The Global Citizenship Programs Index 2026 is a comprehensive comparative assessment of the global investor citizenship landscape. It examines fifteen jurisdictions that, between them, account for the entirety of the world’s active citizenship planning ecosystem: from the Eastern Caribbean programs that defined the category, to the discretionary European routes that have redrawn its upper boundary, to the new entrants in the Pacific, Africa and the Middle East that are reshaping its lower tier.

Investor citizenship is no longer a niche product in the international mobility industry. Over four decades, it has grown into a recognised instrument of sovereign economic policy, generating measurable fiscal contributions, specially for small states, financing post-disaster reconstruction, and serving (for several Caribbean nations in particular) as a structural pillar of national revenue. For the individuals who use these programs, the calculus has likewise evolved. What began as a means of acquiring a second passport for travel convenience has become a multi-dimensional decision involving tax residency, succession planning, business mobility, family security, and increasingly, long-term resilience against geopolitical and climatic risk.

The market has matured, and so has the audience it serves. This maturation is also reflected in how programs themselves are being designed and analysed. The 2026 edition of the Index appears at a moment of clear directional change. Compliance and credibility, once treated as background conditions, are emerging as central determinants of program value. Regional coordination, as we see in the Caribbean region, is replacing fragmented national approaches. In Europe, financial investment is giving way to qualitative contribution, with citizenship increasingly conferred in recognition of sustained value to the host state rather than the completion of a single transaction. Outside the established jurisdictions, a new generation of programs is entering the market, priced for accessibility but tested by the higher governance expectations that now apply across the sector.

Against this backdrop, the Index is designed to do three things. First, to provide a transparent, evidence-based ranking of the fifteen jurisdictions using a consistent five-pillar framework, Procedure, Mobility, Investment, Tax Optimisation and Quality of Life, supplemented by two cross-cutting indicators, Credibility and Compliance, that function as essential markers of program integrity. Second, to make the methodology and underlying data fully auditable, so that investors, advisors, policymakers and journalists can interrogate the findings rather than simply accept them. Third, to situate the rankings within the broader market context, explaining not only how each program performs but why its position is changing, and what the trajectory implies for the year ahead.

This Index is published in the conviction that an industry of this scale and consequence deserves the same standard of analytical scrutiny applied to other instruments of international finance and mobility. Citizenship planning has come of age. The framework presented here is intended to ensure that the way it is measured, compared and understood comes of age with it.

Investment migration is often portrayed as a modern phenomenon, but the principle that citizenship can be acquired in exchange for contribution has deeper roots. As Shachar (2017, pp. 789-816) sets out in her contribution to the topic, naturalization in exchange for monetary or military contribution can be traced to the Roman Republic and to medieval and early modern European city-states. What distinguishes the contemporary industry from these historical precursors is its scale, its institutionalization, and its integration into a global market for legal mobility.

1.1/ The pre-modern foundations

The legal architecture of citizenship as recognised today emerged largely in the nineteenth and twentieth centuries, alongside the consolidation of the modern nation-state. Yet the practice of conferring nationality in exchange for capital or service is far older. As Surak (2023, ch. 1) research, ancient Rome routinely granted citizenship to foreigners providing military service or significant financial contributions, and the Italian city-states of the Renaissance formalised mechanisms to naturalise wealthy foreign merchants whose presence advanced commercial interests. These early arrangements share a common logic with modern citizenship programs: the state exercising sovereign authority over membership in exchange for contribution.

1.2/ The 1984 inflection point: St. Kitts and Nevis and the birth of the modern citizenship programs

The modern investment migration industry traces its origin to a single piece of legislation: the Saint Christopher and Nevis Citizenship Act, 1984 (No. 1 of 1984). Enacted one year after the federation gained independence from the United Kingdom in 1983, Section 3(5) of the Act provided that the Cabinet could register as a citizen any person who had “invested substantially in Saint Christopher and Nevis” (Saint Christopher and Nevis Citizenship Act, 1984). As Surak (2023, ch.2) records, this was the first formal investment migration framework in the world, although in its initial form it remained largely dormant for two decades.

Other Caribbean nations followed.

Belize introduced economic citizenship arrangements through 1985 amendments to the Belizean Nationality Act 1981, with the program formally launched as the Belize Economic Citizenship Investment Program (BECIP) in 1995 (IFC Review, 2017; Briceño, 2023). The program was terminated in January 2002 pursuant to the Belize Constitution (Fourth Amendment) Act 2001, and the underlying legal provisions were repealed by the Belizean Nationality (Amendment) Act 2014.

The Commonwealth of Dominica formalized its program in 1993, and Grenada established its first program in 1996. Regulation during this period was light. Several of these early arrangements were subsequently closed in response to international pressure. The St. Kitts program remained the longest continuously operating framework, even through years of low application volume.

1.3/ The post-2006 professionalization

The St. Kitts and Nevis program transformed from a dormant statutory provision into the global benchmark in 2006–2007, when the government restructured and promoted the program (Abrahamian, 2015, chs. 2 and 4; Surak, 2023, ch. 2). This intervention introduced innovations that have since become standard across the industry: a dedicated Citizenship by Investment Unit, streamlined application procedures, due-diligence standards developed in partnership with specialist compliance firms, and a global marketing footprint. The 2008 global financial crisis was the second major turning point, governments started seeking to attract capital in the wake of the crisis turned increasingly to investment migration as a fiscal and economic recovery instrument (Shachar & Bauböck, 2014).

Most of the current programs were established during or after this period: Cyprus launched its first investor-citizenship framework in 2007 and significantly revised it in 2013, creating the Cyprus Investment Program that served as the model for the modern scheme; Antigua and Barbuda and Grenada followed in 2013; Malta introduced its first formal program in 2013/2014; St. Lucia in 2015/2016; and Türkiye in 2017/2018. Cyprus terminated its program in November 2020 following pressure from the European Commission (Republic of Cyprus, Nikolatos Committee Report, 2021).

1.4/ The investment migration industry

Professor Yossi Harpaz (2019, pp. 15-38) develops the concept of compensatory citizenship: the idea that for individuals from countries with weaker passports or less stable institutions, a second citizenship functions as a form of compensation for the limitations of their original status (Harpaz, Y. & Mateos, P., 2019, p. 849). Harpaz’s empirical fieldwork is grounded in three case studies of non-investment pathways: Israelis acquiring European citizenship by ancestry, Hungarian-speaking Serbs naturalizing in Hungary based on ethnicity, and Mexicans securing US citizenship for their children through strategic cross-border birth (Harpaz, 2019, chs. 2–4, pp. 39–125).

The logic he identifies has also been extended to investor-citizenship, where the similar instrumental drivers such as mobility, opportunity, and insurance against home-country risk, are documented for investor-citizens specifically in Surak’s ethnographic fieldwork across the principal CBI-providing jurisdictions in the Caribbean, the Mediterranean, and the South Pacific (Surak, 2023, ch. 9, pp. 206–247).

It is safe to infer thus that holders of an additional citizenship (whether acquired by ancestry, ethnicity, birth, or investment) not always intend to migrate to or reside in the country concerned. They seek mobility, opportunity, status, and insurance against political and economic risk in their home country (Harpaz, 2019, ch. 1, pp. 15–38; Harpaz & Mateos, 2019, p. 849 and Surak, 2023, ch. 9, pp. 206–247).

The investment migration market has expanded significantly over the past decade. According to market analysis, capital deployed through eleven major residence-by-investment programs rose from about USD 2.86 billion in 2011 to USD 12.4 billion in 2017, representing a compound annual growth rate of 23.4% (IMI Daily, 2019). Including citizenship programs, which IMI Daily estimated generated roughly USD 3 billion in 2017–18, the total investment migration market reached approximately USD 21.4 billion in less than one decade.

Authoritative cumulative data on naturalizations granted through citizenship programs since the launch of the first scheme in 1984 does not exist, since several operating governments do not publish complete annual figures. Surak’s fieldwork-derived estimate places contemporary annual naturalizations at approximately 50,000 individuals globally as of the early 2020s, a figure that, while modest in absolute global terms, marks a substantial reordering of the relationship between citizenship and capital that no theory of citizenship in the twentieth century anticipated (Surak, IMI Daily, 2023; Surak, 2023, ch. 1).

The geography of demand has diversified materially. Surak’s fieldwork identifies three core source regions for citizenship by investment, China and Southeast Asia, Russia and the post-Soviet states, and the Middle East, with smaller but expanding flows from Sub-Saharan Africa and Latin America (Surak, 2023, ch. 9, pp. 206–215).

The demand for a second nationality comes from individuals whose primary citizenship fails to deliver the mobility, opportunity, and security available in higher-ranked countries (Harpaz, 2019, ch. 1, pp. 15–38; Harpaz & Mateos, 2019, p. 849), and among the wealthy specifically, this gap is felt most acutely when democratic institutions at home are weak or eroding.

A similar logic is observed among citizenship and residency programs investors, whose three principal source regions share a common structural feature: substantial private wealth coupled with passports that under-deliver on global mobility. There is an identified pattern that demonstrates that what drives demand is not wealth alone but the asymmetry between wealth and passport strength.

Knight Frank’s Wealth Report 2025 sets the broader frame for where that asymmetry is now emerging. While North America retains absolute dominance in wealth concentration (home to nearly 40% of the world’s HNWIs) Africa is identified as the region “poised to outperform in future wealth creation, in growth, if not in absolute terms” (Knight Frank, 2025, p. 14).

This asymmetry is especially pronounced in Africa.The continent is projected to see its high-net-worth population (US$10m+) grow by 17.8% between 2024 and 2028, from 19,496 to 22,964 individuals, placing it among the fastest-growing wealth regions over the forecast horizon (Knight Frank, 2025, p. 14). Yet the passport these new wealth-holders carry remains, on Global Citizen Solutions’ GPI metrics, structurally underpowered, with the bulk of African nationalities clustered in the lower tiers of the index and only a handful of outliers such as Mauritius and Rwanda showing meaningful progress (Global Citizen Solutions, 2025).

India offers a clearer, more contemporary illustration of this asymmetry. Knight Frank’s Wealth Report 2025 records India as the world’s fourth-largest HNWI population (85,698 individuals worth US$10m+, up 6% in 2024 alone) and the third-largest billionaire wealth pool globally at US$950 billion, behind only the United States and China (Knight Frank, 2025, pp. 14-16). The earlier Wealth Report 2024 projected India’s UHNWI population (US$30m+) to grow by 50.1% between 2023 and 2028, the fastest national growth rate in the world, ahead of China (+47%) and Türkiye (+43%) (Knight Frank, 2024, p. 12). The Indian passport, however, ranks 127th of 199 countries on Global Citizen Solutions’ Global Passport Index, which measures not only travel freedom but the wider envelope of mobility, investment environment and quality of life that wealth-holders weigh when assessing the global value of their primary citizenship (Global Citizen Solutions, 2024). India therefore embodies the wealth–passport asymmetry in its sharpest contemporary form: a globally significant and rapidly expanding pool of private wealth held by households whose primary citizenship materially under-delivers on the mobility, asset-diversification and risk-insurance functions that Harpaz and Surak identify as the structural driver of demand for an additional citizenship (Harpaz, 2019, pp. 15–38; Surak, 2023, pp. 206–215).

Both examples embody scissor pattern visible at different stages of maturity. In India, the gap is already binding: with the world’s fourth-largest HNWI population, third-largest billionaire wealth pool, and a UHNWI cohort projected to grow faster than any other country’s, Indian wealth-holders already encounter daily the passport, investment-environment and lifestyle constraints that domestic wealth alone cannot resolve. In Africa, the same configuration is emerging on a longer time horizon: as the continent’s HNWI population continues to expand through the second half of the decade, a widening share of new African wealth-holders will run into the same structural ceiling , a passport that, on Global Citizen Solutions’ GPI metrics, materially under-delivers on the mobility, investment access and quality-of-life dimensions that wealth would otherwise unlock.

Africa and India cases instantiate a possible configuration as the structural antecedent of compensatory-citizenship demand: substantial private wealth coupled with a primary citizenship whose practical value falls short of what that wealth could otherwise command. Historically, this is the condition under which appetite for an additional citizenship accelerates, specially in the case of investment migration pathways.

1.5/ The international regulatory response

As the industry expanded, so did international scrutiny. The European Parliament adopted its Resolution of 16 January 2014 (2013/2995(RSP)), calling for stricter due diligence on national investor citizenship schemes. This culminated in the European Commission’s Report on Investor Citizenship and Residence Schemes in the European Union (COM(2019) 12 final), which set out concerns about security, money-laundering, tax-evasion and corruption risks, and the need for enhanced transparency and oversight (European Commission, 2019). The OECD raised parallel concerns about the use of citizenship and residency by investment schemes to circumvent the Common Reporting Standard, publishing guidance and a list of high-risk schemes in October 2018 (OECD, 2018).

The most significant international intervention to date is the joint FATF–OECD report Misuse of Citizenship and Residency by Investment Programs, approved by the FATF Plenary on 25–27 October 2023 and published in November 2023. The report concluded that CBI/RBI programs “can help spur economic growth through foreign direct investment” while also identifying specific vulnerabilities and proposed multi-layered due diligence as the central risk-mitigation framework (FATF/OECD, 2023).

Both Malta and the five Eastern Caribbean CBI states moved, over the period 2018–2024, to implement substantial portions of the international recommendations. Malta’s 2020 framework, Citizenship by Naturalisation for Exceptional Services by Direct Investment, introduced a four-tier due-diligence process, a 12- or 36-month residence requirement, a cap on annual applicants and an oath of allegiance. The Eastern Caribbean Five, partly under direct US Treasury and EU pressure and partly through the regional Memorandum of Understanding that would later establish the Eastern Caribbean Citizenship by Investment Regulatory Authority (ECCIRA), raised their minimum contribution thresholds, harmonised enhanced due-diligence standards, expanded biometric and interview requirements, and introduced information-sharing protocols. By the time of the FATF–OECD report, none of the principal Caribbean programs resembled their pre-2018 form.

Despite this compliance trajectory, both groups of programs continued to face judicial and political pressure. In April 2025, the Grand Chamber of the Court of Justice of the European Union ruled in Commission v Malta (Case C-181/23) that Malta’s 2020 framework violated EU law (CJEU, 2025, para. 100). The Court grounded its finding in the principle that the bond of nationality with a Member State is formed by “the special relationship of solidarity and good faith between that State and its nationals” (CJEU, 2025, paras. 96, 99), a doctrinal innovation that several leading EU-law scholars promptly contested.

Writing in Verfassungsblog shortly after the judgment, Dimitry Kochenov (2025) characterised the ruling as “an ultra vires attack against the principle of solidarity,” arguing that the Court had abandoned the liberal conception of EU citizenship developed in Micheletti and Zhu and Chen in favour of an “essentialist” reading in which Member States must police “thick” extra-legal bonds:

“Instead of fighting Member States in the name of a tolerant citizenship ideal and standing up for Europeans’ rights, the Union … now peddles petty nationalisms instead, instructing the Member States that there are citizens ‘in law’ only and also the ‘true’ citizens” (Kochenov, 2025).

In a longer co-authored analysis, Basheska and Kochenov argued that the Court had “abandoned legal reasoning by establishing a thick version of EU citizenship unwarranted by the Treaties, with a solitary reference to ‘solidarity'”, a notion which, in their reading, “has however acquired a new meaning: the construction of a solidarity of thick nationalist identities, policed from Kirchberg at the expense of EU citizens’ status and rights” (Basheska & Kochenov, 2025, p. 1).

Daniel Sarmiento, Professor of EU Law at the Complutense University of Madrid and lead counsel for Malta before the Grand Chamber (CJEU, 2025), has been one of the most consistent critics of the trajectory of EU citizenship jurisprudence in this field. He has argued in the past that the Commission’s case rested on a contested doctrinal premise: that EU law imposes a “genuine link” requirement on Member States in matters of nationality, for which neither the Treaties nor settled case-law provided a textual basis (Sarmiento, 2019). This view aligned with Advocate General Collins’s Opinion of 4 October 2024, which had recommended that the Court dismiss the Commission’s action and held that to find otherwise would “upset the carefully crafted balance between national and EU citizenship in the Treaties and constitute a wholly unlawful erosion of Member States’ competence” (Opinion of AG Collins, 2024, para. 56).

In response to the ruling, Malta moved swiftly to adapt rather than retreat. The Maltese government brought its naturalisation framework into line with the Court’s reasoning and now operates a citizenship by exceptional merit pathway solely, joining Austria’s Section 10(6) route as the principal European model for conferring citizenship in recognition of genuine, sustained contribution rather than predetermined investment.

The 2025 reform repealed the direct-investment limb the Court had ruled against and retained, recalibrated and strengthened the merit limb, which now operates as Malta’s principal pathway for conferring citizenship in recognition of genuine and sustained contribution, in science, entrepreneurship, culture, philanthropy, sport or humanitarian service, rather than a direct economic contribution.

Together, these two frameworks point to where European investor-linked citizenship is heading toward a qualitative, merit-based architecture that is both compatible with EU constitutional principles and capable of continuing to attract individuals whose economic, scientific, cultural or philanthropic contribution genuinely advances the host state.

The Maltese and Austrian models suggest that the future of European citizenship pathways is not closure, but evolution, toward a higher standard that the most resilient programs are already meeting.

1.6/ The four-decade arc

More than four decades after the Saint Kitts and Nevis Citizenship Act, the investment migration industry has matured from a single statutory provision into a global market with fifteen active programs, an estimated USD 20 billion in annual capital flows, and an emerging international regulatory architecture. Three lessons frame the chapters that follow:

- First, demand has proved remarkably durable across economic cycles and geopolitical shifts, suggesting that the underlying drivers (mobility inequality, global risk, and the instrumentalisation of citizenship) are structural features of the international system rather than passing trends.

- Second, the industry’s governance has consistently lagged its growth, with each major regulatory reform arriving after a corresponding scandal, sovereign default, or external intervention.

- Third, programs that have invested in compliance infrastructure ahead of crises (most notably St. Kitts and Nevis, followed by other Caribbean programs) have proved more resilient when international scrutiny intensifies.

This historical perspective frames the empirical assessment of the fifteen active programs that follows.

Scholars such as Dimitry Kochenov and Kristin Surak, argue that investment migration generates measurable contributions for both host states and applicants, and that the contribution is not always economic. Kochenov also claims that these programs are subject to higher scrutiny than virtually any other route to nationality.

2.1/ Rethinking the contribution

The dominant framing of investment migration and citizenship and residency programs in the popular press is transactional: states sell, individuals buy. As Dimitry Kochenov, one of the most-cited contemporary scholars of comparative citizenship law, has argued for over a decade, this framing is both empirically misleading and theoretically impoverished.

Kochenov (2017) argues that the dominant principles by which citizenship is acquired worldwide, jus soli (right of soil) and jus sanguinis (right of blood), are themselves arbitrary. Allocating membership in one of the world’s most consequential legal regimes by accident of birthplace or parentage is, in Kochenov’s terms, the operation of a ‘sacred blood aristocracy principle’ (Kochenov and Basheska, forthcoming 2026). Against that benchmark, jus pecuniae (the acquisition of citizenship through economic contribution) is not less legitimate. It is, arguably, more transparent and more deliberate than the principles it is contrasted with.

“Ideas about what forms the basis of citizenship have constantly evolved. To view it as being purely about ius soli or ius sanguinis is outdated. Why shouldn’t ius pecuniae be among them? Globalization has turned citizenship into a commodity. We help people cross barriers and contribute to the societies of their choice.”

— Professor Dimitry Kochenov, University of Groningen, Faculty of Law. (2017, September)

Writing shortly after the Grand Chamber’s April 2025 judgment in Commission v. Malta, which struck down Malta’s 2020 Citizenship by Naturalisation for Exceptional Services by Direct Investment framework as incompatible with EU law, Kochenov goes further. He argues that the Court’s reasoning rests on an essentialist view of citizenship: one that fails to grasp the realities of twenty-first-century legal and political context, and one that makes a ‘huge disservice to the project of European integration’ (Kochenov, 2025).

The same critique appears in the comprehensive Citizenship and Residence Sales volume edited by Kochenov and Surak for Cambridge University Press (Kochenov and Surak, 2023), which assembles work by legal scholars, economists, sociologists, political scientists, and historians.

The book’s central empirical finding is that, as of 2022, more than a third of all countries in the world offered some path to membership (either citizenship or residency rights) in exchange for a donation or investment, a level of state practice that, in Kochenov’s view, makes wholesale rejection of investment migration legally and analytically untenable.

In sum, granting membership rights in exchange for contribution is not a modern invention; it pre-dates the modern nation-state itself. As Surak (2023, ch. 1) and Džankić (2019) document, ancient Rome conferred citizenship for contribution. What is genuinely modern about contemporary investment migration is not the underlying logic of contribution-based naturalization but its scale, its institutionalization, and its alignment with a world in which capital, talent, and individuals themselves move across borders with a frequency that no twentieth-century model of citizenship anticipated.

In this context, investment migration is the recognition that citizenship has always been awarded in exchange for some form of demonstrable value to the host state, and that aligning that recognition with the realities of an interconnected world of mobile individuals is the legitimate response of sovereign states to a structural feature of the twenty-first century, not a departure from the principles on which citizenship has historically rested.

2.2/ The host-state contribution

Critics often treat the economic case for citizenship by investment as speculative. The data tells a different story. IMF Article IV consultations, an independent PwC audit, and government fiscal reports converge on a consistent picture: in the Eastern Caribbean and the Pacific, well-run CPs have become a material (in some cases dominant) fiscal pillar.

Three findings stand out:

- At the regional level: most rapid expansion of any single revenue category in Caribbean fiscal history

Drawing on IMF research, the Commonwealth Secretariat reports that the citizenship by investment industry in the five-state Eastern Caribbean grew from approximately zero per cent of regional GDP in 2007 to 5.1 per cent of regional GDP by 2015, by orders of magnitude the most rapid expansion of any single revenue category in Caribbean fiscal history (Cover-Kus, 2017). The IMF has subsequently characterised CBI as a valuable countercyclical revenue source for Small Island Developing States, a function it performed visibly during the COVID-19 pandemic, when tourism collapsed and CBI inflows backstopped public finances across the Eastern Caribbean and helped finance reconstruction following the 2017 Atlantic hurricane season. (IMF, 2023, on St. Kitts and Nevis; IMF, 2025, on Dominica).

- At the country level: the figures are extraordinary

Country-level data, drawn directly from IMF Article IV consultations, the 2019 PwC independent audit of the Dominica program, and official government statistics, shows that several CP jurisdictions are now structurally dependent on these flows for fiscal stability and infrastructure development.

Dominica is the most striking case. According to the IMF’s Article IV consultation, CBI revenue reached an unprecedented 37 per cent of GDP in fiscal year 2022/23, a figure the IMF itself describes as evidence of over-reliance (IMF, 2024). This was not a single-year spike. The IMF and PwC together document a steady ascent: 9.5 per cent of GDP in fiscal year 2015/16, 26 per cent of GDP in 2018 following the post-Maria reconstruction surge, 30 per cent of GDP in 2021 during the COVID-19 fiscal emergency, and 37 per cent of GDP in 2022/23 as both pipelines converged (Cover-Kus, 2017; PwC, 2019; Global Financial Integrity, 2022; IMF, 2024).

St. Kitts and Nevis shows a comparably structural pattern over a longer horizon. The IMF’s 2025 Article IV consultation records that recurrent CBI revenue amounted to a cumulative 65 per cent of GDP across 2017 to 2021 (averaging roughly 13 per cent of GDP per year) and reached 25 per cent of GDP in 2022 alone (IMF, 2023). The IMF further confirms that a significant share of these revenues was prudently saved during the pre-pandemic years, reducing public debt below the ECCU regional target of 60 per cent of GDP and supporting the accumulation of large government deposits that financed the country’s COVID-19 response (IMF, 2023). However, the IMF’s 2025 Article IV Consultation with St. Kitts and Nevis, completed in May 2025, documents the most significant single-year decline in CBI revenue in the program’s modern history, and in doing so confirms just how central these programs have become to the fiscal architecture of small island states.

Grenada recorded the strongest single-year revenue performance of any Caribbean CBI program in 2024. The Investment Migration Agency Grenada reported revenues of EC$1.116 billion (approximately USD 412.5 million) making 2024 the second-best year in the program’s history (Caribbean National Weekly, 2025).

Antigua and Barbuda sits at a structurally smaller scale on a percentage-of-GDP basis, but the program is nevertheless central to the country’s fiscal architecture. CIP revenue accounted for approximately 60 per cent of all non-tax government revenue by 2023, while in absolute fiscal terms the IMF 2025 Article IV puts CIP inflows at slightly over 1 per cent of GDP for 2025 (US Department of State, 2023; IMF, 2025a).

Vanuatu, in the Pacific, shows the same pattern outside the Caribbean. Per the IMF’s most recent Country Report, Vanuatu’s CBI revenues moved from 3.7 per cent of GDP in 2017 to a peak of 14 per cent of GDP in 2020, before settling at 7 per cent of GDP in 2024 as governance reforms tightened (IMF, 2025c).

- Where the money has gone: tangible outputs

After Hurricane Maria (which inflicted damages equivalent to approximately 226 per cent of Dominica’s GDP) the Dominican government deployed EC$582.6 million from CBI receipts to fund the island’s recovery (PwC, 2019). The audit records the rehabilitation of fifteen schools, nineteen bridges, fifteen road sections, three hospitals, and six health centres; full funding of 6,680 hurricane-resilient households under Prime Minister Roosevelt Skerrit’s Build Back Better initiative; and direct financing of the Dominica geothermal energy plant and the new Wesley international airport, scheduled for completion in 2026 (PwC, 2019; IMI Daily, 2024). Without CBI inflows, none of these projects would have been financed at the speed or scale at which they were delivered.

Similar evidence exists for St. Kitts and Nevis. St. Kitts and Nevis has, on IMF data, the highest GDP per capita of the Eastern Caribbean Currency Union (approximately USD 18,000 in 2021) a position the IMF attributes in significant part to the sustained, prudently managed CBI inflows of the preceding decade (IMF, 2023).

In Antigua and Barbuda, the National Development Fund and the University of the West Indies Fund are direct CBI-funded mechanisms. In Grenada, the National Transformation Fund channels capital into priority sectors and generated the record EC$1.116 billion in 2024. Across the region, Grenada’s 2024 figure alone exceeded USD 400 million, and combined Eastern Caribbean CBI revenues comfortably exceeded USD 500 million in the same year, financing climate-resilient infrastructure, debt reduction, and the diversification of tourism-dependent economies.

The pattern is consistent across both the Caribbean and the Pacific. Citizenship programs’ revenue, where well-governed, has demonstrably funded reconstruction after catastrophic natural disasters, financed the build-out of climate-resilient infrastructure, reduced public debt, accumulated fiscal buffers for future shocks, and supported diversification of fragile single-sector economies. The international financial institution most often quoted as a sceptic of CBI (the IMF itself) has, in successive Article IV consultations for Dominica, St. Kitts and Nevis, Vanuatu and Antigua and Barbuda, repeatedly recorded this contribution in its own statements.

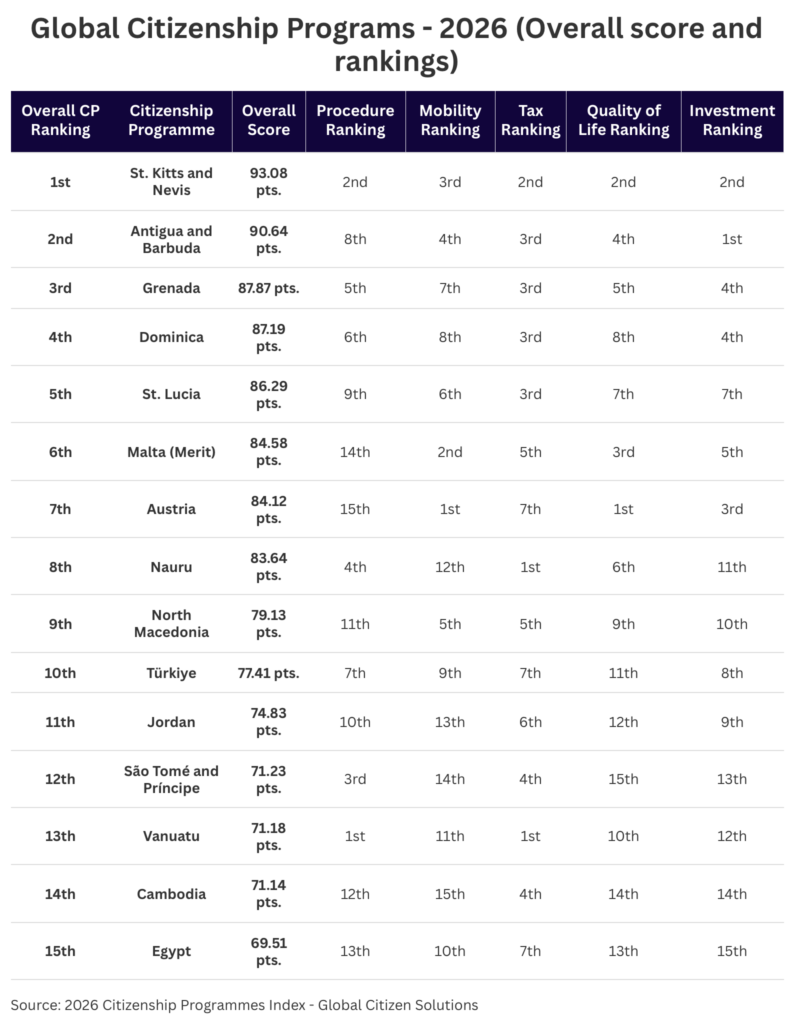

The table below presents the composite ranking of all fifteen active citizenship programs, ordered by Overall Score, with each programs’ individual dimension position.

The Global Citizenship Programs Index 2026 reflects a global investment migration market that has reached a new level of maturity, sophistication and investor choice. Across the 15 active sovereign programs assessed by the Index, applicants now have access to an unprecedented breadth of options spanning four continents, with cost effective entry thresholds and routes that range from streamlined contribution-based programs to bespoke merit-based pathways into the world’s leading economies. The five sub-indexes, Procedure, Mobility, Tax Optimisation, Quality of Life, Investment, capture this diversity and allow each program to be evaluated against the specific objectives of any investor profile. Credibility and Compliance are cross-cutting metrics that also impact programs’ performance.

A defining feature of the 2026 market is that strength is broadly distributed (see map below). Every program in the Index leads or ranks competitively on at least one dimension, and the differentiation between programs increasingly reflects strategic positioning rather than absolute quality. This is good news for investors: where a decade ago the choice was effectively between a handful of similar Caribbean offerings and a small number of European programs, today’s applicants can construct a citizenship strategy tailored to their mobility needs, tax planning objectives, family composition, residency preferences and long-term lifestyle goals.

Source: Global Intelligence Unit – Global Citizen Solutions

St. Kitts and Nevis leads the Index with an overall score of 93.08 points, consolidating its long-standing position as the world’s reference CBI jurisdiction. Its leadership is not built on dominance in any single dimension but on consistency: 2nd on Procedure, 3rd on Mobility, 3rd on Tax, 2nd on Quality of Life and 2nd on Credibility. Antigua and Barbuda follows in 2nd place at 90.64 points, leading the Index on Credibility (1st) and performing strongly on Mobility, Tax and Quality of Life (all 4th), with its only relative weakness being Procedure (8th). Grenada (87.87), Dominica (87.19) and St. Lucia (86.29) complete the top five, an all-Caribbean leadership group separated by less than seven points and characterized by balanced sub-index performance across the board.

The middle of the table introduces a structural break. Malta (Merit) (84.58, 6th) and Austria (84.12, 7th) are the only European programs in the top ten. Both programs are merit-based CPs and requirements are analyzed under the most strict and discretionary procedures. They stand out by exceptional Mobility scores (2nd and 1st respectively) and strong Quality of Life indicators (3rd and 1st). Nauru (83.64, 8th) presents the mirror image: 4th on Procedure, 2nd on Tax and 6th on Quality of Life, but constrained to 12th on Mobility. The three programs share the same band of the table but occupy it for entirely different reasons, a useful illustration of how the weighted composite design rewards different combinations of strengths.

North Macedonia (79.13, 9th) and Türkiye (77.41, 10th) close the upper half. North Macedonia draws strength from its Mobility (5th) as a NATO member and EU candidate, while Türkiye is supported by Procedure (7th) and the scale of its real-estate market. Both score lower on Tax Index (11th and 13th) reflecting their worldwide systems. Jordan (74.83, 11th) is the highest-ranked program outside the top ten, with a balanced profile across all five sub-indexes.

The bottom four places display the widest sub-index dispersion in the Index. São Tomé and Príncipe (71.23, 12th) finishes 3rd on Procedure but 14th on Mobility and 15th on Quality of Life. Vanuatu (71.18, 13th) leads two sub-indexes outright — Procedure (1st) and Tax (1st) — yet finishes only 13th overall because of 11th-place Mobility and 12th-place Credibility (“Investment Ranking” in the chart shorthand). Cambodia (71.14, 14th) and Egypt (69.51, 15th) close the table, with Cambodia weighed down by 15th-place Mobility and Egypt by joint-worst scores on Tax (15th) and Credibility (15th).

Three structural patterns emerge from the overall ranking. First, balance outperforms specialization: every top-five program ranks in the top eight on all five sub-indexes, while every leader on a single sub-index (Vanuatu on Procedure and Tax, Austria on Mobility and Quality of Life, Antigua on Credibility) is positioned outside the top five overall unless that strength is matched by breadth. Second, the Eastern Caribbean bloc dominates the leadership reflecting the maturity, structural similarity and competitive convergence of the OECS CBI programs. Third, the European programs occupy a distinctive position: high passport quality and quality of life, but procedural and fiscal constraints that prevent them from reaching the top of the table. The 23.6-point spread between first (93.08) and last (69.51) is narrower than the underlying sub-index dispersion would suggest, indicating that the weighting structure smooths extreme outcomes.

3.1/ Sub-Index Analysis

3.1.1/ Procedure Sub-Index

The Procedure sub-index measures the accessibility, efficiency and flexibility of the application process. It captures minimum investment thresholds, processing times, residence and language requirements, dual-citizenship rules, and the breadth of investment routes. It is one of the two highest-weighted dimensions of the composite, alongside Mobility.

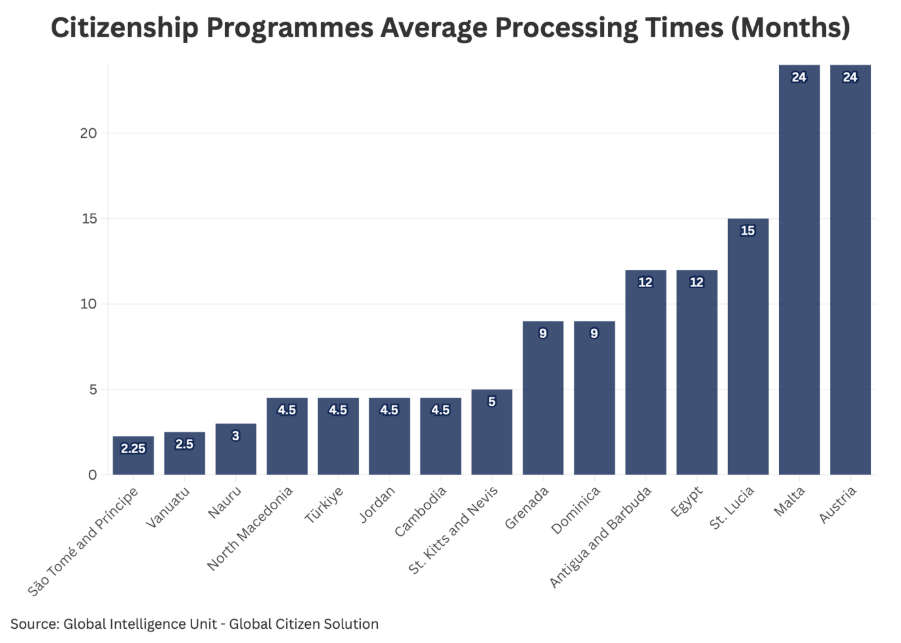

The Procedure ranking is led by Vanuatu (1st), whose 2–3 month processing time and absence of residence or language conditions make it the most operationally efficient program. St. Kitts and Nevis (2nd) is a close second, leveraging its longstanding institutional infrastructure. São Tomé and Príncipe (3rd) and Nauru (4th) round out the top four (both with the lowest minimum thresholds in the Index) followed by Grenada (5th), Dominica (6th) and Türkiye (7th). Antigua and Barbuda is notably absent from the top tier of Procedure (8th), because it requires modest five-day physical-presence obligation and slightly longer processing schedule despite otherwise streamlined operations.

At the bottom of the Procedure ranking, Austria (15th) is the clear outlier: its merit-based, discretionary route under §10(6) of the Austrian Citizenship Act offers no fixed investment amount, no defined timeline and a discretionary approval system, which collectively reduce its procedural score. Malta (Merit) (14th) is similarly constrained by its discretionary structure and 8-month physical-residence requirement. Egypt (13th) and Cambodia (12th) sit just above, reflecting longer processing times and, in Cambodia’s case, a unique Khmer language examination.

Processing times across the 15 citizenship programs span a remarkably wide range: from just 2.25 months in São Tomé and Príncipe to 24 months in Malta and Austria, a tenfold gap that reflects the structural divide between contribution-based and merit-based pathways. The fastest tier (under 5 months) is dominated by streamlined, contribution-driven programs where standardized due diligence enables predictable, expedited approval. A middle cluster of 9 to 15 months groups the remaining Eastern Caribbean programs (Grenada, Dominica, Antigua and Barbuda, St. Lucia) alongside Egypt, reflecting more layered review processes typical of established CBI jurisdictions. At the far end, Malta and Austria’s 24-month timelines stand apart as the signature of merit-based European programs, where discretionary vetting, extensive background checks and case-by-case adjudication trade speed for the prestige of EU citizenship. The pattern reinforces a core finding of the Index: procedural efficiency and passport quality are inversely correlated, and investors effectively choose their position on this trade-off when selecting a program.

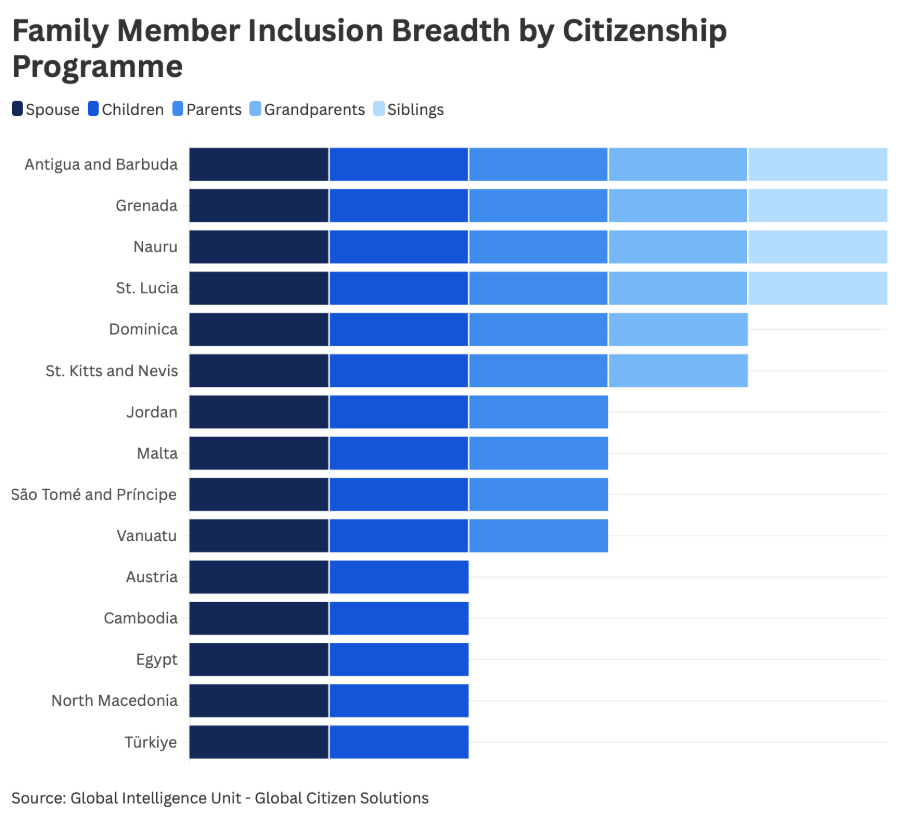

Family inclusion breadth varies sharply across the 15 citizenship programs, revealing another dimension along which applicants must weigh their priorities. At the top end, Antigua and Barbuda, Grenada, Nauru and St. Lucia offer the most expansive eligibility, extending citizenship to all five categories assessed (spouse, children, parents, grandparents and siblings) making them the natural choice for applicants with multigenerational or extended-family considerations. Dominica and St. Kitts and Nevis form a close second tier, covering everyone except siblings, while Jordan, Malta, São Tomé and Príncipe and Vanuatu include up to parents but exclude grandparents and siblings. The pattern highlights a competitive advantage of the Eastern Caribbean bloc: alongside speed and cost efficiency, the breadth of family inclusion is a defining feature of OECS programs and a meaningful differentiator for investors whose strategy centers on securing intergenerational mobility rather than individual relocation.

3.1.2/ Mobility Sub-Index

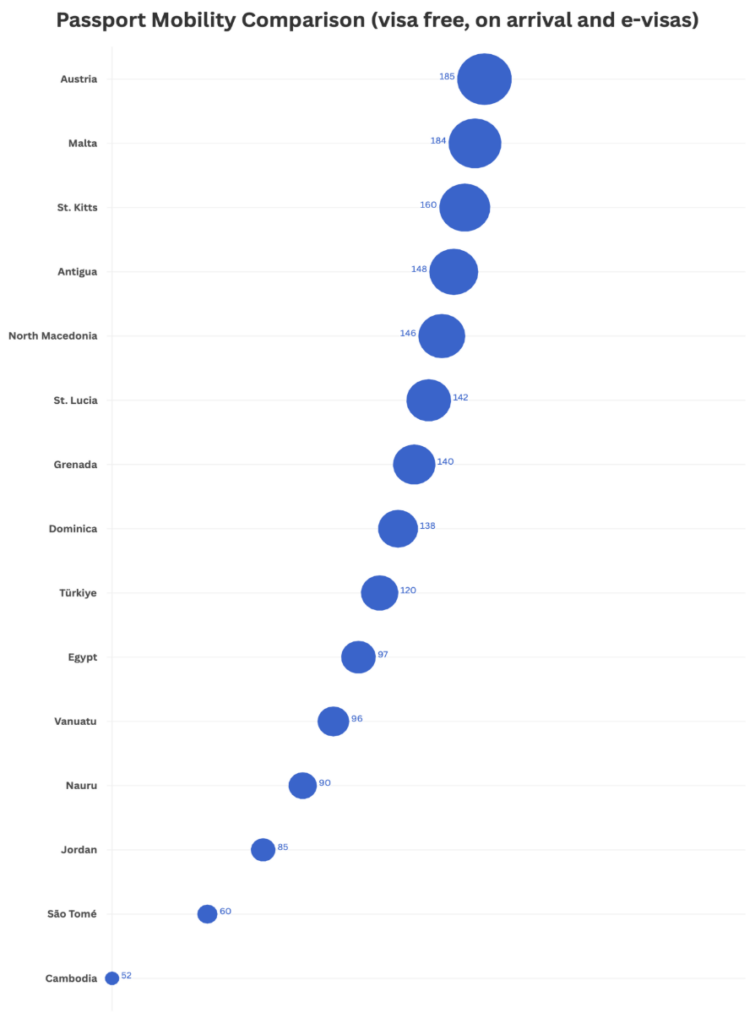

Mobility captures the travel freedom delivered by the passport, measured by the number of destinations accessible visa-free or visa-on-arrival. This dimension is the most strongly correlated with global recognition of the underlying jurisdiction.

The Mobility ranking is led by Austria (1st), whose passport benefits from EU and Schengen membership and ranks at or near the top of all major global passport indexes. Malta (Merit) (2nd) follows, with comparable EU-driven access and retained passport strength even after the April 2025 European Court of Justice ruling. St. Kitts and Nevis (3rd) is the strongest-performing Caribbean passport, ahead of Antigua and Barbuda (4th), North Macedonia (5th), St. Lucia (6th), Grenada (7th), Dominica (8th) and Türkiye (9th). The Mobility ranking is the principal mechanism by which European and leading Caribbean programs outperform the rest of the field on the composite, even when their procedural or fiscal characteristics are uncompetitive.

The lower half of the Mobility ranking is occupied by the Pacific, Middle Eastern and African programs. Egypt (10th) provides intermediate access. Vanuatu (11th), Nauru (12th) and Jordan (13th) sit in a tightly clustered third tier.

The two weakest passports in the dataset are São Tomé and Príncipe (14th) and Cambodia (15th), whose limited visa-free networks are the single largest drag on their overall scores. Mobility is the most volatile of all five sub-indexes, the gap between 1st and 15th is the widest of any dimension, and it is the principal differentiator between programs that compete in the leadership tier and those that do not.

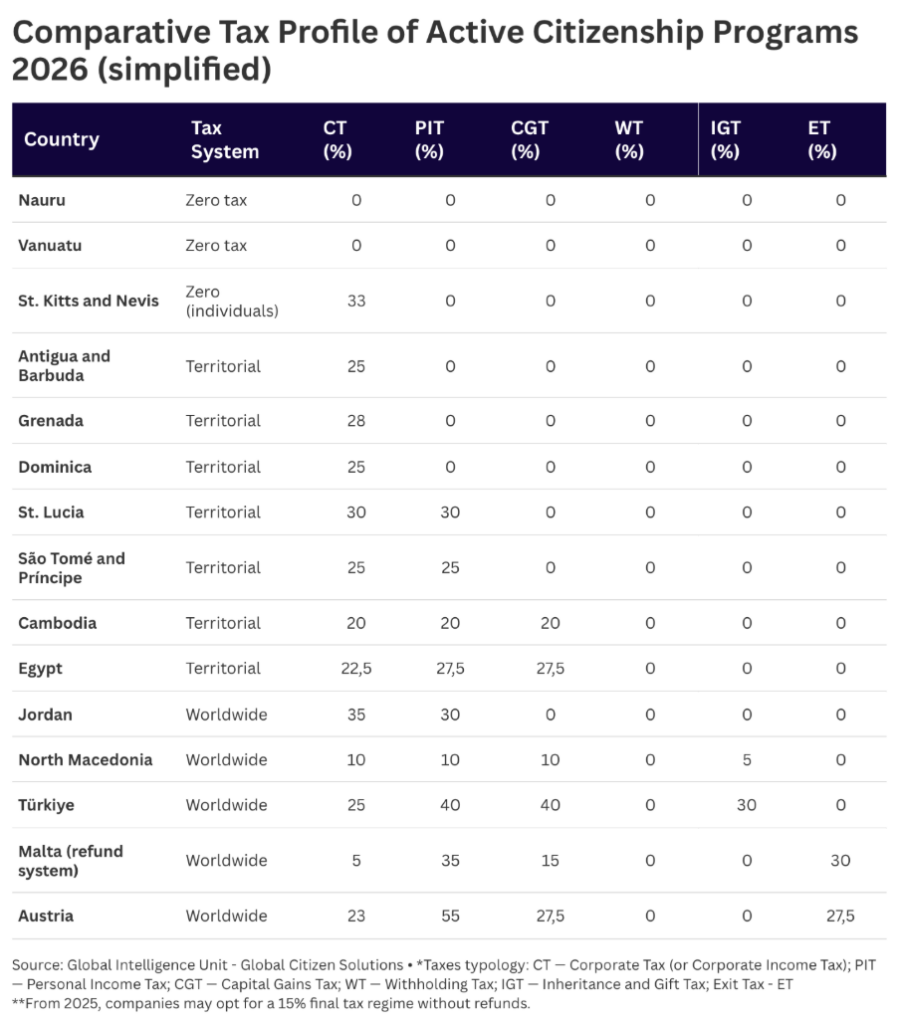

3.1.3/ Tax Optimization Sub-Index

The Tax Optimization sub-index captures the structural attractiveness of the host fiscal regime, combining the tax-system type (zero, territorial or worldwide) with a composite of headline rates for corporate income tax, personal income tax, capital gains tax, wealth tax and inheritance or gift tax.

The Tax ranking is led by Vanuatu (1st) and Nauru (2nd) (the two zero-tax regimes in the Index) followed by St. Kitts and Nevis (3rd), Antigua and Barbuda (4th), Grenada (5th), Dominica (6th) and St. Lucia (7th). The remaining four Caribbean programs share territorial systems with no personal income tax on foreign-source income; their relative positions are determined by corporate rate differentials. Malta (8th) and São Tomé and Príncipe (9th) form an intermediate tier.

At the bottom of the Tax ranking, Austria (14th) and Egypt (15th) operate worldwide tax systems with high headline rates, while Türkiye (13th), Jordan (12th) and North Macedonia (11th) face similar structural challenges.

The Tax sub-index captures a clear strategic trade-off: applicants prioritizing fiscal optimization are directed away from European and Middle Eastern jurisdictions and toward Pacific or Caribbean programs, even where mobility trade-offs apply.

The Comparative Tax Profile reveals a market structured around three clearly delineated fiscal archetypes, each carrying distinct implications for investor strategy. The zero-tax tier, Nauru, Vanuatu and St. Kitts and Nevis (for individuals), offers the cleanest fiscal proposition, with no personal income tax, capital gains, withholding, inheritance or exit tax; St. Kitts is the only program in this group to levy meaningful corporate tax (33%), making it less attractive for operating businesses but equally efficient for individual wealth-holders.

The territorial bloc, comprising the four other Eastern Caribbean programs alongside São Tomé and Príncipe, Cambodia and Egypt, applies corporate tax in the 20-30% range while exempting foreign-sourced income from personal taxation, a configuration that suits globally diversified investors whose income streams sit outside the granting jurisdiction. Within this group, internal differentiation matters: Antigua, Grenada and Dominica preserve full 0% personal taxation, while St. Lucia, São Tomé, Cambodia and Egypt apply meaningful PIT on locally-sourced income, narrowing their appeal for residents. The worldwide tier shows the widest internal dispersion of any group in the Index: North Macedonia’s flat 10% across CT, PIT and CGT is among the most competitive global-income regimes anywhere, while Austria sits at the opposite extreme with 55% PIT, 27.5% CGT, and an individual exit tax, the heaviest combined burden in the dataset. Türkiye is the standout case for inheritance planning concerns, being the only program outside Austria to apply meaningful taxes on capital gains (40%) and the only one to levy inheritance and gift tax at a 30% upper bound.

Two cross-cutting findings reinforce the structural argument of the broader Index: withholding tax is uniformly zero across all 15 programs, eliminating a common friction point for cross-border income flows; and exit taxes are confined to Malta (corporate) and Austria (individual), making them a distinctly European phenomenon tied to OECD anti-avoidance alignment. The overall picture confirms that fiscal attractiveness and passport quality move in opposite directions — the lightest tax regimes cluster among the weaker-passport jurisdictions, while the strongest European passports come bundled with the heaviest fiscal exposure — meaning tax positioning functions less as a standalone selection criterion than as one axis of an integrated trade-off that every investor must price into their citizenship strategy.

3.1.4/ Quality of Life Sub-Index

Quality of Life is one of the five dimensions assessed in the 2026 Global Citizenship Programs Index, and it carries particular weight for applicants whose citizenship strategy includes the option of relocation, family establishment, or extended periods of physical residence in the host state. To anchor the Index’s findings against an external, independently constructed benchmark, this section cross-references the 2026 Citizenship Programs Index Quality of Life sub-index with the Global Citizen Solutions Global Passport Index 2025, a separate ranking of 197 sovereign jurisdictions evaluated across six Quality of Life indicators: sustainable development, cost of living, level of happiness, personal freedoms, environmental performance, and migrant acceptance. The convergence between the two indices is substantial, and the alignment provides external validation of the Index’s analytical framework.

Austria is the highest-scoring jurisdiction in the entire fifteen-program index, with a Quality of Life score of 83.65, ranking 14th globally on the GPI 2025 against 197 sovereign jurisdictions. This is consistent with Austria’s structural advantages: the highest human development indicators in the index, comprehensive universal healthcare, the highest safety scores, and a passport that benefits from full EU and Schengen membership. Austria’s §10(6) merit pathway under the Staatsbürgerschaftsgesetz, while functionally accessible only to a narrow cohort of UHNW applicants whose contribution case is compelling on its own terms, delivers a quality-of-life experience that no other program in the index can match.

Malta is the second-strongest performer at 77.65 (global rank 32). Even after the April 2025 CJEU ruling restructured Malta’s citizenship framework into the discretionary merit pathway under Article 10(9), the underlying jurisdiction retains its quality-of-life advantages: EU membership, Schengen access, a Mediterranean lifestyle, English as an official language, and a healthcare system consistently ranked among the strongest in southern Europe.

The third-highest Quality of Life score in the dataset belongs not to a Caribbean program but to Nauru, at 72.57 (global rank 48). Nauru is a small Pacific island state with limited infrastructure, modest per-capita income, and existential exposure to climate risk, but it reflects the specific way the GPI 2025 weights its Quality of Life indicators. Nauru scores well on environmental performance metrics, on personal freedoms within its political system, and on the demographic and social-fabric indicators captured by the migrant-acceptance dimension. Whether this score is sustainable over a longer time horizon, as climate exposure intensifies and as the program attracts a more diverse applicant pool, is an open question.

The defining feature of the Caribbean group on this dimension is structural similarity rather than competitive differentiation. The five OECS programs occupy GPI 2025 ranks 54 through 70, with scores between 67.13 (Grenada) and 70.78 (Dominica). The internal order — Dominica, St. Lucia, St. Kitts and Nevis, Antigua and Barbuda, Grenada — reflects modest differences in the underlying sub-indicators rather than fundamental divergence in the lived experience of citizenship. Caribbean Quality of Life is shaped by the same regional features across all five: tourism-driven service economies, English as an official language, common-law legal systems, low population density, sub-tropical climate, and proximity to the United States and Canada for healthcare and education access. The Caribbean Five sit firmly in the middle of the global Quality of Life distribution, above São Tomé, Türkiye, Jordan, Egypt, and Cambodia, but well below the European leaders. For applicants whose primary use of the citizenship is mobility and optionality rather than relocation, this middle-tier positioning is more than sufficient; for applicants who intend to relocate physically, the lifestyle proposition is materially different from what an EU or Austrian passport would deliver.

For the segment of applicants whose strategy does include eventual relocation, family establishment in the host state, or extended periods of physical residence, Quality of Life becomes the most consequential of the five dimensions. The data clarifies the trade-off: applicants for whom this dimension matters most should concentrate their decision-making on Austria and Malta first, on Nauru and the Caribbean Five second, and approach the lower-tier programs only where their primary objective is something other than the lived experience of residence.

3.1.5/ Investment Sub-Index

The Investment sub-index used in the Global Citizenship Programs Index 2026 is drawn from the Investment dimension of the Global Passport Index, ensuring methodological continuity across our flagship products and giving applicants a consistent, transparent measure of economic destination quality. For citizenship programs specifically, the dimension is particularly well-suited: it captures the after-tax economic environment a new citizen would actually face, which is precisely the question most applicants are trying to answer when comparing jurisdictions.

The composite combines three indicators: the Global Innovation Index (50%), GNI per capita (25%) and the headline personal income tax rate (25%). Together they proxy the long-term economic platform each program offers, innovation capacity as a forward-looking signal of dynamism, GNI as a measure of prosperity, and personal taxation as the most direct lever shaping an individual investor’s net return.

The ranking rewards exactly what the citizenship investor values most. Vanuatu and the Eastern Caribbean programs combine zero or near-zero personal taxation with stable, well-governed economies, producing a fiscal environment that maximises the net economic value of citizenship for globally mobile individuals. Malta and Austria, while institutionally deeper, are penalised on the tax component (55% and 35% top personal rates respectively), a trade-off that applicants in those programs consciously accept in exchange for EU passport quality and access to one of the world’s most integrated economic blocs.

Two structural patterns reinforce the broader Index narrative. First, the Investment sub-index runs almost inversely to Mobility, confirming that programs have differentiated themselves along genuinely opposing economic axes and that investors face a real choice rather than a quality gradient. Second, the Eastern Caribbean bloc’s tight clustering between 84 and 87 points reflects the underlying convergence of OECS economies, a sign of the maturity and consistency of the regional CBI model.

3.2/ Regional overview

3.2.1/ The Caribbean: the modern benchmark

Five Eastern Caribbean nations dominate the top of the 2026 ranking, occupying ranks 1 through 5 and accounting for roughly 90 per cent of CBI applications globally (European Commission, 2024; Astons, 2025). Their collective strength rests on four pillars: efficient processing (4–14 months), competitive minimum investments (USD 200,000–250,000), no residency requirements, and strong passport mobility.

The 2024 Memorandum of Understanding among the five governments has fundamentally upgraded the regional value proposition. ECCIRA, headquartered in Grenada and ratified in October 2025, now serves as a centralized regulator with powers to license agents, publish reports, impose penalties, and revoke permits.

Each of the five programs occupies a distinct strategic niche: St. Kitts and Nevis remains the prestige benchmark; Antigua and Barbuda offers the broadest family inclusion globally; Grenada is uniquely positioned for US business access via the E-2 Treaty; Dominica provides the lowest entry threshold in the region; and St. Lucia uniquely offers a refundable government bond route.

3.2.2/ Europe: the post-Malta landscape

Europe’s CP footprint has been dramatically reshaped. Malta’s MEIN program was effectively terminated by the April 2025 CJEU ruling. Malta retains a discretionary Citizenship by Merit (CBM) framework. This operates on a case-by-case basis with no fixed price tag and is not comparable to the structured CBI programs elsewhere in this report.

Austria’s Section 10(6) pathway under the Citizenship Act remains the only direct route to EU citizenship through extraordinary contribution, though it is functionally inaccessible: no published threshold, no application form, multi-year processing, and an estimated USD 3 million entry cost.

North Macedonia provides the most affordable European-passport route at USD 200,000, with NATO membership and EU candidate status conferring partial European mobility.

3.2.3/ Other regions: cost-conscious and strategic alternatives

Outside Europe and the Caribbean, eight programs (Türkiye, Jordan, Egypt, Cambodia, Vanuatu, Nauru, and São Tomé and Príncipe) form a heterogeneous group serving cost-conscious investors and those with specific regional ties.

Türkiye operates the highest-volume citizenship program globally; Jordan offers a stable Middle Eastern hub; Egypt provides multiple routes including a refundable treasury certificate option. Vanuatu remains the fastest CBI globally but carries significant compliance risk. Nauru and São Tomé and Príncipe are tied as the cheapest CBI programs globally.

The investment migration industry stands at the most significant inflection point since its modern emergence in the mid-1980s. The convergence of three forces, the post-Malta legal ruling, the operationalization of the FATF/OECD compliance framework, and the rapid maturation of digital identity technology, is driving a structural transformation in how programs are designed, applicants are vetted, and citizenship is granted.

4.1/ The phasing out of price-driven competition

The first and most visible trend is the systematic phasing out of price-driven competition. The March 2024 Memorandum of Understanding among the five Eastern Caribbean nations explicitly committed signatories to harmonized minimum investment thresholds and prohibited what regional officials called ‘underselling and illegal discounting’ (Caribbean News Global, 2025). St. Kitts and Nevis raised its threshold to USD 250,000 in 2023 ahead of its peers, and the rest of the region followed in mid-2024.

This shift reflects a deeper repositioning. As the OECS heads of government noted in their September 2025 communiqué establishing ECCIRA, the strategic priority is to ‘protect external market access, avoid sanctions or visa suspensions, and position [the region] as a premium, reputationally resilient second-citizenship option’ (CEOWORLD, 2026). The economic logic is straightforward: the value of a Caribbean passport depends entirely on its visa-free access to the EU, the UK, and major Asian financial hubs. Below a certain price point, programs generate volume that exceeds the carrying capacity of due diligence systems, and reputational damage propagates across the region. The race to the bottom has ended.

4.2/ The reintegration of residency requirements

Perhaps the most consequential trend is the reintroduction of physical-presence requirements into traditionally residency-free programs. In late 2025, St. Kitts and Nevis announced that 2026 reforms will require applicants to demonstrate physical presence as part of their eligibility, the first time in the program’s forty-year history (CEOWORLD, 2026). This responds directly to the European Commission’s growing emphasis on ‘genuine link’ as a precondition for visa-free access, and to the underlying logic of the CJEU’s Malta judgment, which held that nationality decoupled from a deeper bond of integration is incompatible with EU treaty obligations (Court of Justice of the European Union, 2025).

The implications are significant. The defining feature of the Caribbean CBI value proposition since 2006 has been remote applicability, citizenship without relocation. As more programs adopt residency obligations, the differentiation between CBI and traditional Residence by Investment (RBI) routes will narrow. Saint Vincent and the Grenadines, which is preparing to launch a CBI program in 2026, has already signaled that ECCIRA-aligned standards including residency requirements will form part of its design.

4.3/ The mainstreaming of biometric due diligence

The November 2023 FATF/OECD report has had a transformative effect on program design. The report identified ‘multi-layered due diligence’ as the central risk-mitigation framework and recommended biometric collection, mandatory applicant interviews, source-of-wealth verification (in addition to source-of-funds), and continuous monitoring of approved beneficiaries (FATF/OECD, 2023). St. Kitts and Nevis began rolling out fingerprint and facial-recognition biometric collection for all CBI applicants in April 2026, with new ePassports to be issued from July 2026 (Hamilton Trust Company, 2026).

ECCIRA-aligned programs are expected to route security checks through CARICOM IMPACS and the Joint Regional Communications Centre (JRCC), creating a shared regional security backbone (Armenian Lawyer, 2026). The operational consequences are substantial: applicants will face longer onboarding processes, advisors will need to manage biometric appointments and consent disclosures, and authorized agents will be subject to centralized licensing. The Investment Migration Council (IMC, 2024) has noted that these requirements will ‘compress differentiation around risk standards rather than just price’, a market structure in which compliance quality, not cost, becomes the primary axis of competition.

4.4/ Citizenship programs: from passive contribution to active, merit-based contribution

As mentioned, the architecture of citizenship programs is undergoing the deepest transformation in the sector’s modern history. In some regions, the post-2025 regulatory landscape has decisively pivoted toward active contribution, demonstrable economic value, and alignment with national strategic priorities.

The trigger for the most consequential change in citizenship policy this decade was the Court of Justice of the European Union’s judgment of 29 April 2025 in Commission v. Malta (Case C-181/23). With this ruling, the country no longer offers any direct citizenship-by-investment route

The replacement framework is instructive. Malta Citizenship by Merit now operates under Article 10(9) of the Maltese Citizenship Act (Chapter 188) and is implemented through Subsidiary Legislation S.L. 188.06 (Legal Notice 159 of 2025). This framework replaced Malta’s former citizenship-by-investment program following the Court of Justice of the European Union ruling in April 2025. The framework is explicitly not an investment program: future access to Maltese nationality prioritizes merit-based contributions with “added value” and job creation rather than upfront payments (Government of Malta, 2025). Discretionary naturalization now hinges on demonstrable contribution in fields such as science, technology, innovation, culture, philanthropy, humanitarian work, or entrepreneurship, categories that map directly onto SDG 8 (decent work and economic growth), SDG 9 (industry, innovation and infrastructure), and SDG 17 (partnerships for the goals).

Malta’s reconstituted program is the newest expression of an older European tradition that Austria has maintained for decades. According to Article 10(6) of the Austrian Citizenship Act (Staatsbürgerschaftsgesetz), citizenship is awarded based on the extraordinary services performed by foreigners in the past and the expectation of extraordinary services that will be performed in the future. Crucially for the post-CJEU environment, the Austrian model has always rejected the passive-capital logic. Under the citizenship by merit provisions, an applicant is required to invest actively in the Austrian economy, for example, in the form of a joint venture or direct investment in a business that creates jobs or generates new export sales. Alternatively, citizenship may be granted for extraordinary achievements that serve Austria’s national interest, such as outstanding contributions in sports, science, the arts, or philanthropy (Government of Austria, Citizenship Act §10(6)).

Austria’s Citizenship by Merit is a special pathway that allows the Austrian government to grant citizenship to individuals who make extraordinary contributions to the nation. Qualifying contributions include major direct investments that generate jobs and tax revenue, and significant donations to public-interest projects in areas such as the arts, science, education, or research.

Regarding CPs outside the European Union, the architecture is being recalibrated along similar lines. Passive routes are being narrowed, while active and SDG-aligned routes are preserved or expanded.

The Memorandum of Agreement dated of March 2024 established a Regional Regulator and a shared due-diligence framework. Dominica’s Economic Diversification Fund has channeled program revenue into geothermal energy development and post-Hurricane Maria reconstruction, explicitly linking citizenship contributions to SDG 7 (affordable and clean energy) and SDG 13 (climate action).

Nauru’s National Prosperity Fund, launched in 2024, is structured around climate-resilience financing, making it the first citizenship program designed around an explicit SDG-13 thesis. Program proceeds are ring-fenced for adaptation infrastructure in a jurisdiction facing existential climate exposure (Government of Nauru, 2024).

Egypt’s citizenship route, structured around refundable treasury certificates returnable after three years, aligns program design with sovereign capital management rather than donation-based revenue extraction, a model that connects citizenship to SDG 17.1 (strengthening domestic resource mobilization) (Government of Egypt, Law No. 190/2023).

Jordan’s 2025 reforms eliminated passive bank deposit and treasury bond routes in favor of active job-creation pathways requiring sectoral investment and demonstrable employment thresholds, anchoring citizenship eligibility directly to SDG 8.5 (productive employment and decent work for all) (Government of Jordan, 2025).

As Surak (2023) anticipated, citizenship is increasingly being deployed as “an instrument of statecraft” rather than passive capital attraction, and the post-CJEU European environment has accelerated that shift from a trend into a regulatory baseline that is now reshaping program design globally.

4.5/ The convergence with talent, innovation, and merit pathways

The recalibration of citizenship around merit, contribution, and demonstrable national value points to where citizenship policy is ultimately heading. The credible long-term proposition for any citizenship pathway tied to economic contribution will require some combination of:

(i) genuine economic contribution beyond passive donation, typically expressed through job creation, research and development commitment, sectoral investment with employment thresholds, or active enterprise that produces measurable national value (SDG 8, SDG 9);

(ii) demonstrable governance integrity, validated by independent third parties and aligned with FATF/OECD (2023) due diligence standards, including enhanced source-of-funds verification and beneficial ownership transparency (SDG 16);

(iii) a genuine link with the host state, expressed through actual residence, language acquisition, civic knowledge, or sectoral participation — now a constitutional requirement under EU law following CJEU (2025) in Case C-181/23, and an emerging norm in non-European citizenship frameworks responding to international compliance pressure;

(iv) alignment with broader national and global development priorities, particularly the Sustainable Development Goals concerning decent work (SDG 8), innovation and industrial upgrading (SDG 9), climate resilience (SDG 13), and the mobilization of resources for sustainable development (SDG 17).

The European experience demonstrates that this is no longer a forward-looking aspiration. It is the operating framework. Citizenship programs that fail to meet these conditions are being restructured, or absorbed into discretionary merit pathways.

Those that successfully reposition themselves around active contribution and SDG-aligned outcomes are emerging as the new template for how sovereign states engage with mobile capital and talent in the post-2025 era.

4.6/ Anticipating the next decade

Looking forward, four developments appear most likely:

- Regulatory convergence around international standards. ECCIRA’s full operationalization in 2026 will likely become the template for regional CBI regulators in other jurisdictions. The FATF will integrate CBI/RBI assessment into its next-round mutual evaluation methodology beginning in 2026 (FATF, 2025), making program governance directly relevant to a country’s overall AML rating.

- Technology-mandated compliance. AI-powered transaction monitoring, automated KYC, and real-time sanctions screening are becoming regulatory expectations rather than competitive differentiators (Moody’s, 2025). Programs without sophisticated technology infrastructure will progressively lose access to international banking partners.

- Multi-jurisdictional citizenship portfolios. Ultra-high-net-worth families are increasingly building diversified mobility portfolios combining citizenship, residence, and digital access rights across multiple jurisdictions. The single ‘best program’ framework is giving way to ‘best portfolio combination’ analysis.

- ESG integration. Environmental, social, and governance criteria are no longer optional. Real estate investments must increasingly meet sustainability standards, and government-fund options are shifting toward climate adaptation and social development (FTN News, 2025). High-net-worth applicants under fifty consistently prioritize sustainability when selecting programs, a generational shift that will reshape demand patterns.

The cumulative effect of these forces is a more mature, more regulated, and ultimately more credible investment migration sector. The cheapest, fastest, lightest-touch programs of 2015 are being systematically displaced by structured platforms with biometric verification, residency obligations, sectoral investment requirements, and regional regulatory oversight. For investors, this means higher costs and longer timelines but also greater predictability, durability of citizenship rights, and reputational protection. For the industry, it means a transition from a product to an institutional service.

Citizenship planning has come of age. The conversation that defined the industry a decade ago, which program to invest on? at what cost? in what timeframe? has been displaced by a fundamentally different question: how a family’s mobility, fiscal, and security exposure should be structured across multiple jurisdictions over a generational horizon?

Citizenship is no longer the deliverable. It is one component within a coordinated portfolio that includes tax residency, asset structuring, family planning, and jurisdictional diversification, and life choices designed to deliver specific outcomes as regulatory conditions and geopolitical circumstances evolve. The most sophisticated clients in the 2026 market construct their citizenship strategies in this layered way: a primary citizenship as the core mobility instrument, a secondary citizenship addressing a specific objective the primary cannot fulfil, strategic tax residencies, and long-term elective pathways positioned for the next generation.

Compliance and credibility have surpassed cost and processing speed as the primary axes on which programs are judged and selected. Programs that meet this baseline proactively will retain the visa-free EU, UK, and major Asian access on which their value depends.

The future of citizenship programs belongs to those that meet this convergent standard: compliance infrastructure aligned with the FATF/OECD framework, credibility anchored in transparent governance and demonstrable national contribution, and investment options aligned with measurable development outcomes.

The industry is moving, in short, from product to institutional service, and the families, programs, and advisors who recognise this and adapt accordingly will define what investor citizenship looks like in the decade ahead. The world is becoming more uncertain, not less. The Global Citizenship Programs Index 2026 documents an industry that has matured, often under pressure, to meet that uncertainty. The decisions that follow from this Index matter not because they are about passports, but about how families construct durable resilience across jurisdictional, fiscal, and geopolitical risk in a world where the assumption of stability is itself a source of risk. That is the conversation investor citizenship now exists to support, and the standard against which every program in this Index will be measured in the years to come.

References

Academic Books and Journal Articles

Abrahamian, A. A. (2015). The cosmopolites: The coming of the global citizen. Columbia Global Reports.

Bauböck, R. (2014). Cash-for-passports and the end of citizenship. In A. Shachar & R. Bauböck (Eds.), Should citizenship be for sale? (pp. 19–21) [EUI Working Paper RSCAS 2014/01]. European University Institute. https://cadmus.eui.eu/handle/1814/29318

Basheska, E., & Kochenov, D. V. (2025). A successful attempt to hijack the Union’s liberal promise [SSRN Working Paper No. 6466803]. Forthcoming in Nordic Journal of European Law, 2026. https://doi.org/10.2139/ssrn.6466803

Carrera, S. (2014). The price of EU citizenship: The Maltese citizenship-for-sale affair and the principle of sincere co-operation in nationality matters. Maastricht Journal of European and Comparative Law, 21(3), 406–427. https://doi.org/10.1177/1023263X1402100302

Harpaz, Y. (2019). Citizenship 2.0: Dual nationality as a global asset. Princeton University Press. https://doi.org/10.23943/princeton/9780691194066.001.0001

Harpaz, Y., & Mateos, P. (2019). Strategic citizenship: Negotiating membership in the age of dual nationality. Journal of Ethnic and Migration Studies, 45(6), 843–857. https://doi.org/10.1080/1369183X.2018.1440482

Kochenov, D. V. (2014). Citizenship for real: Its hypocrisy, its randomness, its price. In A. Shachar & R. Bauböck (Eds.), Should citizenship be for sale? [EUI Working Paper RSCAS 2014/01]. European University Institute. https://cadmus.eui.eu/handle/1814/29318

Kochenov, D. V. (2025, May 5). EU citizenship’s new essentialism: The solidification of the illiberal union. Verfassungsblog. https://verfassungsblog.de/eu-citizenships-new-essentialism/https://doi.org/10.59704/452e3eca733be6a5

Kochenov, D. V., & Surak, K. (Eds.). (2023). Citizenship and residence sales: Rethinking the boundaries of belonging. Cambridge University Press.

Shachar, A. (2009). The birthright lottery: Citizenship and global inequality. Harvard University Press.

Shachar, A. (2017). Citizenship for sale? In A. Shachar, R. Bauböck, I. Bloemraad, & M. Vink (Eds.), The Oxford handbook of citizenship (pp. 789–816). Oxford University Press. https://doi.org/10.1093/oxfordhb/9780198805854.013.34

Surak, K. (2016). Global citizenship 2.0: The growth of citizenship by investment programs [IMC Research Paper 2016/3]. Investment Migration Council. https://investmentmigration.org/wp-content/uploads/2020/10/Surak-IMC-RP3-2016.pdf

Surak, K. (2023). The golden passport: Global mobility for millionaires. Harvard University Press. https://doi.org/10.4159/9780674294738

International Organization Reports and Primary Legal Documents

Council of the European Union. (2022, March 3). Council Decision (EU) 2022/366 on the partial suspension of the application of the Agreement between the European Union and the Republic of Vanuatu on the short-stay visa waiver. Official Journal of the European Union, L 69, 105–106. https://eur-lex.europa.eu/eli/dec/2022/366/oj

Court of Justice of the European Union. (2025, April 29). Judgment of the Court (Grand Chamber), European Commission v. Republic of Malta, Case C‑181/23. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:62023CJ0181

Court of Justice of the European Union. (2024, October 4). Opinion of Advocate General Collins, European Commission v. Republic of Malta, Case C‑181/23 [Press Release No. 165/24]. https://curia.europa.eu/

European Commission. (2019). Investor citizenship and residence schemes in the European Union: Report from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions [COM(2019) 12 final]. https://commission.europa.eu/strategy-and-policy/policies/justice-and-fundamental-rights/democracy-eu-citizenship-anti-corruption/eu-citizenship/investor-citizenship-schemes_en

European Parliament. (2014, January 16). Resolution of 16 January 2014 on EU citizenship for sale [2013/2995(RSP)]. Official Journal of the European Union, C 482, 117–118 (23.12.2016). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52014IP0038

FATF/OECD. (2023, November). Misuse of citizenship and residency by investment programs. Financial Action Task Force and OECD. https://doi.org/10.1787/ae7ce5fb-en https://www.fatf-gafi.org/content/dam/fatf-gafi/reports/Misuse-CBI-RBI-Programs.pdf.coredownload.pdf

Financial Action Task Force. (2023, October 27). Outcomes FATF Plenary, October 2023. https://www.fatf-gafi.org/en/publications/Fatfgeneral/outcomes-fatf-plenary-october-2023.html

FATF/OECD. (2023, November). Misuse of citizenship and residency by investment programmes. Financial Action Task Force and OECD. https://doi.org/10.1787/ae7ce5fb-en

Global Financial Integrity. (2022). Citizenship by investment programs in the Caribbean: Trends and risks. https://gfintegrity.org/

International Monetary Fund. (2021). Dominica: 2021 Article IV Consultation — Press Release; Staff Report; and Statement by the Executive Director for Dominica [IMF Country Report No. 21/182]. https://www.imf.org/en/-/media/files/publications/cr/2021/english/1dmaea2021001.pdf

International Monetary Fund. (2022, February 14). IMF Executive Board concludes 2021 Article IV Consultation with Dominica [Press Release No. 22/35]. https://imf.org/en/News/Articles/2022/02/14/pr2235-imf-executive-board-concludes-2021-article-iv-consultation-with-dominica

International Monetary Fund. (2023, March 31). St. Kitts and Nevis: 2023 Article IV Consultation — Press Release; Staff Report; and Statement by the Executive Director for St. Kitts and Nevis [IMF Country Report No. 23/130]. https://www.imf.org/en/Publications/CR/Issues/2023/03/31/St-Kitts-and-Nevis-2023-Article-IV-Consultation-Press-Release-Staff-Report-Informational-531625