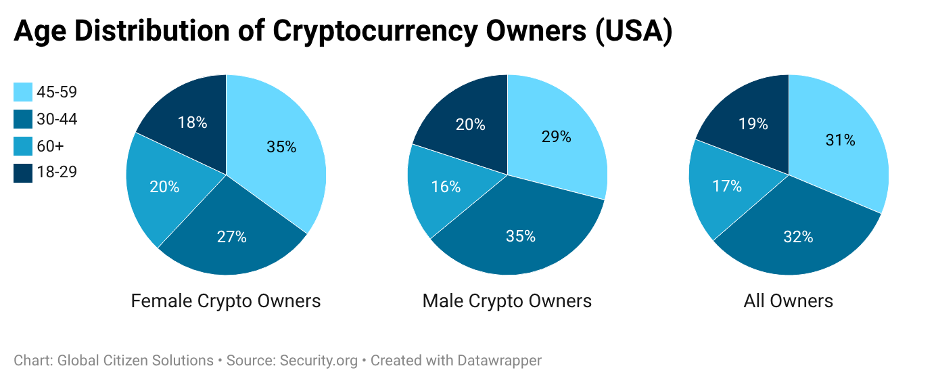

Globally, men comprise around 61% of crypto owners, while women account for approximately 39%, although participation differs notably by country. For example, women represent about 37% of crypto owners in the United Kingdom, over 50% in Indonesia, and roughly 24% in France, illustrating meaningful regional variation. Income is another important factor: in the United States, crypto owners report an average annual income of approximately USD 111,000, above the national average, suggesting stronger participation among higher-income individuals (CoinLedger, 2025).

Regionally, Asia accounts for a substantial share of global crypto users, particularly in fast-growing markets such as India, Vietnam, and the Philippines, while North America and Europe maintain steady but comparatively smaller portions of global adoption (Chainalysis, 2025).

Overall, cryptocurrency ownership remains more prevalent among younger, higher-income, and male investors, with regional economic dynamics shaping participation worldwide.

A behavioral pattern related to this data is that individuals with higher risk tolerance are significantly more likely to own cryptocurrencies, a trait more common among younger cohorts. Overall, crypto owners exhibit higher financial risk tolerance than non-owners, even after controlling for income and education (Di Giacomo et al, 2024).

A “secure” crypto jurisdiction is generally characterized by a stable and transparent operating environment supported by three core pillars:

- Regulatory clarity: Clear legal definitions of digital assets, defined licensing regimes, and established supervisory authorities.

- Institutional infrastructure: Access to regulated exchanges, custodians, banking services, and tokenization platforms.

- Predictable tax and compliance treatment: Well-defined rules on gains, reporting obligations, and enforcement standards.

Jurisdictions with unclear or overly permissive frameworks may attract short-term activity but can expose investors to regulatory uncertainty, banking restrictions, or future enforcement risks.

An important yet underexplored dimension of cryptocurrency adoption is its role as a facilitator of international relocation and cross-border mobility. Beyond its function as a financial and store-of-value instrument, cryptocurrency increasingly operates as a strategic mechanism for wealth diversification, jurisdictional flexibility, and mobility planning among high-net-worth individuals (HNWIs) and globally oriented investors.

Crypto Citizenship: An Emerging Concept

The term “crypto citizenship” (Global Citizen Solutions, 2025) refers to the ability of individuals to obtain legal residency or citizenship in a foreign jurisdiction using wealth derived from cryptocurrencies. In practice, this is typically achieved through formal residency- or citizenship-by-investment (RCBI) programs, where applicants may:

- Invest directly using crypto assets

- Present cryptocurrency holdings as proof of funds

- Convert digital assets into fiat currency through licensed intermediaries to meet regulatory requirements

From an investor perspective, crypto citizenship reflects a structural shift in how states recalibrate capital-attraction and migration frameworks to accommodate digitally native wealth, while investors deploy crypto holdings to enhance geographic diversification, regulatory optionality, and long-term capital preservation.

Mobility Capacity

A passport determines how easily an individual can relocate in response to regulatory changes and maintain multiple residences with minimal administrative friction. The citizenship one holds directly affects jurisdictional flexibility and access to alternative regulatory environments.

Compliance and Risk Assessment

Citizenship influences compliance screening processes, particularly in contexts shaped by international sanctions regimes, geopolitical considerations, and financial risk frameworks. Certain nationalities may trigger enhanced due diligence requirements or limitations on access to financial services and cryptocurrency exchanges.

Citizenship-Based Tax Obligations

A small but significant subset of jurisdictions imposes reporting or taxation requirements tied to citizenship rather than residence. The United States, for example, requires all citizens to report worldwide income and cryptocurrency holdings regardless of their country of residence. Holders of U.S. citizenship must comply with these obligations even when living and investing abroad, making nationality a direct and ongoing consideration for affected crypto investors.

International taxation can be based on two main concepts: the concept of source and the concept of residence. Tax systems worldwide are structured primarily around the concept of tax residency (United Nations). While a small number of countries base taxation on citizenship and others function as tax havens, the majority of jurisdictions determine tax obligations based on an individual’s residency status. This fundamental principle has significant implications for cryptocurrency taxation.

Tax residency determines several key factors:

- Whether cryptocurrency gains are subject to taxation

- The classification of gains for tax purposes (capital gains versus ordinary income)

- Record-keeping requirements

- Disclosure and reporting obligations

Importantly, tax obligations may arise even in the absence of transactions. Certain jurisdictions mandate annual reporting of foreign accounts, digital assets, or holdings that exceed specified thresholds, regardless of whether assets have been sold or converted. When transactions do occur, the tax treatment of cryptocurrency gains varies substantially depending on the taxpayer’s residency status at the time of the transaction.

Regulatory and tax developments now directly influence crypto asset prices, liquidity, and investor behavior, making regulation a core driver of risk and return. In response, jurisdictions are adopting more prescriptive reporting and enforcement frameworks.

The United States exemplifies this shift: effective January 1, 2025, expanded digital-asset reporting requirements include broker-level reporting under Form 1099-DA and enhanced transaction traceability, signaling a broader move toward treating digital assets like traditional financial instruments with stronger transparency and systemic integration (Ernst and Young, 2025).

This expansion of digital assets has exposed a structural gap in existing tax and regulatory systems. Most frameworks were not designed for assets that function simultaneously as investment vehicles, payment instruments, and stores of value without central intermediaries. The IMF notes that features such as cross-border mobility and limited traceability complicate traditional reporting and enforcement, placing pressure on income, capital gains, and consumption tax regimes (International Monetary Fund, 2023).

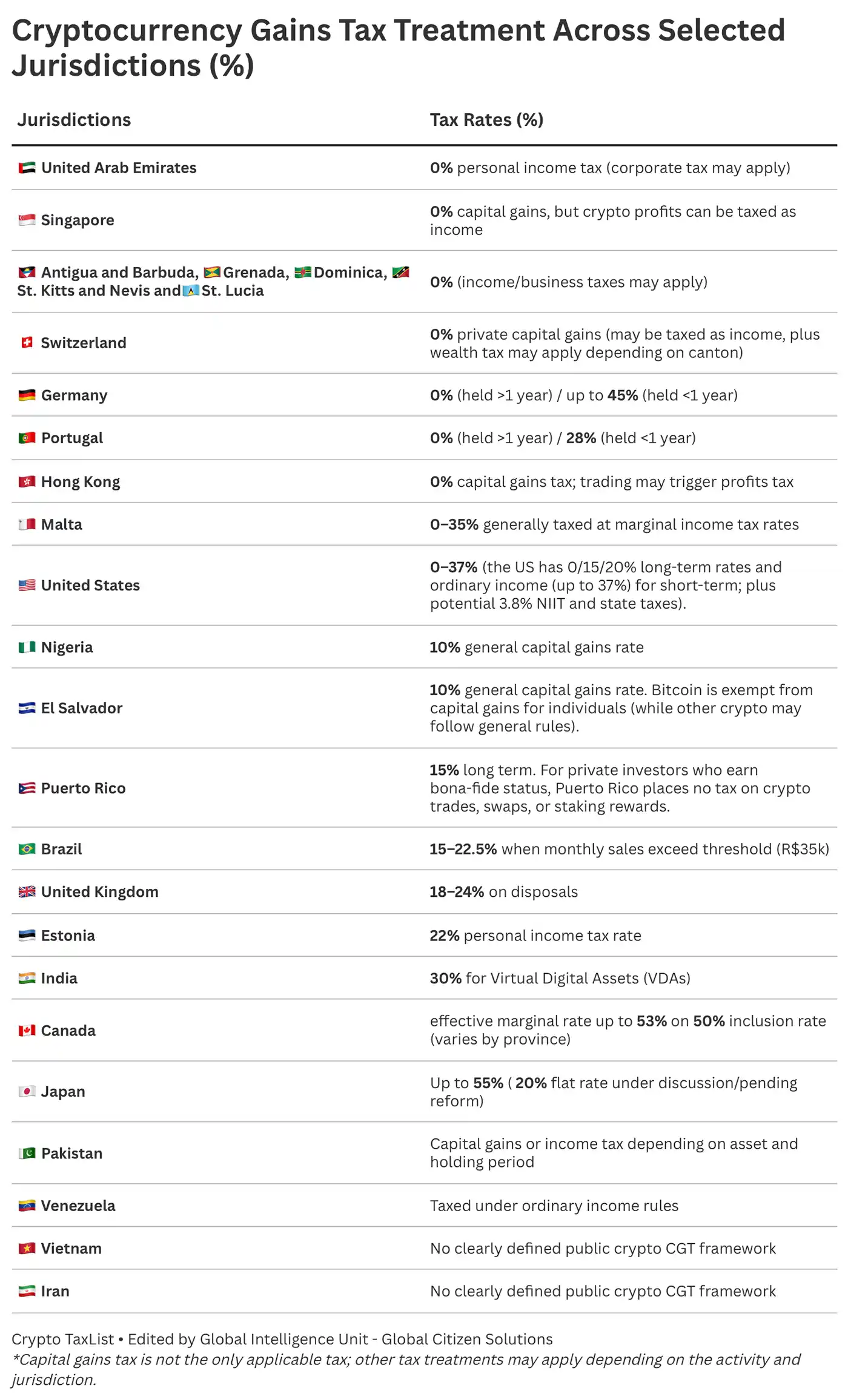

*The table compares maximum tax rates on individual cryptocurrency capital gains across 20 countries, ranked from lowest to highest, illustrating the sharp contrast in global tax treatment. As displayed, Japan stands out as particularly punitive, with rates up to 55, often viewed as a deterrent to investors and innovation.

- Crypto taxation varies by jurisdiction: some countries apply capital gains tax, while others tax crypto as income or under a wealth/deemed return system.

- Holding-period exemptions may apply (e.g., Germany, Portugal).

- In the U.S. and Canada, effective rates depend on income level, classification, and may include state or provincial taxes.

- Capital gains tax is not the only applicable tax; other tax treatments may apply depending on the activity and jurisdiction.

Academic studies (Lazea et al., 2025) show that national responses remain fragmented, since there is no harmonized international framework for most cases. Depending on the jurisdiction, crypto-related income may be treated as capital gains, ordinary income, or business profit, while the indirect tax treatment of exchanges and intermediaries varies widely. This lack of consistency increases compliance burdens, complicates cross-border investment, and creates scope for regulatory arbitrage.

Recent research (Bhullar et al, 2025) further suggests that these challenges cannot be resolved through isolated national measures alone. Greater alignment in digital financial reporting, alongside clearer accounting standards such as International Financial Reporting Standards (IFRS) and United States Generally Accepted Accounting Principles (U.S. GAAP), is increasingly viewed as essential to improving transparency, strengthening enforcement, and integrating digital assets into established financial systems.

Investor takeaway: Jurisdictional choice now depends less on headline tax rates and more on regulatory coherence, predictability, and enforceability, particularly around tax classification and reporting, which directly shape compliance risk and long-term viability.

Crypto remains global in technology but increasingly local in law. While digital-asset transactions can move across borders in minutes, real-world crypto activity depends on regulated infrastructure- exchanges, custodians, banking relationships, stablecoin issuers, and tax-reporting systems, all of which operate within national legal frameworks. Any interaction with the formal financial system, from converting crypto to fiat to accessing institutional custody or banking services, creates a traceable legal footprint subject to regulatory oversight.

As a result, banks and financial institutions assess crypto participants through jurisdiction-specific risk lenses, including residency and citizenship, source of funds and wealth, use of regulated service providers, and exposure to higher-risk regions or activities. Even compliant investors may face “de-risking,” such as account closures or transaction restrictions, reflecting the heightened regulatory sensitivity surrounding digital assets.

Regulation has become a competitive differentiator. The PwC Global Crypto Regulation Report (PWC, 2025) documents a global shift from ad-hoc approaches toward structured, framework-based oversight. Licensing regimes, clearer rules for service providers, and stronger governance standards now form the foundation of credible digital-asset ecosystems, with predictable regulatory environments increasingly attracting long-term capital over speculative flows.

The European Union and the United States illustrate how distinct regulatory strategies can nonetheless converge toward similar objectives. In the EU, MiCAR establishes a harmonized framework enabling crypto firms to operate across the single market under consistent rules, reducing regulatory fragmentation and legal uncertainty. By contrast, the U.S. approach has historically been more fragmented and enforcement-led, relying on existing securities and commodities laws, although regulatory momentum is shifting toward greater coordination and clearer supervisory boundaries.

Despite these differences, both regions are moving toward deeper integration of digital assets into the broader financial system in ways that strengthen investor protection and financial stability. For investors, this convergence reduces long-term regulatory uncertainty, even as short-term compliance paths and enforcement dynamics continue to diverge (PWC, 2025).

As regulatory frameworks mature, attention increasingly shifts from market access alone to the quality of investor and user protection. The U.S. Treasury notes that rapid growth in crypto-asset markets, now involving millions of participants, including an estimated 12 % of Americans, has increased transaction volumes, asset diversity, and interconnectedness with traditional finance, elevating risks related to market integrity, operational resilience, and consumer protection (US Department of Treasury). From an investment perspective, jurisdictions that prioritize coordinated oversight, risk mitigation, and clear supervisory guidance are more likely to attract durable capital. Academic research reinforces this view, showing that regulatory clarity has become a key driver of crypto adoption, market structure, and institutional participation (US Department of Treasury). In this context, regulatory ambiguity is no longer a competitive advantage, but an increasingly material source of investment risk.

Regulatory clarity alone does not guarantee that cryptocurrency activity can function in the real economy. Regardless of licensing status or tax treatment, crypto “works” only where banks are willing to onboard, maintain, and service crypto-exposed clients over time.

Even in formally regulated environments, banks routinely exit or refuse crypto-related relationships. FATF (2023) notes that financial institutions engage in “de-risking” by terminating or limiting relationships to manage AML/CFT exposure. This dynamic has affected virtual asset service providers’ access to banking services.

Common triggers include:

- Unclear source of funds or wealth, particularly where crypto activity predates current regulation

- Exposure to high-risk jurisdictions, including sanctioned or weakly regulated markets

- Use of unlicensed or offshore exchanges and custodians

- Complex personal residency or citizenship profiles, especially involving higher-risk nationalities

- Operational opacity, including inadequate transaction records or weak internal controls

- Regulatory asymmetry, where crypto activity is legal but supervisory expectations remain fragmented

De-risking is often precautionary rather than punitive. Banks frequently act to protect their correspondent relationships, even when clients are technically compliant.

Where Banks Commonly Onboard Crypto Clients: Bank willingness to service crypto clients is highly jurisdiction-dependent and correlates more strongly with institutional integration than with adoption levels.

High-probability onboarding environments: Switzerland, Singapore, Germany, the United Kingdom, the UAE, and Hong Kong demonstrate relatively consistent bank participation. In these jurisdictions, crypto is treated as a regulated financial activity rather than an exceptional risk category. Regulated exchanges, custodians, funds, and professionally structured investors can generally secure accounts, although onboarding remains documentation intensive.

Conditional onboarding environments: Portugal, Malta, Estonia, and Canada permit crypto-related banking but apply stricter scrutiny to foreign clients, retail-heavy activity, or complex structures. Access often depends on local substance and conservative operating models.

Low-reliability environments: High-adoption markets such as Nigeria, Vietnam, India, and Pakistan show limited institutional bank engagement despite widespread crypto usage. Banking access can be inconsistent, policy-sensitive, or restricted to narrow use cases.

Durable stablecoin banking environments: Switzerland, Singapore, Hong Kong, the UAE, and the United States host banks servicing stablecoin issuers, reserve accounts, and settlement flows within defined supervisory frameworks. These environments support scalable fiat–crypto convertibility.

Fragile or indirect banking environments: In many jurisdictions, stablecoin activity relies on correspondent banking, offshore accounts, or intermediary payment providers, making these structures more vulnerable to sudden account closures or regulatory shifts.

The presence of a formal stablecoin regime (e.g., EU MiCAR, Hong Kong’s Stablecoins Ordinance) increasingly signals where durable banking relationships are likely to persist.

Foreign Residents and Non-Residents: Practical Access: For internationally mobile investors, residency status often matters as much as regulation.

Easier onboarding: Jurisdictions aligning crypto regulation with investment migration frameworks (e.g., UAE, Switzerland, Portugal, Malta) tend to offer more predictable banking access for foreign residents with legitimate permits and demonstrable economic substance.

More restrictive onboarding: Non-residents without local presence face materially higher rejection rates. Local residency, tax identification, and demonstrable economic ties significantly improve onboarding outcomes.

Investor Takeaway

Bankability is the practical test of crypto friendliness. Jurisdictions combining clear regulation with active bank participation enable crypto to function as regulated financial infrastructure. Those relying on informal tolerance, correspondent workarounds, or policy ambiguity expose investors to sudden loss of access, even where activity remains legally permitted.

Investors should therefore assess not only what regulation allows, but what banks are willing to support in practice, aligning jurisdictional choice, residency planning, and operational structure accordingly.

This briefing examines 22 jurisdictions, selected through a benchmarking approach rather than a single composite ranking. Jurisdictions were included based on their consistent presence across leading indicators of crypto adoption, regulatory engagement, and digital-asset infrastructure, specifically the Chainalysis 2025 Global Crypto Adoption Index, the Global Citizen Solutions Crypto-Friendly Jurisdictions Report/Index 2024, and the CCN Crypto Regulation Scorecard.

Rather than identifying a single “best” jurisdiction, the analysis applies a uniform comparative framework regulatory clarity, tax treatment, and digital-asset infrastructure to assess differences in investor suitability. This approach reflects the reality that leading digital-asset hubs serve distinct investor profiles and strategic objectives. Accordingly, the briefing emphasizes comparative strengths and trade-offs, rather than producing an aggregate score.

To support this comparison, jurisdictions are grouped into the following hub archetypes:

- Institutional Benchmarks

Jurisdictions offering high regulatory credibility, legal certainty, and strong institutional integration within the digital-asset ecosystem:

Switzerland, Singapore, Japan, Canada, United Kingdom.

- Structuring & Mobility Hubs

Jurisdictions relevant for founders, HNWIs, and funds seeking to optimize tax exposure, separate operational presence from personal residency, or secure legal status within the EU or Gulf region. In these cases, investment migration functions as a structuring tool, aligning residency and substance requirements with compliant digital-asset activity while preserving market access:

UAE, Puerto Rico, Portugal, Germany, Malta, Estonia.

- Market & Capital Powerhouses

Jurisdictions that function primarily as major markets (buy and sell) rather than domiciles, offering scale, liquidity, and capital access rather than structuring advantages:

United States and Hong Kong

- High-Growth Markets

Jurisdictions characterized by rapid user adoption and expanding digital-asset ecosystems, accompanied by increasing regulatory engagement and elevated policy volatility:

Brazil, Vietnam.

- Experimental Cases

Jurisdictions pursuing state-led crypto experimentation, including the adoption of Bitcoin as legal tender or the use of crypto-centric investment and citizenship narratives as development tools:

El Salvador and selected Caribbean nations.

- Adoption Markets

Jurisdictions with high levels of user-level crypto adoption but limited legal certainty, institutional stability, or investor usability. Adoption in these contexts is often driven by macroeconomic pressures such as inflation, remittance dependence, or restricted access to traditional banking:

Nigeria, India, Pakistan, Iran, and Venezuela

Switzerland

Regulatory Clarity

Switzerland is widely seen as a global reference point for regulatory clarity in digital assets. Early on, the Swiss Financial Market Supervisory Authority (FINMA) issued detailed guidance on token classification, distinguishing between payment, utility, and asset tokens, and clarifying how existing financial market laws apply to crypto-assets (FINMA, 2018). This principle-based framework has provided legal certainty and consistent supervision, while still leaving room for innovation within well-defined boundaries.

Taxation

Switzerland offers an unusually high level of tax clarity for digital assets. The Swiss Federal Tax Administration has issued official guidance on the taxation of cryptocurrencies and tokenized assets, addressing wealth tax, income tax, and asset classification for both private and professional investors (Swiss Federal Tax Administration). For individuals, private capital gains are generally tax-exempt, while wealth tax is levied annually at cantonal rates. For corporations, crypto-related income is taxed under standard federal and cantonal regimes, with combined rates typically ranging from 12% to 20%, depending on the canton (Coin Club, 2025).

Digital Asset Infrastructure

Switzerland’s digital-asset ecosystem is primarily institutionally driven rather than retail-led. While the country does not rank among the top jurisdictions for retail crypto adoption, this reflects a strategic focus on governance, financial infrastructure, and institutional participation rather than transaction volume (Chainalysis, 2025). In 2019, FINMA granted full banking and securities dealer licenses to SEBA and Sygnum – among the first globally- enabling digital assets to be fully integrated into regulated banking services (Swissinfo, 2019). Switzerland is also recognized as a global leader in asset tokenization, supported by strong legal foundations and a sophisticated capital markets ecosystem (Quay Research Analysis & Consulting2024). Furthermore, the canton of Zug, widely known as “Crypto Valley,” has become a major blockchain hub, hosting a dense concentration of digital-asset firms and service providers and generating strong network effects for investors and entrepreneurs (Canton of Zug).

Investor profile

Institutional investors, regulated funds, tokenization projects, and high-net-worth individuals prioritizing legal certainty, asset protection, and mature financial infrastructure.

Singapore

Regulatory Clarity

Singapore has established itself as one of Asia’s most credible and institutionally focused digital-asset hubs, combining clear regulation with strong supervisory capacity. Digital-asset activities are primarily governed by the Payment Services Act (PSA), administered by the Monetary Authority of Singapore (MAS), which sets out a comprehensive licensing regime for digital payment token service providers, including exchanges, custodians, and brokers, alongside robust AML/CFT, technology risk management, and consumer-protection requirements (Monetary Authority of Singapore, 2019), embedding crypto supervision within Singapore’s broader financial regulatory framework.

Taxation

Singapore offers a competitive and predictable tax environment for digital assets. The absence of capital gains tax means that long-term crypto investment gains are generally not taxable, unless the activity qualifies as a business. The Inland Revenue Authority of Singapore (IRAS) has issued detailed guidance on the income tax and GST treatment of digital payment tokens, providing clarity for companies, funds, and service providers (Inland Revenue Authority of Singapore). For individuals, investment gains are typically untaxed, while business income is taxed at progressive rates of up to 24%; for corporations, crypto-related business income is subject to the standard corporate tax rate of 17% (Coinclub, 2025).

Digital Asset Infrastructure

More than 300 blockchain and digital-asset firms operate in or from Singapore, underscoring its role as a regional base for exchanges, infrastructure providers, Web3 developers, and regulated service firms (F6S, 2026). The country does not rank among the top jurisdictions for retail crypto adoption, this reflects a strategic emphasis on regulatory certainty, rule of law, capital-market depth, and close integration with the traditional banking system rather than mass consumer usage.

Investor profile

Institutional investors, funds, and regulated digital-asset businesses seeking a stable Asian gateway with strong regulatory credibility, deep financial-market integration, and long-term policy predictability.

Canada

Regulatory Clarity

Canada represents a structured and institutionally accessible digital-asset jurisdiction in North America, with a strong emphasis on investor protection and regulated market participation. Crypto-asset trading platforms and intermediaries are primarily regulated under existing securities laws, coordinated by the Canadian Securities Administrators (Canadian Securities Administrators).

Taxation

For tax purposes, cryptocurrencies are treated as commodities under Canadian law. Individual investors are subject to capital gains tax, with 50% of gains included in taxable income and taxed at marginal rates, while crypto-related business income is fully taxable. For corporations, income and gains from crypto activities are taxed at applicable federal and provincial corporate tax rate (Canada Revenue Agency, 2023).

Digital Asset Infrastructure

Canada has differentiated itself by enabling regulated crypto investment products within its securities framework, reinforcing its role as a jurisdiction that embeds digital assets within mainstream capital markets rather than operating parallel systems. Although Canada does not rank among the top jurisdictions for retail crypto adoption, it remains investor-relevant due to regulatory clarity, institutional credibility, and access to compliant platforms, custodians, and investment vehicles.

Investor profile

Canada is best suited for institutional and compliance-driven investors seeking regulated market access, strong investor protection, and integration of digital assets into traditional securities markets, rather than tax-optimized or retail-led crypto activity.

Japan

Regulatory Clarity

Japan was among the first major economies to establish a comprehensive statutory framework for cryptocurrencies. Crypto-assets are regulated primarily under the Payment Services Act (PSA) and the Financial Instruments and Exchange Act (FIEA), under the supervision of the Financial Services Agency (FSA). The framework imposes mandatory licensing, strict AML/CFT requirements, robust custody rules, and ongoing supervisory oversight for crypto-asset exchange service providers (Financial Services Agency, 2022).

Taxation

The country applies one of the most burdensome tax regimes for individual crypto investors among developed economies. Individual crypto gains are classified as miscellaneous income and taxed at progressive national rates of 5%–45%, plus local inhabitant taxes of approximately 10%, resulting in a combined top marginal rate of around 55%. Corporate crypto gains are taxed as ordinary business income at an effective combined national and local rate of roughly 30% (Koinly). Ongoing policy discussions propose shifting individual crypto taxation toward a flat rate of around 20%, aligned with traditional financial investments and potentially allowing loss carry-forward (Patairya, 2025).

Digital Asset Infrastructure

Japan’s digital-asset infrastructure is defined by stringent custody and asset-segregation requirements. Licensed providers must segregate client assets from corporate funds, hold the majority of customer crypto-assets in offline (cold) storage, and subject custody arrangements to independent audits (Crypto for Innovation, 2023). It’s role in the global digital-asset landscape is shaped by regulatory rigor and institutional safeguards rather than user scale.

Investor profile

Regulated exchanges, custodians, and institutions prioritizing consumer protection, legal certainty, and systemic stability over rapid growth or retail scale.

The United Kingdom

Regulatory Clarity

The United Kingdom approaches digital assets through integration into its established financial-services framework, with a strong emphasis on market integrity, enforceability, and financial stability. Crypto-asset businesses operating in the UK must register with the Financial Conduct Authority (FCA) under the UK’s anti-money-laundering and counter-terrorist-financing regime and demonstrate robust governance, financial-crime controls, and consumer-protection standards before serving the UK market (Financial Conduct Authority, 2026). This registration-based perimeter provides a regulated baseline for institutional participation, with scope for expansion into broader conduct.

Taxation

The UK applies a clear and well-established tax framework to crypto-assets. For individuals, crypto disposals are subject to Capital Gains Tax at 18% for basic-rate taxpayers and 24% for higher-rate taxpayers (for disposals on/after 30 Oct 2024), after the annual allowance, while crypto-related income (including trading, mining, and staking) is taxed as income at progressive rates of 20%–45%. For corporations, crypto income and gains are taxed as ordinary profits at the prevailing corporate tax rate of 25% (HM Revenue & Customs, 2018).

Digital Asset Infrastructure

Despite London’s status as a global financial center, the UK does not rank among the leading jurisdictions for retail crypto adoption, reinforcing its positioning as a law- and credibility-driven digital-asset hub. The UK’s digital-asset ecosystem is therefore characterized by regulated market participants, deep legal and advisory expertise, and strong links to global capital markets rather than high-volume consumer usage.

Investor profile

Institutional investors, market-infrastructure providers, and global firms prioritizing legal enforceability, common-law protections, and access to deep international capital markets.

United Arab Emirates

Regulatory Clarity

The United Arab Emirates has positioned itself as a deliberately designed digital-asset hub, defined by proactive regulation and clear jurisdictional segmentation. In Dubai, the Virtual Assets Regulatory Authority (VARA) acts as a dedicated regulator for virtual-asset activities, operating detailed licensing and rulebooks for exchanges, custodians, brokers, and advisory firms.

In parallel, the Abu Dhabi Global Market (ADGM), through its Financial Services Regulatory Authority (FSRA), has maintained a bespoke crypto regulatory framework since 2018, covering trading venues, custodians, intermediaries, and market infrastructure. This dual-regime model provides regulatory certainty across a wide range of digital-asset business models.

Taxation

The UAE offers one of the most competitive tax environments globally. Individuals are not subject to personal income or capital gains tax on crypto-assets. At the corporate level, a 9% federal corporate tax applies to taxable profits exceeding AED 375,000, including crypto-related activities conducted through licensed entities (Coinclub, 2025).

Digital Asset Infrastructure

The UAE’s digital-asset ecosystem is strongly institutional and internationally oriented, supported by advanced financial free zones, global banking connectivity, and active licensing of exchanges, custodians, tokenization platforms, and service providers. Its appeal lies less in its role as a regional and cross-border hub linking Middle East, Asian, and European markets.

Citizenship or Residency Opportunities

The UAE also provides long-term residency pathways widely used by founders, investors, and executives (UAE Government, 2025). The UAE Golden Visa offers renewable long-term residence for investors, entrepreneurs, and highly skilled individuals, supporting business relocation and regional structuring.

Investor profile

Operating companies, crypto funds, and high-net-worth individuals seeking regulatory certainty, regional market access, and highly tax-efficient corporate and residency structuring.

Portugal

Regulatory Clarity

Portugal operates fully within the EU regulatory framework and is therefore subject to EU-level crypto-asset rules, including the Markets in Crypto-Assets Regulation (MiCAR). At the national level, supervision is exercised by domestic authorities, notably Banco de Portugal, which oversees registration and AML/CFT compliance for certain virtual asset service providers (Banko de Portugal). Portugal thus falls within a harmonized EU regulatory perimeter with domestic supervisory enforcement.

Taxation

Portugal’s crypto tax regime has been a key driver of investor interest. Under rules introduced in 2023, gains realized by non-professional individuals are taxed based on holding period: assets held for less than 365 days are subject to a 28% flat tax, while gains on assets held for more than one year are generally exempt from capital gains tax. Crypto mining and staking carried out as a business are taxed as ordinary income, while certain forms of passive crypto income, including delegated staking and lending, are typically taxed at 28%. Corporate crypto income is taxed at the standard corporate rate of 21% (Global Citizen Solutions, 2025).

These exemptions do not apply in all cases, including certain tokenized securities or assets linked to non-cooperative jurisdictions, reinforcing the need for careful classification and compliance. Moreover, under the 2023/2024 regime, individuals must report crypto transactions (even exempt long-term gains) on the annual Portuguese IRS tax return. Long-term tax exemption no longer means no reporting at all.

Digital Asset Infrastructure

Portugal’s digital-asset ecosystem is primarily investor and lifestyle driven rather than infrastructure-led, with more limited domestic market infrastructure than major financial hubs. Its relevance lies less in hosting large exchanges or custodians and more in its combination of EU market access, regulatory alignment, and tax treatment.

Citizenship or Residency Opportunities

Portugal’s appeal is closely linked to its residency by investment framework, which provide access to EU mobility and long-term residence; such residency, in this context, functions as a form of jurisdictional diversification by enabling optionality across tax and regulatory regimes, enhancing legal and tax planning flexibility for digital-asset investors.

Investor profile

High-net-worth individuals, founders, and investors seeking EU access and potential tax efficiencies, with a focus on compliant structuring and monitoring of evolving reporting obligations and MiCAR implementation.

Germany

Regulatory Clarity

Germany is among Europe’s most institutionally credible digital-asset jurisdictions, combining strong rule of law with a supervisory focus on investor protection and financial stability. Crypto-asset activities are overseen by the Federal Financial Supervisory Authority (BaFin), which requires authorization for regulated services such as crypto custody under the German Banking Act (KWG) (Federal Financial Supervisory Authority). As an EU member state, Germany operates fully within the Markets in Crypto-Assets Regulation (MiCAR) (European Securities and Markets Authority).

Taxation

For individuals, cryptocurrencies are generally treated as private assets: gains realized after a one-year holding period are tax-exempt, while short-term gains above the annual exemption threshold are taxed at progressive rates up to approximately 45%. For corporations, crypto-related business income is taxed at standard corporate rates (approximately 15% plus surcharges), reflecting Germany’s broader corporate tax framework (Coinclub, 2025).

Digital Asset Infrastructure

Thus, Germany functions as an EU anchor jurisdiction with deep financial-market infrastructure, regulated custody providers, and strong banking connectivity. Moreover, a distinctive institutional feature is Germany’s investment-fund framework. Under the Fondsstandortgesetz (Fund Location Act), German domestic special funds (Spezialfonds) have been permitted since August 2021 to allocate up to 20% of assets to crypto-assets, a change with potentially significant capital-market implications given the scale of the Spezialfonds market (PWC Switzerland, 2021).

Investor profile

Best suited for institutional investors, regulated funds, and operating companies seeking EU access through a high-credibility supervisory environment, strong compliance infrastructure, and low tolerance for regulatory uncertainty.

Puerto Rico

Regulatory Clarity

Puerto Rico functions primarily as a tax-residency-based structuring jurisdiction rather than a dedicated crypto regulatory hub. It does not maintain a standalone crypto licensing or supervisory regime comparable to those in the EU, Singapore, or the UK. Instead, crypto-related activity is governed by the same U.S. federal securities, commodities, and banking laws that apply on the mainland, with Puerto Rico–specific tax treatment layered on top. Its relevance for digital-asset investors therefore lies in tax and residency structuring rather than bespoke crypto regulation.

Taxation

Puerto Rico’s distinctiveness is anchored in its Incentives Code (Act 60), under which qualifying individuals and entities may obtain preferential tax treatment through decree approval and ongoing compliance (Puerto Rico Incentives Code, 2019). For individuals who become bona fide residents, certain categories of Puerto Rico–source income, including qualifying capital gains realized after establishing residency, may be taxed at 0% locally, subject to decree terms.

Puerto Rico operates within the U.S. legal and tax system, meaning U.S. federal law continues to apply, while Puerto Rico–source income is taxed locally under distinct sourcing rules. These rules are administered by the Internal Revenue Service and codified in the Internal Revenue Code, including the exclusion of Puerto Rico–source income for qualifying residents (Internal Revenue Service). For corporations, export services conducted from Puerto Rico may benefit from reduced local corporate tax rates under Act 60 (Coinclub, 2025).

Digital Asset Infrastructure

Puerto Rico is not positioned as a digital-asset infrastructure as it does not seek to attract exchanges, custodians, or token issuers through dedicated licensing regimes. Instead, its role in the crypto ecosystem is primarily transactional and post-liquidity-event-oriented.

Investor profile

U.S.-connected founders and investors seeking residency-based tax optimization for crypto liquidity events while remaining within a U.S. legal and regulatory framework.

Malta

Regulatory Clarity

Malta has developed one of the EU’s most formalized digital-asset frameworks, centered on statutory classification and licensing rather than broad permissiveness. Under the Virtual Financial Assets (VFA) Act, digital assets are legally classified to determine whether they fall under securities law, the VFA regime, or are otherwise exempt, providing legal certainty for issuers, exchanges, and service providers operating within an EU jurisdiction (Malta Financial Services Authority). Beyond crypto-asset trading, Malta has also regulated blockchain technology more broadly through the Malta Digital Innovation Authority (MDIA), which oversees certification of distributed ledger technology, innovative technology arrangements, and smart contracts. This dual-track approach prioritizes classification, disclosure, and governance over rapid market expansion.

Taxation

Malta functions primarily as a tax structuring jurisdiction, with outcomes dependent on residency status and the classification of crypto activity. For individuals, long-term capital gains on crypto-assets held as private investments (generally over 12 months and not part of a trading activity) may be tax-exempt, while short-term or frequent trading is typically taxed as ordinary income at progressive rates ranging from 15% to 35%. At the corporate level, Malta’s statutory corporate tax rate is 35%, but its full imputation and shareholder refund system can reduce the effective tax rate to approximately 5% for qualifying international businesses, provided sufficient substance and compliance requirements are met (Coinclub, 2025).

Digital Asset Infrastructure

Malta’s role in the global crypto landscape is primarily structural, anchored in regulatory design rather than retail adoption. The jurisdiction has positioned itself as an EU base for exchanges, token issuers, and blockchain fintech firms through an early and comprehensive legal framework for digital assets, initially under the Virtual Financial Assets Act and now aligned with the EU’s Markets in Crypto-Assets (MiCA) regime, administered by the Malta Financial Services Authority (MFSA). This framework provides legal clarity on token classification, licensing, and supervision, reinforcing Malta’s appeal as a regulatory hub rather than a mass-adoption market (MFSA) (Malta Financial Services Authority).

Citizenship or Residency Opportunities

A key differentiator for Malta is the integration of crypto-friendly regulation with formal investment migration pathways. Malta operates established residency and citizenship by merit programs that can complement digital-asset structuring strategies. Notably, the Malta Permanent Residence Program (MPRP) allows non-EU investors to obtain permanent residency through qualifying property investments and financial contributions, providing long-term residence and EU access alongside Malta’s regulatory framework (Global Citizen Solutions).

Investor profile

Founders, token issuers, and blockchain projects requiring formal EU asset classification and regulatory structuring. Particularly well suited for investors and entrepreneurs who value legal certainty within the EU and who may also seek EU residency or citizenship as part of a broader compliance and structuring strategy.

Estonia

Regulatory Clarity

Estonia leveraged its reputation as a highly digital society to become an early crypto hub in Europe, supported by streamlined digital company formation and its e-Residency program. From 2017, Estonia was among the first EU states to license crypto exchanges and wallet providers through the Financial Intelligence Unit (FIU), initially under a relatively streamlined regime. As EU standards evolved and supervisory expectations increased, Estonia subsequently strengthened its AML/CFT framework, resulting in a substantial reduction in the number of authorized providers and a more selective licensing environment (Coinfomania).

In response to the Markets in Crypto-Assets Regulation (MiCAR), Estonia adopted the Crypto Asset Market Act, effective 1 July 2024, aligning national law with MiCAR and transferring supervision to the Estonian Financial Supervision Authority (Finantsinspektsioon). This framework establishes a clearer, MiCAR-compliant regime that enables EU passporting for authorized crypto-asset service providers and reinforces Estonia’s compliance-first posture.

Taxation

Crypto taxation in Estonia is clearly defined by the Estonian Tax and Customs Board. Crypto disposals, exchanges, and payments are treated as taxable events, while mining income is classified as business income (Estonian Tax and Customs Board). Estonia’s corporate tax system is distinctive: companies are subject to 0% tax on undistributed profits, with tax (generally 20%) levied only upon profit distribution, making the jurisdiction structurally attractive for reinvestment-oriented operating companies.

Digital Asset Infrastructure

Estonia’s relevance in digital assets derives from its digital-state infrastructure and codified compliance environment rather than market scale.

Citizenship or Residency Opportunities

Furthermore, Estonia’s e-Residency program enables non-residents to establish and manage EU-based companies remotely, providing access to the EU business environment without physical relocation (Estonia e-Residency).

Investor profile

Founders and funds seeking EU company access, digital administrative efficiency, and clearly codified compliance rules for crypto operations, particularly tech-driven teams willing to operate under high AML and supervisory standards.

United States

Regulatory Clarity

The United States occupies a unique position in the global digital-asset landscape, combining unmatched market scale with a complex, enforcement-led regulatory approach. Rather than a single comprehensive crypto statute, digital assets are regulated through existing securities, commodities, and banking laws applied by multiple federal agencies. The Securities and Exchange Commission (SEC) maintains that many crypto-assets fall within the scope of securities law, while the Commodity Futures Trading Commission (CFTC) asserts jurisdiction over crypto-assets treated as commodities. This has produced a fragmented but gradually clarifying regulatory perimeter shaped largely by enforcement actions and court decisions (U.S. Securities and Exchange Commission).

Taxation

The U.S. applies a clearly defined but compliance-intensive tax regime to crypto-assets. For individuals, long-term crypto gains (held over one year) are taxed at preferential capital gains rates of 0%–20% depending on income, while short-term gains are taxed as ordinary income at progressive rates of 10%–37%. For corporations, crypto-related income and gains are taxed at the standard federal corporate rate of 21%, with potential additional state-level taxation (Coinclub, 2025). Moreover, reporting requirements are tightening significantly. From 1 January 2025, brokers are required to report digital-asset transactions under Form 1099-DA, introducing per-wallet reporting and enhanced disclosure obligations that align crypto taxation more closely with traditional financial instruments (Ernst and Young, 2025).

Digital Asset Infrastructure

The United States ranks second globally in crypto adoption, reflecting strong institutional participation alongside significant retail activity (Chainalysis,2025). The U.S. also hosts a deep ecosystem of exchanges, custodians, asset managers, and market-infrastructure providers. Its competitive advantage lies primarily in capital-markets depth and financial infrastructure.

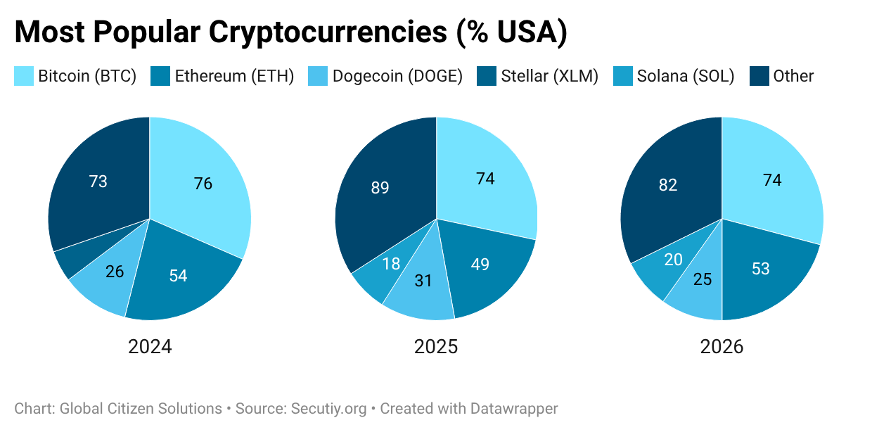

Below is an illustration of cryptocurrency ownership in the United States, by age and gender, together with a representation of most popular cryptocurrencies.

Citizenship or Residency Opportunities

The United States offers a recently introduced investment-linked residency pathway – the Gold Card program launched in September 2025. This option is not crypto-specific and operates independently of digital-asset activity under standard U.S. immigration law.

Investor profile

Institutional investors, asset managers, market-infrastructure providers, and sophisticated investors seeking liquidity, scale, and exposure to regulatory-driven market developments, with a higher tolerance for legal and compliance complexity.

Hong Kong

Regulatory Clarity

Hong Kong has emerged as one of Asia’s most institutionally credible and tightly regulated digital-asset jurisdictions, positioning itself as an onshore hub for exchanges, asset managers, and tokenized products. The Securities and Futures Commission (SFC) has established a comprehensive virtual-asset regulatory regime, licensing and supervising virtual asset trading platforms (VATPs), intermediaries, and fund managers under the principle of “same business, same risks, same rules” (Securities and Futures Commission) Hong Kong is also advancing a stablecoin regulation. The Stablecoins Bill, passed on 21 May 2025, establishes a licensing regime for fiat-referenced stablecoin issuers under the Stablecoins Ordinance, strengthening requirements on reserves, governance, and prudential oversight (Hong Kong Government, 2025).

Taxation

Hong Kong offers a competitive and predictable tax environment for digital assets. There is no capital gains tax on private crypto disposals and no VAT, GST, or stamp duty on crypto transfers. Corporate profits arising from crypto-related activities – such as trading, exchange operations, or custody services, are generally taxed under Hong Kong’s standard profits tax rate of 16.5%, with tax treatment guided by established principles on source of income and business classification (Hong Kong Institute of Certified Public Accountants).

Digital Asset Infrastructure

Hong Kong’s digital-asset ecosystem is institutional by design, prioritizing governance, licensing, and prudential safeguards over mass-market retail adoption. Retail crypto usage is not among the highest globally; the city’s strengths lie in its deep capital markets, regulated intermediaries, and its role as a bridge between global financial institutions and the broader Asia-Pacific region.

Brazil

Regulatory Clarity

Brazil is widely recognized as one of the world’s highest-ranking crypto adoption markets, placing fifth globally in the Chainalysis 2025 Global Crypto Adoption Index, reflecting broad engagement across both retail and institutional channels. This scale of usage is increasingly matched by formal regulatory structuring: in late 2025 the Central Bank of Brazil (CBB) issued a comprehensive regulatory framework for virtual asset service providers (including licensing, operational standards, and supervision), positioning the BCB as a key supervisory authority where crypto activities intersect with payments, custody, and financial stability (Banco Central do Brasil, 2025).

Taxation

Cryptocurrencies are treated as assets for tax purposes in Brazil. For individuals, crypto gains are generally taxed at a flat rate of approximately 15%, while for corporations crypto-related income is taxed under standard corporate income tax rules, commonly around 15% under simplified regimes (Coinclub, 2025). Reporting and compliance obligations have been strengthened, including updated declaration requirements and expanded transaction reporting frameworks introduced through regulatory instructions in late 2025, with further implementation phases scheduled from 2026.

Digital Asset Infrastructure

Brazil’s digital-asset ecosystem is adoption-driven and increasingly institutionalizing. The country hosts large domestic exchanges, strong fintech integration, and growing participation from traditional financial institutions, supported by Brazil’s advanced payments infrastructure and large consumer base. While regulatory architecture is still maturing, the trajectory is toward greater clarity and institutional compatibility rather than retrenchment (Chainalyis, 2025).

Investor profile

Best suited for growth-oriented investors, exchanges, and market operators targeting Latin American scale, particularly those comfortable operating in evolving regulatory and tax environments with rising institutional engagement.

Vietnam

Regulatory Clarity

Vietnam consistently ranks among the world’s highest crypto adoption markets (Chainalysis, 2025), reflecting strong retail participation and on-chain activity. For much of its development, this adoption occurred in a regulatory grey area, with limited legal recognition of crypto-assets and constrained certainty for service providers.

A significant shift occurred in June 2025, when Vietnam’s National Assembly passed the Law on Digital Technology Industry, effective 1 January 2026. The law formally recognizes digital and crypto assets and introduces a framework for regulated trading and pilot licensing of exchanges, signaling a transition toward structured oversight, although detailed rules on custody, reporting, and investor protection remain under development (CryptoNews, 2026).

Taxation

Historically, cryptocurrencies were not formally recognized as lawful financial instruments in Vietnam, and use of crypto as a means of payment was explicitly prohibited under directives from the State Bank of Vietnam. As a result, the legal status and tax treatment of crypto transactions remained unclear under existing law, with no comprehensive crypto-specific tax regime firmly established by late 2025. In response, the Vietnamese National Assembly passed the Law on Digital Technology Industry in June 2025, scheduled to take effect January 1, 2026, which formally recognizes crypto assets and provides a legal basis for future regulatory and tax frameworks (Coindesk, 2025).

Digital Asset Infrastructure

Vietnam’s crypto ecosystem is retail- and peer-to-peer-driven, with millions of users accessing global platforms rather than operating through a dense domestic institutional infrastructure. Adoption significantly outpaces regulatory and custodial development, making Vietnam a leading indicator of crypto usage rather than a mature hub for regulated service providers.

Investor profile

Best suited for growth-focused investors and market operators seeking exposure to high-adoption environments, with a higher tolerance for regulatory uncertainty and evolving compliance frameworks as formal oversight develops.

These jurisdictions represent experimental or non-traditional intersections between digital assets and investment migration, where crypto’s relevance is driven less by mature financial infrastructure and more by its role in mobility, onboarding, and capital portability. In these cases, citizenship or residency is the core proposition, and crypto functions as an enabling mechanism rather than the object of regulation itself.

El Salvador

Regulatory Clarity

El Salvador represents the most explicit global example of a crypto-centered citizenship proposition. The country has established a dedicated legal and regulatory framework for digital assets through the Digital Assets Law and a specialized regulator, the National Commission of Digital Assets (CNAD), covering issuance, service providers, and compliance (National Commission of Digital Assets, 2023).

Taxation

El Salvador applies a 0% capital gains tax on Bitcoin transactions, while other digital assets may fall under standard income or corporate tax rules unless specific exemptions apply.

Digital Asset Infrastructure

El Salvador has built state-backed digital-asset infrastructure disproportionate to its size, including a dedicated regulator and a formal issuance regime. This infrastructure supports institutional service providers (custody, issuance, compliance) that can operate alongside migration-linked capital flows (U.S. Department of Commerce, International Trade Administration, 2024).

Citizenship or Residency Opportunities

El Salvador is the clearest example of a crypto-native, fast-track citizenship model. Through the government-run “Adopting El Salvador / Freedom” program, citizenship may be obtained via a qualifying contribution payable in BTC or USDT, explicitly positioning digital assets as a settlement medium for nationality acquisition (Government of El Salvador). In this model, crypto directly reduces cross-border banking friction for high-net-worth, crypto-native applicants.

Investor profile

Crypto-native high-net-worth individuals seeking citizenship diversification and willing to engage with a state-led crypto–migration model where policy direction remains closely tied to national strategy.

Select Caribbean Jurisdictions

Regulatory Clarity

Caribbean citizenship-by-investment (CBI) jurisdictions occupy a distinct position in the crypto–migration landscape. Unlike El Salvador, these programs do not market citizenship payable in crypto. Instead, they integrate digital assets indirectly within existing AML/CFT-driven investment migration frameworks, preserving institutional credibility while adapting to new wealth forms.

Taxation

In Caribbean CBI jurisdictions, crypto tax treatment is generally secondary, as several programs, including Antigua and Barbuda and St. Kitts and Nevis operate in low- or zero-tax environments for individuals (often 0% capital gains and personal income tax) and some rely on non-specific application of general income tax rates (typically up to 25–35%). As a result, CBI due diligence prioritizes source-of-wealth validation, capital provenance, and reputational risk management over ongoing crypto tax residence planning.

Digital Asset Infrastructure

Several Caribbean jurisdictions have implemented formal digital-asset regulatory frameworks that operate alongside, rather than supplant, their CBI programs. These frameworks facilitate the assessment, documentation, and compliant conversion of crypto-derived wealth through regulated financial channels, without repositioning CBI programs as crypto-based payment mechanisms.

Citizenship or Residency Opportunities

Across the Caribbean, crypto functions primarily as a structural enabler within CBI programs:

- Saint Kitts and Nevis recognizes cryptocurrency as an acceptable source of wealth, subject to enhanced due diligence and traceability, while maintaining fiat settlement requirements (IMI Daily,2025).

- Antigua and Barbuda operates an established CBI program alongside a Digital Assets Business Act, allowing crypto-derived funds to be incorporated into applications where provenance is clearly documented, while settlement remains fiat-based (Digital Assets Business Act, 2020).

- Grenada applies a conservative approach, with crypto relevant primarily for source-of-funds documentation, requiring conversion to fiat and robust evidentiary support.

- Saint Lucia combines a functioning CBI program with a statutory Virtual Asset Business regime, enabling regulated intermediaries to bridge crypto-derived wealth into compliant CBI investments (Financial Services Regulatory Authority, 2025).

Collectively, these jurisdictions treat crypto not as a payment mechanism for citizenship, but as an auditable asset class compatible with established investment migration processes.

Investor profile

Crypto-native high-net-worth individuals and families seeking citizenship diversification who prioritize program legitimacy, AML robustness, and the ability to deploy digital-asset-derived wealth through compliant, institutionally acceptable channels, rather than jurisdictions offering unstructured or lightly supervised “pay-in-crypto” citizenship models.

These jurisdictions have large and active crypto user bases driven by retail use, remittances, inflation hedging, and peer-to-peer activity, rather than by mature institutions or clear regulation. Crypto’s importance in these markets comes from real economy use and widespread adoption, while legal, tax, and supervisory frameworks remain limited, fragmented, or still evolving.

Nigeria, India, Pakistan, Iran, and Venezuela are all high crypto-adoption markets where usage is driven primarily by economic necessity rather than institutional maturity or regulatory clarity. In these jurisdictions, crypto adoption is largely retail-led and linked to remittances, inflation hedging, capital controls, sanctions, or peer-to-peer activity, rather than regulated investment markets or formal financial infrastructure. While some countries have taken steps toward oversight, such as Nigeria’s recognition of digital assets under the Securities and Exchange Commission (SEC) (PWC Nigeria,2025), India’s taxation of crypto gains at 30% (Chainalysis,2025), Pakistan’s creation of a virtual assets authority FirstTechSpot (2025), and Iran’s partial licensing of mining activities (Innterim, 2025) – regulatory frameworks remain fragmented, evolving, or unevenly enforced. Venezuela’s prolonged hyperinflation has further entrenched crypto as a tool for value preservation and payments amid unstable oversight (Cointelegraph, 2023).

In these countries, cryptocurrency adoption is often driven by necessity rather than preference. Crypto helps individuals deal with inflation, weak currencies, capital controls, remittances, and limited access to traditional banking, so adoption grows even when regulation, institutions, and investor protections are weak or are still in the developing phase. This makes adoption alone an unreliable indicator of crypto friendliness for investors.

As shown above, countries are making deliberate choices about the type of crypto activity they support, rather than attempting to capture the entire value chain.

Regulation has become a competitive differentiator. Jurisdictions such as Switzerland, Singapore, Germany, and the UAE are not targeting mass adoption, instead they are designing environments where crypto can operate within banks, funds, and capital markets. In these settings, crypto is treated less as a consumer-facing product and more as regulated financial infrastructure.

A second pattern emerging from the comparison is the growing role of investment migration as a safeguard. For many high-net-worth individuals, the central crypto question has shifted from “where can I trade?” to “where can I live, structure, and legally protect digital wealth?” As a result, residency and citizenship jurisdictions have become a stabilizing layer within an otherwise fragmented regulatory landscape.

This dynamic is visible in Portugal, where favorable holding-period tax rules and EU residency options attract crypto holders despite the country not being a major trading or infrastructure hub. Portugal’s appeal lies not in market depth, but in its ability to provide regulatory continuity and personal mobility for investors operating elsewhere.

The same logic applies, at a larger scale, to the United Arab Emirates. Low taxation, long-term residency visas, and dedicated crypto regulators have positioned Dubai and Abu Dhabi as relocation centers for founders, funds, and executives. Here, investment migration does not replace market participation but reinforces it by offering jurisdictional stability and long-term planning certainty.

At the experimental end of the spectrum, Caribbean CBI jurisdictions and El Salvador illustrate two distinct mobility models. In the Caribbean, crypto is treated conservatively as a verified source of wealth within established citizenship programs. El Salvador, by contrast, integrates crypto directly into settlement and fast-track nationality, representing a more direct and higher-risk approach.

The UAE offers the most competitive tax environment among credible jurisdictions: 0% personal income tax, 9% corporate tax, and specialized crypto regulators (VARA in Dubai and FSRA in Abu Dhabi). Combined with long-term residency options, this creates a package that traditional financial centers such as London, New York, and Hong Kong are currently unable to match.

Europe (Germany, the UK, Switzerland, Malta, Estonia) presents a different picture. Harmonised regulation under MiCAR delivers predictability and investor protection, but at the cost of higher compliance burdens and slower innovation. These jurisdictions appeal to participants who prioritize regulatory clarity and legal certainty over speed.

The United States occupies a contrasting position. Despite high adoption, deep liquidity, and strong capital markets, the absence of a comprehensive federal framework and fragmented SEC–CFTC oversight continue to create regulatory uncertainty.

Among emerging markets, Brazil stands out as a partial counterexample. Like Vietnam and Nigeria, it exhibits high adoption driven by retail participation and fintech penetration. Unlike them, Brazil has moved decisively toward regulatory formalization through central bank oversight, clearer tax treatment, and improving compliance standards. This places Brazil closer to institutional compatibility than most high-adoption peers.

Vietnam and Nigeria highlight the opposite dynamic: exceptionally high user adoption alongside limited regulatory maturity. In these markets, crypto usage reflects economic need and behavioral momentum rather than institutional readiness.

- Prioritize regulatory clarity

Choose jurisdictions where digital assets are clearly defined, licensed activities are well understood, and supervision is predictable. Legal certainty is essential for banking access and long-term operations.

- Optimize for institutional use

Focus on environments where crypto can be custodied, reported, and audited without friction. Regulated custody, clear documentation, and credible compliance matter more than retail trading volume.

- Follow tokenization

Tokenization is the main bridge between crypto and traditional finance. Jurisdictions that support tokenized issuance and capital-markets integration are building real digital financial infrastructure.

- Build investment migration in as a safeguard

Residency or second citizenship should be part of the strategy from the start. It provides flexibility to relocate, restructure, and maintain banking continuity if rules change.

As crypto becomes regulated financial infrastructure, jurisdictional choice is risk management. Build in places where crypto can be regulated, banked, and audited—and use investment migration to preserve flexibility if conditions shift.

Thus, this briefing concludes that jurisdictional choice has become a primary strategic variable in cryptocurrency investment, outweighing headline tax rates, adoption metrics, or short-term regulatory arbitrage. As digital assets are progressively embedded into national tax, licensing, and reporting systems, the viability of crypto activity increasingly depends on legal certainty, institutional compatibility, and predictable enforcement rather than permissive or lightly regulated environments.

Other developments highlighted by the analysis point to a structural transition in the crypto industry itself. After a prolonged period of regulatory ambiguity, the scale and economic relevance of digital assets are prompting governments to integrate crypto into the regular financial system, rather than treat it as an exceptional or parallel asset class. The growing role of stablecoins in settlement and payments, alongside the accelerating tokenization of financial assets, reinforces this shift toward infrastructure-level integration, where compliance, custody, and reporting become as important as innovation.

Within this context, investment migration emerges as a distinct strategic pillar. Residency or alternative citizenship is no longer merely a lifestyle or tax consideration, but a legal anchoring mechanism that supports compliant crypto activity. It offers access to different tax and compliance environments, more stable banking relationships, clearer documentation standards, and a legitimate jurisdictional base for both personal and financial life. Because crypto regulation evolves faster than most financial sectors, mobility functions as built-in optionality – the capacity to relocate, restructure, or realign operations in response to regulatory change without disrupting core investment strategy.

The country cases illustrate how these dynamics materialize in practice. Portugal demonstrates how mobility and regulatory alignment can outweigh market scale, attracting crypto investors through EU access and predictable residency-based structuring rather than domestic infrastructure. The United Arab Emirates represents the most fully integrated model, combining low taxation, dedicated crypto regulators, institutional infrastructure, and long-term residency pathways into a coherent relocation and operating environment. Brazil, by contrast, highlights an emerging trajectory in high-adoption markets, where scale is increasingly paired with formal regulatory oversight, positioning it closer to institutional compatibility than many adoption-driven peers.

Looking ahead, the crypto industry is likely to continue moving away from fragmented, jurisdiction-agnostic activity toward geographically anchored digital finance. Tokenization, regulated stablecoins, and deeper integration with capital markets will favor jurisdictions that can support auditability, legal enforceability, and banking connectivity at scale. In this environment, the most resilient strategies will combine credible operating jurisdictions with mobility planning, recognizing that adoption alone does not equal friendliness, and that long-term value creation in digital assets increasingly depends on where crypto can be legally domiciled, supervised, and sustained.

- Financial Stability Board, & International Monetary Fund. (2023). IMF–FSB synthesis paper: Policies for crypto-assets. Financial Stability Board. https://www.fsb.org/uploads/R070923-1.pdf

- Adrian, T., Mancini-Griffoli, T., & Kiff, J. (2025). Understanding stablecoins. International Monetary Fund. https://www.imf.org/-/media/files/publications/dp/2025/english/usea.pdf

- International Monetary Fund. (2025). Crypto-assets monitor. https://www.imfconnect.org/content/dam/imf/News%20and%20Generic%20Content/GMM/Special%20Features/Crypto%20Assets%20Monitor.pdf

- CoinMarketCap. (2025). Bitcoin price historical data — October 6, 2025 to February 10, 2026. https://coinmarketcap.com/currencies/bitcoin/historical-data/

- Deutsche Bank. (2024). Bitcoin sell-off reflects lost conviction, says Deutsche Bank. CoinMarketCap Academy. https://coinmarketcap.com/academy/article/bitcoin-sell-off-reflects-lost-conviction-says-deutsche-bank

- TRM Labs. (2025). 2025 crypto adoption and stablecoin usage report. https://www.trmlabs.com/reports-and-whitepapers/2025-crypto-adoption-and-stablecoin-usage-report

- Chainalysis. (2025). The 2025 global crypto adoption index. https://www.chainalysis.com/blog/2025-global-crypto-adoption-index/

- CoinLedger. (2025). How many people own crypto in the world? https://coinledger.io/research/how-many-people-own-crypto-in-the-world/

- Di Giacomo, M., Rossi, M., & Sekhposyan, T. (2024). Financial literacy, risk tolerance, and cryptocurrency ownership in the United States. Federal Reserve Bank of Kansas City. https://doi.org/10.18651/RWP2024-03

- Social Capital Markets. (2025). Cryptocurrency statistics & demographics. https://socialcapitalmarkets.net/crypto-trading/cryptocurrency-statistics/

- Bank for International Settlements. (2025). Annual economic report 2025. https://www.bis.org/annualeconomicreports/index.htm

- Global Citizen Solutions. (2025). Crypto citizenship. https://www.globalcitizensolutions.com/crypto-citizenship/

- Global Citizen Solutions. (2025). Crypto compliance and citizenship: Where digital assets meet residency planning. https://www.globalcitizensolutions.com/crypto-compliance-and-citizenship-where-digital-assets-meet-residency-planning/

- International Monetary Fund. (2023). [IMF working paper]. https://www.imf.org/-/media/files/publications/wp/2023/english/wpiea2023144-print-pdf.pdf

- Lazea, G., Balea-Stanciu, M., Bunget, O., Sumanaru, A., & Coraș, A. (2025). Cryptocurrency taxation: A bibliometric analysis and emerging trends. International Journal of Financial Studies, 13(1), Article 37. https://doi.org/10.3390/ijfs13010037

- Bhullar, P., Joshi, M., Sharma, S., Phan, D., & Nguyen, A. (2025). Global taxation issues in cryptocurrencies: A synthesis of literature and future research agenda. Journal of Accounting Literature. https://doi.org/10.1108/jal-10-2024-0314

- United Nations. (2015). Manual on the negotiation of bilateral tax treaties between developed and developing countries. https://www.un.org/esa/ffd/wp-content/uploads/2015/09/11STM_Manual_Tax_Treaties.pdf

- Ernst & Young. (2025). Latest rules for digital asset taxation, reporting, and compliance require new processes for 2025. https://taxnews.ey.com/news/2025-2354-latest-rules-for-digital-asset-taxation-reporting-and-compliance-require-new-processes-for-2025

- PwC. (2025). PwC global crypto regulation report 2025. https://legal.pwc.de/content/services/global-crypto-regulation-report/pwc-global-crypto-regulation-report-2025.pdf