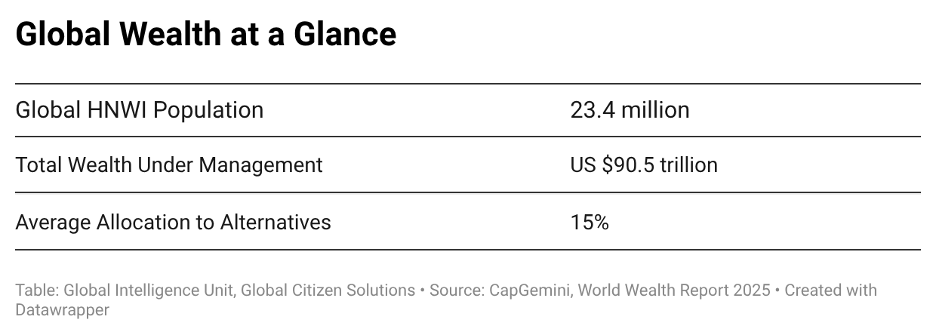

Global private wealth is expanding in scale and complexity. The High-Net-Worth Individuals (HNWI) global population now numbers over 23 million (Capgemini, 2025) and an unprecedented intergenerational wealth transfer is underway. These developments are not isolated trends: they reflect structural changes in how capital is accumulated, managed, and geographically distributed.

Historically, portfolio construction for wealthy investors was primarily concerned with balancing risk and return across financial assets. The classic stock–bond framework, grounded in Harry Markowitz’ modern portfolio theory, emphasized diversification across asset classes within relatively stable economic and political environments. Over time, however, this model has evolved. Contemporary portfolios increasingly incorporate private markets, real assets, and other alternative investments to capture illiquidity premia, diversify return drivers, and reduce dependence on public market cycles.

At the same time, a new dimension of risk has become increasingly relevant to wealth preservation: sovereign risk. Rising geopolitical fragmentation, regulatory divergence, fiscal pressures, and shifting policy environments have elevated the importance of geographic exposure within portfolio construction. This reality made jurisdiction diversification increasingly relevant for wealthy individuals.

This briefing examines how asset allocation strategies among HNWIs have evolved and identifies the structural forces driving this transformation. It traces the shift from traditional stock–bond frameworks toward multi-asset portfolios incorporating private markets and alternative investments, while also examining the demographic and behavioral dynamics shaping investor preferences. Crucially, it argues that contemporary wealth architecture now operates across two interconnected layers: financial diversification across asset classes and jurisdictional diversification across sovereign frameworks.

Within this context, investment migration emerges as a strategic mechanism through which HNWIs can mitigate sovereign risk while preserving global mobility, market access, and long-term capital resilience.

The global wealth management landscape is undergoing a number of alterations. Drawing on insights from thousands of HNWI-s worldwide, a report by Capgemini states that traditional investment approaches are increasingly “no longer sufficient” to address the evolving priorities, risk perceptions, and behavioral patterns of HNWIs. It emphasizes the need for new strategies, greater personalization, and more dynamic capital deployment frameworks (CapGemini, 2025).

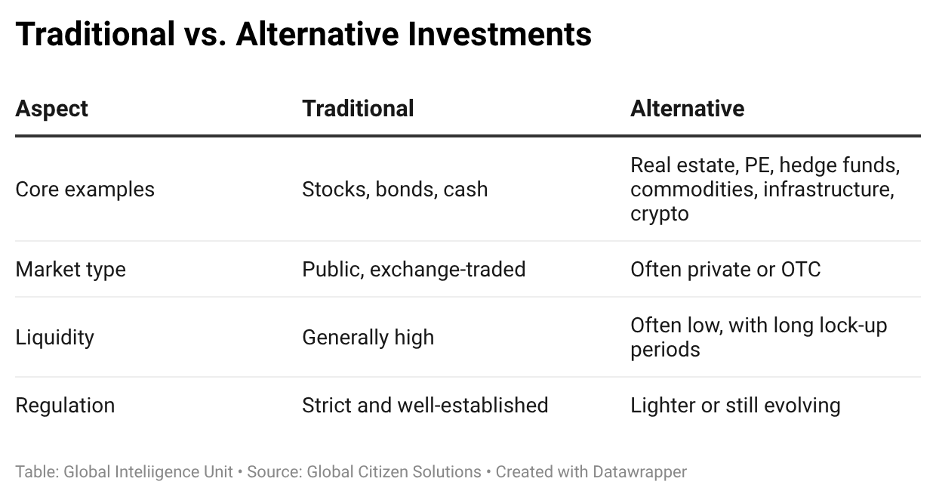

Therefore, the distinction between traditional and alternative assets matters less as a technical classification than a strategic one.

- Traditional assets, primarily public equities, fixed income, and cash equivalents, remain the core liquid building blocks of most portfolios. Their advantages lie in transparency, liquidity, regulatory oversight, and ease of valuation. Yet in a market environment shaped by inflation shocks, compressed bond returns, and elevated public-market correlations, these instruments no longer provide the same diversification and income characteristics they once did. These instruments are highly regulated, relatively liquid, and traded on organized public markets, with transparent pricing and extensive historical data (Doshi, 2023).

- Alternative assets are most simply defined by exclusion: any investment that differs from a traditional stock, bond, or cash deposit. This spans a wide range – real estate, private equity, hedge funds, commodities, infrastructure, managed futures, and structured products, as well as newer categories like cryptocurrencies, NFTs, fine art, wine, and collectibles, which tend to have low correlation with conventional financial markets (Fraser-Sampson, 2012).

The vulnerabilities that affect traditional assets portfolios explain the growing strategic role of alternative assets. Rather than serving as peripheral holdings, alternatives are increasingly used to access sources of return and resilience that are less available in public markets. Private equity offers exposure to growth before public listing and the possibility of capturing illiquidity premia. Real assets such as infrastructure, commodities, and real estate can strengthen inflation hedging and diversify return drivers. Private credit has gained relevance as investors seek enhanced yield and stronger covenant structures in a higher-rate environment. Hedge funds and other non-traditional strategies may also help reduce dependence on broad market direction by introducing differentiated sources of risk and return. Alternative portfolios respond better to structural weaknesses of mainstream investment options.

Table 1. This chart shows a summary of Traditional vs. Alternative investment options and its main characteristics.

The key difference is that alternative investments offer higher potential returns but carry greater risk and lower liquidity, while traditional investments tend to be safer with more predictable, if modest, returns.

In this context, risk primarily reflects liquidity constraints, valuation uncertainty, and lower levels of transparency. Unlike publicly traded equities and bonds, many alternative assets are privately negotiated and traded in less regulated markets, making it more difficult to price and exit. Consequently, investors require a higher expected return as compensation for bearing these additional risks.

The interplay between risk and return has fundamentally shaped the evolution of portfolio theory and the strategic allocation of capital among asset classes. To examine this evolution more systematically, it can be divided into the following phases:

1. Modern Portfolio Theory (50s-2000s): Modern Portfolio Theory, introduced by Harry Markowitz in 1952, formalized the idea that investors can reduce risk and improve returns by diversifying across public equities and bonds, laying the foundation for the classic 60/40 stock-bond allocation widely used through the late 20th century.

2. Institutionalization and Alternatives Expansion (2000–2020): From the 2000s into the 2010s, institutional investors progressively increased their allocations beyond traditional public markets into private equity, private credit, hedge funds and real assets, as product innovation expanded access to alternative asset classes and research highlighted their potential for enhanced diversification and return characteristics relative to conventional stocks and bonds (Fidelity Institutional, 2025).

3. Sovereign Risk Era (2020s–current): In the 2020s, heightened macro financial uncertainty and persistent geopolitical risks have emerged as key concerns for global financial stability. Major geopolitical events have been shown to place downward pressure on asset prices and increase sovereign risk premiums, prompting investors and policymakers to reassess market vulnerabilities and the resilience of exposure management strategies. (International Monetary Fund, 2025).

Moreover, recent episodes of systemic stress have seen equities and bonds decline concurrently, weakening the negative correlation that historically underpinned the diversification benefits of the 60/40 capital deployment model. Prolonged periods of near-zero interest rates further constrained the return potential and defensive role of fixed income. These developments have led investors to reassess static allocation frameworks and increasingly adopt more dynamic, multi-asset strategies that incorporate alternative assets to enhance distribution and portfolio resilience across market regimes (BlackRock, 2023).

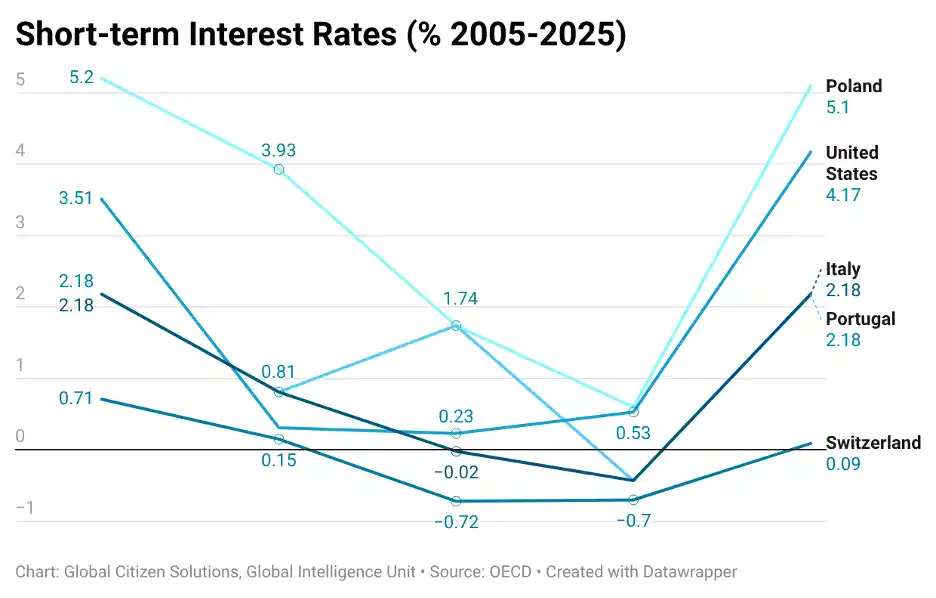

The near-zero interest rate environment in advanced economies is clearly illustrated in the chart below. Following the Global Financial Crisis, short-term interest rates declined sharply across OECD countries and remained close to zero for an extended period. For example, U.S. rates fell from 3.51% in 2005 to 0.31% in 2010 and remained below 1% through 2020, while several European economies experienced negative rates, such as Italy and Switzerland. This prolonged low-rate regime significantly reduced the yield available from traditional fixed-income investments.

Chart 1. Interest Rate Percentages Across Several OECD Economies

One of the major drivers of this shift is geopolitical risk. Caldara and Iacoviello (2022) show that rising geopolitical tension consistently precedes lower investment, greater economic instability, and heightened downside risk. Building on this, Wang, Wu, and Xu (2024) find that when geopolitical risk doubles in intensity, corporate investment falls by 14% the following quarter. The authors measure it by factors such as war threats, political conflict, and international tensions. Historical spikes in geopolitical risk are associated with events such as the Gulf War, the 2003 Iraq invasion, the 2014 Russia-Ukraine crisis, and the aftermath of the September 11 attacks, illustrating how geopolitical tensions can disrupt economic activity and investment decisions.

Other underlying factors include inflationary pressure, technological change, expanding access to private markets and tokenized instruments, the growing influence of values-driven investing, etc.

In an environment marked by inflation shocks, capital controls, sanctions risk, and fiscal tightening, sovereign risk has a direct impact on private balance sheets. Geographic concentration therefore becomes a structural vulnerability.

What are the current patterns of global wealth distribution, and how are high-net-worth individuals responding? Where is wealth concentrated today, and how is it shifting geographically? What generational differences shape investment behavior? Do men and women allocate capital differently, and if so, how?

Understanding these demographic dynamics provides an essential context for explaining how and why investment strategies, including jurisdictional diversification, are evolving.

Table 2. Global Wealth Portrayed in Numbers

Wealth Transfer

An unprecedented intergenerational wealth transfer accelerates structural changes in high-net-worth (HNW) and ultra-high-net-worth (UHNW) investment behavior. Cerulli Associates estimates that approximately $124 trillion will transfer through US households by 2048, with the majority passing to heirs, thereby shifting capital allocation decisions to a younger generation of investors (Cerulli, 2024). This transition is not merely demographic since it also reshapes wealth structuring preferences, risk tolerance, and long-term allocation frameworks.

Where is Wealth Concentrated Today?

Wealth is overwhelmingly concentrated in the US, followed by China and Western Europe, and within those countries, concentrated at the very top of the income/asset distribution.

This pattern is especially pronounced in the United States, where the richest 1 percent owns approximately 35.5 percent of national wealth. By comparison, the share held by the top percentile in many advanced European economies is substantially lower, for example around 27–28 percent in Germany and Sweden, and about 21 percent in the United Kingdom, highlighting the unusually high degree of wealth concentration in the U.S. (World Inequality Database, 2025; Our World in Data).

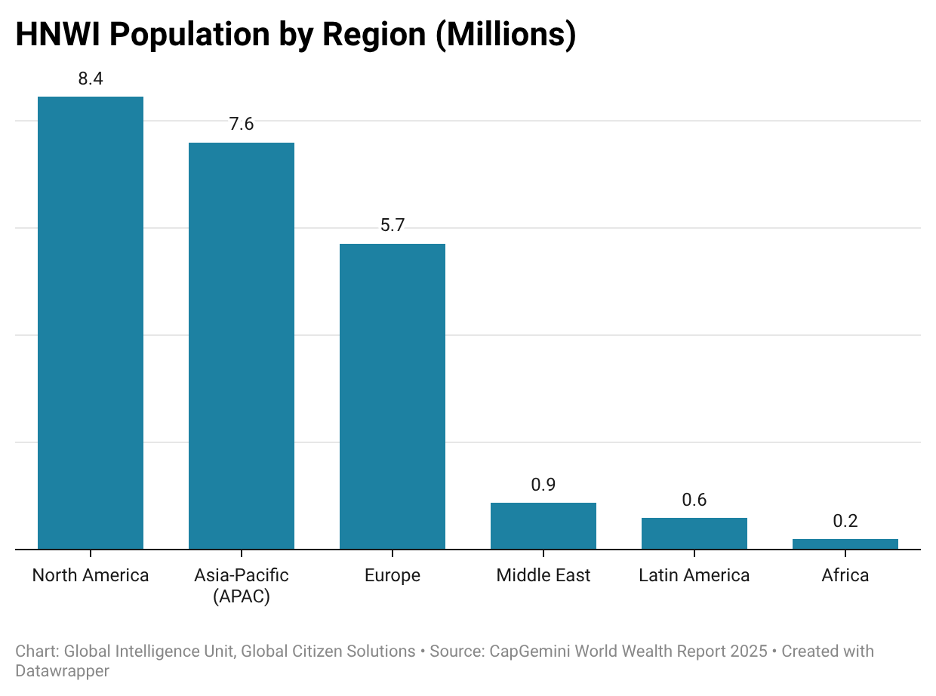

Chart 2. Regional Portrayal of HNWI Population

At the individual market level, Switzerland has its position at the top, followed by the United States, Hong Kong SAR, and Luxembourg. Notable momentum was observed elsewhere, however, as Denmark, South Korea, Sweden, Ireland, Poland, and Croatia all recorded double-digit growth in average wealth when measured in local currencies, suggesting that while concentration remains entrenched at the top, meaningful accumulation is beginning to emerge across a broader set of economies (UBS, 2025).

The Gender Reallocation of Wealth

Alongside these regional and distributional shifts, the demographic composition of wealth ownership is also changing along gender lines. Of the $124 trillion US wealth transfer currently underway, $54 trillion is expected to transfer to surviving spouses, of whom roughly 95% are women, while a further $47 trillion is anticipated to pass to women in younger generations through inheritance. With Baby Boomers currently holding half of all US wealth, this transfer is already in motion. The consequence is that women will soon control a historically unprecedented share of private wealth, a shift widely expected to carry profound implications for how capital is allocated and deployed (Bank of America, 2025).

Research also shows that gender differences influence investment behavior in ways that may affect portfolio outcomes. Women tend to trade less frequently than men, a pattern associated with lower transaction costs and improved long-term performance. They also display lower levels of financial overconfidence and greater awareness of risk, which often results in more diversified and stable portfolios. At the same time, female investors are more likely to incorporate environmental and social considerations into investment decisions and to align financial choices with personal values (Brière, 2025).

Taken together, generational and gender dynamics are reshaping not only who controls global private wealth, but also how it is invested, transferred, and positioned across asset classes and jurisdictions. The demographic transformation of wealth ownership is therefore emerging as a structural driver of evolving allocation strategies.

Generational Risk Preferences and Investment Allocation

Evidence suggests that younger wealthy investors approach capital allocation differently from prior generations. Next-generation HNWIs exhibit stronger preferences for alternative investments, digital engagement, and highly customized strategies (Capgemini, 2025), while UHNW investors more broadly are increasing allocations to private markets and real assets, reflecting a continued shift beyond traditional public securities (Altrata, 2025). Bank of America (2024) reinforces this picture, reporting that younger wealthy individuals are significantly more likely to regard conventional stocks and bonds as insufficient for generating above-average returns.

Older generations, by contrast, remain more anchored to public equities, fixed income, and capital preservation. A divergence that is not merely portfolio-based but philosophical, reflecting fundamentally different relationships with risk, liquidity, and long-term value creation.

The intersection of generational investment preferences and investment migration is increasingly significant. Solimano (2024) observes that younger cohorts – Millennials and Generation Z, demonstrate a marked preference for crypto-currencies and real estate, diverging sharply from the stocks and bonds favored by older generations. Governments are responding to the mobility of the globally wealthy by devising new mechanisms or improving existing ones – digital nomad visas, visas for individuals of independent means, and investment migration programs, to attract investors that can bring fresh capital, know-how, market contacts, and entrepreneurial spirit. As these generational investment patterns become more pronounced, they are poised to reshape both the demand for and the character of investment migration programs worldwide.

Migration data also indicate that geographic mobility is concentrated among younger adults. According to the U.S. Internal Revenue Service’s Statistics of Income migration dataset, approximately 16.3 million individuals changed residence between 2020 and 2021, with those aged 26–34 accounting for the largest share of movers (32.2%). In total, individuals aged 26–44 represented 57.2% of all migrants, highlighting that relocation activity is heavily concentrated among younger working-age populations (IRS, 2023). As younger generations increasingly accumulate wealth and participate in financial markets, this higher mobility may translate into greater openness to international investment opportunities, jurisdictional distribution, and more globally oriented wealth structuring strategies.

As wealth continues to pass between generations, these preferences are not simply being inherited but actively renegotiated, reinforcing a broader structural shift toward alternatives, customization, and more dynamic approaches to portfolio construction.

The investment architecture of high-net-worth individuals (HNWIs) has evolved beyond traditional allocations to publicly traded equities and fixed income instruments. Contemporary capital deployment increasingly incorporates real estate, private equity, venture capital, digital assets, and other alternative investments, reflecting a broader approach to capital deployment across asset classes and jurisdictions. Importantly, geographic risk spreading is not limited to asset location but also relates to exposure across different national risk environments.

Empirical research on international portfolio diversification demonstrates that spreading equity investments across countries can generate measurable risk-reduction benefits, particularly through mitigating market, political, and inflation-related risks over long investment horizons (Attig et al., 2023).

This expanded understanding of diversification provides the foundation for more structurally complex wealth management strategies, including the rise of institutional-style family office platforms, impact investing, etc.

Rise of Sustainable and Impact Investing

Sustainable and impact investing has become an established component of family office portfolio strategy. The UBS Global Family Office Report 2023, based on a survey of 230 single-family offices representing approximately $495.8 billion in wealth, shows that sustainability is increasingly viewed as both a risk and opportunity within investment structuring rather than as a purely ethical or exclusionary approach. The report highlights that family offices are seeking more sophisticated information and advisory support on sustainability issues and increasingly incorporate environmental and social considerations into broader asset allocation frameworks alongside traditional financial objectives (UBS, 2023).

Evolution of Family Office Management

Family offices increasingly operate as comprehensive wealth management structures that extend beyond traditional investment administration. The UBS Global Family Office Report 2023 documents that family offices provide integrated services including investment management, governance structures, estate and succession planning, tax management, and philanthropic activities (UBS, 2023). The report further highlights the growing institutionalization and professionalization of family office operations, including formal governance frameworks and structured risk oversight.

As Part of Investment Framework:

Alternative investments represent a substantial share of sophisticated portfolios. BlackRock’s Global Family Office Survey 2025 reports that alternatives account for approximately 42% of family office portfolios, including private equity, private credit, hedge funds, venture capital, and infrastructure (BlackRock, 2025). Similarly, the UBS Global Family Office Report 2025 documents continued strategic allocations to private equity, private debt, and hedge funds as core long-term holdings (UBS, 2025).

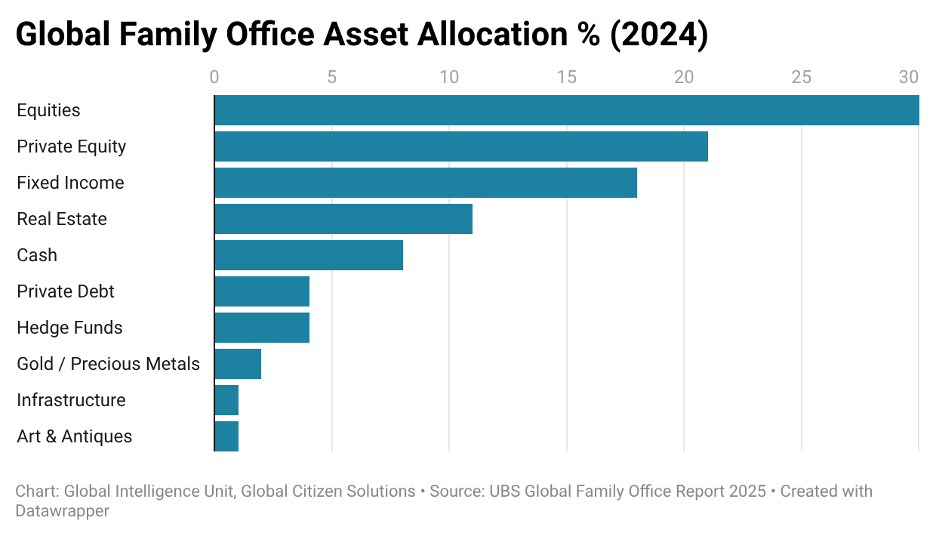

Chart 3. Asset Allocations in Family Offices

Traditional asset classes account for 56% of portfolios, while alternatives represent approximately 44%. This confirms that alternative investments are structural components of family office portfolios rather than marginal allocations.

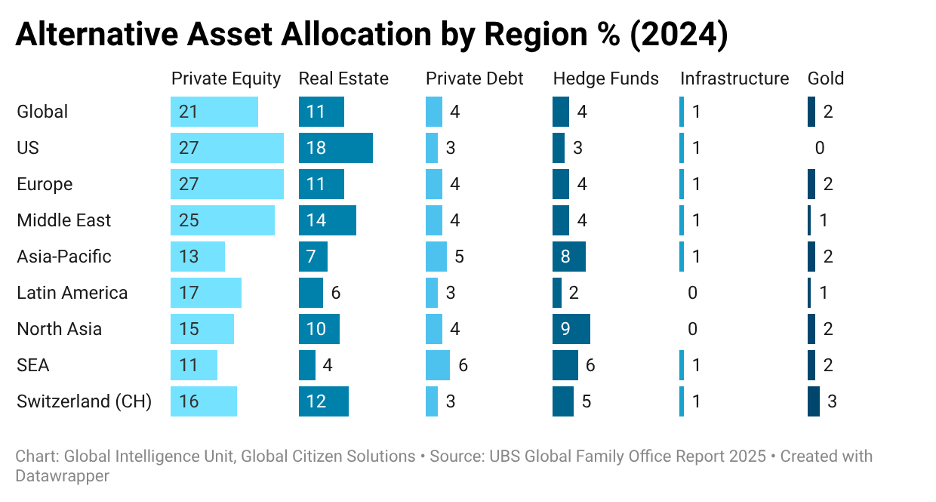

Chart 4. Regional Representation of Alternative Asset Allocation

As shown above, private equity is the largest alternative allocation across nearly all regions. However, the composition of alternatives differs meaningfully, with Asia-Pacific allocating relatively more to hedge funds and private debt compared to the U.S., where real estate and private equity dominate.

Real Estate

Real estate remains a foundational real asset designation within family office portfolios, combining income generation with capital appreciation potential. The UBS Global Family Office Report 2025 documents a consistent average allocation to real estate in 2024, while underscoring that prospects for real estate performance depend importantly on local market conditions (UBS, 2025).

From a capital deployment perspective, real estate provides exposure to multiple return drivers, including rental income, physical asset values, and local economic growth dynamics. Rental income streams may adjust over time, offering some inflation responsiveness, while valuations remain sensitive to interest rates and financing conditions. As a result, performance can diverge across macroeconomic environments. In some emerging markets, higher yield profiles may be attractive, although accompanied by elevated local market risk.

Private Equity and Direct Investments

Private equity continues to represent a substantial alternative allocation for family offices globally. Average private equity exposure stood at approximately 21% in 2024, following a peak of 22% in 2023. The 2024 allocation comprised roughly 11% in direct private equity investments and 10% in funds or funds of funds (UBS, 2025)

The persistence of meaningful private market exposure reflects structural preferences for long-term capital appreciation, access to growth prior to public listings, and the potential to capture illiquidity premia through operational value creation.

Infrastructure

Infrastructure remains a relatively small allocation on average according to UBS (2025), at approximately 1% of family office portfolios. However, broader industry research suggests a rising interest in infrastructure as a strategic asset. A significant share of surveyed family offices view infrastructure positively, and approximately 30% plan to increase infrastructure allocations over 2025–2026. Within alternatives, planned increases in infrastructure allocations are second only to those for private credit. Family offices are leaning toward opportunistic and value-add strategies rather than exclusively core or core-plus approaches. Infrastructure’s linkage to essential services and long-duration cash flows is cited in industry analysis as contributing to its diversifying characteristics (BlackRock, 2025).

Private Credit

Private credit has gained prominence as investors seek yield enhancement amid higher interest-rate environments. More than half of surveyed family offices are bullish on private credit and that approximately 32% of respondents plan to increase allocations to private credit over 2025–2026, the highest planned increase among alternative asset classes in the survey BlackRock, 2025).

Family offices cite private credit’s total return profile, yield characteristics, and senior positioning in capital structures as key attractions. Alternatives more broadly are reported to represent 42% of participating portfolios, underscoring the structural role of private markets in contemporary family office allocations.

Global Diversification and Cross-Border Equity Exposure

International risk distribution remains a structural feature of modern wealth architecture. The International Monetary Fund (IMF) reports that foreign portfolio investment holdings reached USD 71.1 trillion as of June 2024, including USD 40.2 trillion in portfolio equity holdings, both record levels (IMF, 2025). These figures document the sustained scale of cross-border capital allocation and provide a quantitative context for the continued importance of global exposure in investment strategies.

Gold and Safe-Haven Assets

Gold retains a role as a strategic diversifier and risk mitigator. The World Gold Council (2024) emphasizes that gold is a highly liquid asset that is no one’s liability, carries no credit risk, and has a long history of preserving value over time. Consistent with this positioning, UBS (2025) reports that family office allocations to gold and precious metals increased modestly from 1% in 2023 to 2% in 2024.

Digital Assets and Innovation

Digital assets represent a selective but expanding allocation sleeve among institutional and advisory participants. Fidelity reports that 58% of institutional investors surveyed globally hold digital assets or related investments, and 73% of financial advisors surveyed report having an allocation to digital assets (Fidelity, n.d.).

While digital assets exhibit elevated volatility relative to traditional asset classes, their inclusion among institutional and advisory portfolios reflects engagement with technological adoption and financial system innovation themes.

Sustainable and Thematic Investments

Sustainability and thematic investing increasingly form part of strategic portfolio discussions among family offices and high-net-worth investors. A growing share of family offices regard sustainable and impact investing not only as a risk-management consideration but as an investment opportunity. More broadly, sustainability and thematic strategies encompass allocations aligned with environmental transition and governance standards (UBS 2025). These approaches are increasingly integrated across asset classes rather than functioning solely as exclusionary screens.

What do these developments imply?

Contemporary portfolios blend private credit, infrastructure, private equity, gold, and digital assets – a structuring that now extends across liquidity profiles, capital structures, geographies, and thematic exposures rather than asset classes alone.

Yet even this expanded model of risk structuring remains primarily financial in nature. It assumes that risk can be managed through asset allocation within existing legal and sovereign frameworks. Increasingly, however, the stability of those frameworks themselves becomes part of the risk equation, bringing into focus a further dimension of wealth structuring: sovereign risk diversification.

Recent financial history provides multiple examples of how sovereign decisions can directly affect private wealth outcomes. In Cyprus, the 2013 banking crisis resulted in a bail-in that imposed losses on large depositors to recapitalize domestic banks. Argentina has repeatedly introduced capital controls restricting the movement of funds abroad, limiting the ability of investors to transfer capital internationally. Even in advanced economies, policy decisions can alter investment dynamics, as illustrated by the implications of Brexit for cross-border investment flows and property markets in the United Kingdom. These episodes illustrate that sovereign risk is not an abstract concept but a recurring feature of the global financial system, capable of directly influencing portfolio outcomes.

The expansion of alternative investments illustrates how portfolio construction has progressively moved beyond the traditional boundaries of public markets. Yet this evolution also highlights a broader shift in how risk is conceptualized. Investors are no longer diversifying solely across asset classes or liquidity profiles, but increasingly across economic systems, regulatory regimes, and policy environments. Sovereign risk is becoming an increasingly significant factor in the portfolio assessment metrics of wealthy investors.

What exactly are younger generations inheriting? Consider a concrete example: a family holding a substantial concentration of Swiss real estate. On paper, a sound and stable asset. Yet looking toward 2050, when Switzerland’s climate neutrality mandates come into full effect, that same portfolio faces mounting retrofitting costs, potential devaluation of non-compliant properties, and growing regulatory uncertainty (UBS, 2025).

The question for the next generation is therefore not simply what they are inheriting, but whether the jurisdictions anchoring that wealth still make sense.

This is where geographic distribution evolves from a purely financial strategy into a legal and regulatory one. Allocating assets across multiple jurisdictions may reduce exposure to any single country’s policy trajectory – whether related to climate regulation, taxation, capital controls, or political instability. The choice of destination becomes as consequential as the act of risk distribution itself: some investors may seek jurisdictions with less aggressive decarbonization mandates, while others prefer markets where sustainability standards are already embedded in asset pricing, thereby reducing future regulatory uncertainty.

More broadly, a defining feature of contemporary portfolio strategy is the intentional structuring of capital across jurisdictions rather than across markets alone. Digital assets may be held where regulatory treatment is clear and predictable ; real estate acquired where ownership provides both yield and optionality; liquidity diversified across currencies; and operating entities incorporated in stable financial centers. The analytical lens shifts accordingly: the question is no longer only what is owned, but under which legal and regulatory system it operates. In this sense, wealth is no longer anchored within a single framework, instead it is distributed across several.

Overlooking Concentration Risk

Even when capital is diversified across jurisdictions, a deeper concentration risk often persists: sovereign dependence embedded in citizenship and residency. Financial assets may be globally allocated, yet taxation, capital mobility, property rights, and legal protection typically remain anchored to a single state. This structural exposure cannot be mitigated through asset structuring alone.

In this context, investment migration functions as a formal mechanism of jurisdictional risk management. With the global market estimated at $20–30 billion annually (IMI Daily 2019, TTT, 2025), alternative citizenships and residencies increasingly serve as tools for accessing different legal and regulatory systems, reducing exclusive reliance on a single sovereign framework. Unlike traditional wealth allocation, jurisdictional hedging spreads risk across different legal, tax, regulatory, and political systems.

The relevance of investment migration also lies in the concrete advantages it introduces at the intersection of legal status, regulatory exposure, and capital allocation. These benefits can be grouped into four interrelated dimensions:

- Regulatory Arbitrage and Sovereign Risk Hedging

Alternative citizenships and residencies reduce exposure to single-country political, regulatory, or macroeconomic shocks. Jurisdictional diversification embeds structural optionality into the broader wealth framework, while also preserving the ability to relocate capital, operations, or family should legal or policy conditions materially deteriorate.

- Tax Structuring and Legal Optimization

Strategic residency placement enables lawful tax efficiency and access to differentiated fiscal regimes that are unavailable within a single-jurisdiction framework. When properly structured, cross-border residency can materially affect after-tax returns and long-term wealth preservation.

- Market Access and Strategic Expansion

Residency and citizenship programs, including EU residence pathways, the U.S. EB-5 program, and Caribbean citizenship programs enhance mobility and facilitate market entry. For entrepreneurs and investors, jurisdictional positioning can directly influence cross-border transactions, M&A strategy, capital raising, and operational scalability.

- Asset Protection and Crisis Optionality

Concentration in a single sovereign framework creates asymmetric downside exposure. Alternative residencies introduce legal and geographic optionality, limiting vulnerability to adverse policy shifts while preserving strategic flexibility under uncertainty.

Accordingly, the contemporary HNWI portfolio extends beyond traditional capital allocation to incorporate legal and sovereign structuring. Jurisdictional flexibility is becoming a structural component of the capital preservation strategy. Investment migration institutionalizes that flexibility, embedding optionality at the sovereign level and aligning personal legal architecture with financial strategy.

Under this paradigm, wealth management is no longer confined to asset selection within a jurisdiction. It increasingly becomes the deliberate positioning of capital across jurisdictions.

This briefing has traced the structural evolution of high-net-worth investment portfolios, from the traditional stock–bond framework toward more complex, multi-asset architectures incorporating private equity, private credit, infrastructure, and real assets. Prolonged low interest rate environments, shifting correlations between asset classes, and the broader limitations of public markets have collectively prompted a reallocation toward alternative investments – instruments that now constitute nearly half of family office portfolios globally.

Alongside this financial evolution, demographic dynamics are reshaping the composition and behavior of wealth holders. The ongoing intergenerational transfer of capital, combined with documented differences in investment behavior across age and gender, is producing a shift in preferences toward greater diversification, geographic mobility, and values-aligned allocation strategies.

The briefing then examined what has emerged as a central variable for contemporary wealth management: sovereign risk. Geopolitical fragmentation, fiscal tightening, capital controls, and regulatory divergence have established that the legal and political environment governing private wealth is itself a source of material risk – one that asset class diversification alone cannot address. This recognition extends the logic of diversification beyond the financial dimension into the jurisdictional one.

Investment migration represents one of key formal mechanisms through which this jurisdictional diversification is institutionalized, offering sovereign risk hedging, legal optimization, market access, and structural optionality under conditions of uncertainty. These developments collectively point toward an emerging paradigm in wealth architecture – the borderless portfolio, in which capital is not merely allocated across asset classes, but deliberately positioned across sovereign frameworks. Under this model, personal legal status becomes a structural component of long-term wealth strategy, and the central analytical question shifts: not only what is owned, but under which legal system it operates.

- Capgemini Research Institute. (2025). World Wealth Report 2025: Sail the great wealth transfer (29th ed.). Capgemini. https://www.capgemini.com/insights/research-library/world-wealth-report/

- Doshi, T. (2023). A comparative analysis of traditional and alternative asset classes. International Journal of Social Science and Economic Research, 8(7), 1707–1729. https://ijsser.org/2023files/ijsser_08__128.pdf

- Fraser-Sampson, G. (2012). What are alternative assets? In G. Fraser-Sampson (Ed.), Alternative assets: Investments for a post-crisis world (ch. 1). John Wiley & Sons. https://doi.org/10.1002/9781119205821.ch1

- Fidelity Institutional. (2025). A study of allocations to alternative investments by institutions and financial advisors. https://institutional.fidelity.com/app/proxy/content?literatureURL=%2F9909709.PDF

- International Monetary Fund. (2025). Chapter 2: Geopolitical risks: Implications for asset prices and financial stability (Global Financial Stability Report, April 2025). https://www.imf.org/-/media/files/publications/gfsr/2025/april/english/ch2.pdf

- BlackRock. (2023). 60/40 portfolios and alternatives. https://www.blackrock.com/us/individual/insights/60-40-portfolios-and-alternatives

- Cerulli. (2024). U.S. High-Net-Worth and Ultra-High-Net-Worth Markets. https://www.cerulli.com/reports/us-high-net-worth-and-ultra-high-net-worth-markets-2024

- World Inequality Database. (2025). Wealth share of the richest 1% [Dataset]. Our World in Data. https://ourworldindata.org/grapher/wealth-share-richest-1-percent

- UBS Group AG. (2025, June 18). Global wealth report 2025: Wealth growth accelerated in 2024. UBS. https://www.ubs.com/global/en/media/display-page-ndp/en-20250618-gwr-2025.html

- Bank of America Institute. (2025). Women and wealth: Growing the pie, creating opportunities. https://institute.bankofamerica.com/content/dam/economic-insights/women-and-wealth-creating-opportunities.pdf

- Brière, M. (2025). Women and investment. Amundi Investment Institute. https://research-center.amundi.com/files/nuxeo/dl/22f96a00-ba27-43b1-aa18-24a8a4b9d5b0

- Capgemini Research Institute. (2025). World wealth report 2025. https://www.capgemini.com/insights/research-library/world-wealth-report/

- Altrata. (2025). UHNW asset allocation. https://altrata.com/articles/uhnw-asset-allocation

- Solimano, A. (2024). Anatomy of the global wealthy: Millennials, investment patterns, and the international mobility of high-net-worth individuals (IMC-RP 2024/1). Investment Migration Council. https://investmentmigration.org/wp-content/uploads/2024/11/Anatomy-of-the-Global-Wealthy-2.pdf

- Internal Revenue Service. (2023). SOI tax stats – Migration data: U.S. population migration by age based on individual income tax returns, 2020–2021. U.S. Department of the Treasury. https://www.irs.gov/pub/irs-pdf/p5508.pdf

- Bank of America Private Bank. (2024). Study of wealthy Americans. https://mlaem.fs.ml.com/content/dam/ML/Articles/pdf/Study_of_Wealthy_Americans_WhitePaper.pdf

- Caldara, D., & Iacoviello, M. (2022). Measuring geopolitical risk. American Economic Review, 112(4), 1194–1225. https://www.aeaweb.org/articles?id=10.1257/aer.20191823

- Wang, X., Wu, Y., & Xu, W. (2024). Geopolitical risk and investment. Journal of Money, Credit and Banking, 56(8), 2023–2059. https://onlinelibrary.wiley.com/doi/abs/10.1111/jmcb.13110

- Attig, N., El Ghoul, S., Guedhami, O., & Rizeanu, S. (2023). International diversification benefits and country-level risk. Journal of International Financial Markets, Institutions & Money. https://www.sciencedirect.com/science/article/abs/pii/S1042443122002013

- UBS. (2023). Global family office report 2023. UBS.

https://www.ubs.com/content/dam/assets/wm/static/noindex/gfo/docs/ubs-gfo-report-2023.pdf

- BlackRock. (2025). Global Family Office Report 2025 (Family Office Survey).

https://www.blackrock.com/gls-download/literature/whitepaper/global-family-office-report.pdf

- Fidelity. (n.d.). Digital assets insights.

https://clearingcustody.fidelity.com/app/item/RD_9902266/digital-assets.html

- International Monetary Fund (IMF). (2025). Foreign portfolio investment equity holdings hit record high in June 2024. https://data.imf.org/en/news/31925foreign%20portfolio%20investment%20equity%20holdings%20hit%20record%20high%20in%20june%202024

- UBS. (2025). Global Family Office Report 2025.

https://www.ubs.com/content/dam/assets/wma/static/documents/ubs-gfo-report.pdf?utm_source=chatgpt.com

- World Gold Council. (2024). The relevance of gold as a strategic asset.

https://www.gold.org/goldhub/research/relevance-of-gold-as-a-strategic-asset

- Travel Trade Today. (2025). Investment migration trends 2025: High-net-worth insights. https://traveltrade.today/travel-insights/investment-migration-trends-2025-high-net-worth-insights/

- Nesheim, C. H. (2019). Investment migration market would reach US$100bn in revenue by 2025 if 23% CAGR trend persists. IMI Daily. https://www.imidaily.com/editors-picks/investment-migration-market-would-reach-us100bn-in-revenue-by-2025-if-23-cagr-trend-persists/