When we launched the Global Passport Index in 2021, our ambition was to redefine what “passport power” truly means in an era of unprecedented mobility, and mounting uncertainty. Four years later, the Global Passport Index 2025 captures a world transformed: one where the ability to move freely, invest wisely, and live securely has never been more valuable.

In today’s unstable global landscape, marked by geopolitical tensions, climate challenges, and shifting economic tides, passport strength is not only about visa-free travel. It has become a vital instrument of resilience. For many, a powerful passport is a Plan B: a pathway to safety, a tool for relocation, and a means of diversifying investment and opportunity across borders.

The 2025 results reveal a world of contrasts and convergence. Europe remains dominant, propelled by governance quality and institutional trust; the Nordic countries exemplify how social cohesion and innovation reinforce long-term strength. Singapore continues to lead in Asia as a model of foresight and stability, while smaller states (from the Baltics to the Caribbean) demonstrate that strategic openness and sound governance can turn size into advantage. On the other hand, one of the most striking findings this year is the United States’ 13-place decline since 2021, a reminder that even the world’s largest economies are not immune to structural slowdown and governance challenges

At Global Citizen Solutions, we believe that citizenship is more than a legal status, it is a bridge to opportunity, belonging, and resilience. The Global Passport Index 2025 embodies that vision: a data-driven tool to understand not only where opportunities lie, but how nations enable individuals to thrive amid uncertainty.

As the world becomes more complex, the value of a passport extends far beyond mobility, it becomes a form of freedom insurance. The countries that will lead in this new era are those that pair openness with stability, opportunity with responsibility, and prosperity with purpose.

I invite you to explore this edition not just as a ranking, but as a reflection of how nations empower people to move, invest, and live freely, in a world where adaptability and foresight have become the ultimate measures of strength.

By Patricia Casaburi, CEO, Global Citizen Solutions

Since 2021, Global Citizen Solutions has published the Global Passport Index (GPI), an index designed to move beyond conventional assessments of travel freedom and capture the wider dimensions of global mobility. In response to the growing complexity and interdependence of international relations, the GPI has progressively evolved into a comprehensive measure of passport strength.

Unlike other indexes that focus narrowly on visa-free access, the GPI incorporates broader indicators (including quality of life, innovation and investment potential, and the strategic advantages conferred by citizenship) providing a more holistic framework for evaluating a country’s global standing.

The GPI is built on a multi-dimensional framework that integrates hard data and qualitative indicators. It draws on international sources such as the World Bank, World Economic Forum, UNDP, and government statistics, ensuring comparability and consistency across countries.

The index is structured around three core dimensions:

- Enhanced Mobility (Passport Strenght)

- Evaluates the number of visa-free or visa-on-arrival destinations, but also the desirability of those destinations.

- Goes beyond quantity by considering the strategic importance of mobility options.

- Investment & Innovation

- Measures economic competitiveness, infrastructure quality, innovation capacity, taxation systems, and ease of doing business.

- Highlights countries that offer strong prospects for investors, entrepreneurs, and skilled workers.

- Quality of Living

- Covers safety, environmental performance, political stability, freedom, health care, education, and overall well-being.

- Captures how attractive a country is as a place to live, not just to visit

Purpose and Evolution

In 2025, the GPI offers not just a snapshot of rankings, but a deeper analysis of how countries perform over time, helping investors, policymakers, and globally minded individuals understand where opportunities and advantages are emerging. With four years of data now available, the GPI enables year-on-year comparisons, revealing how countries rise, stabilize, or decline across different dimensions.

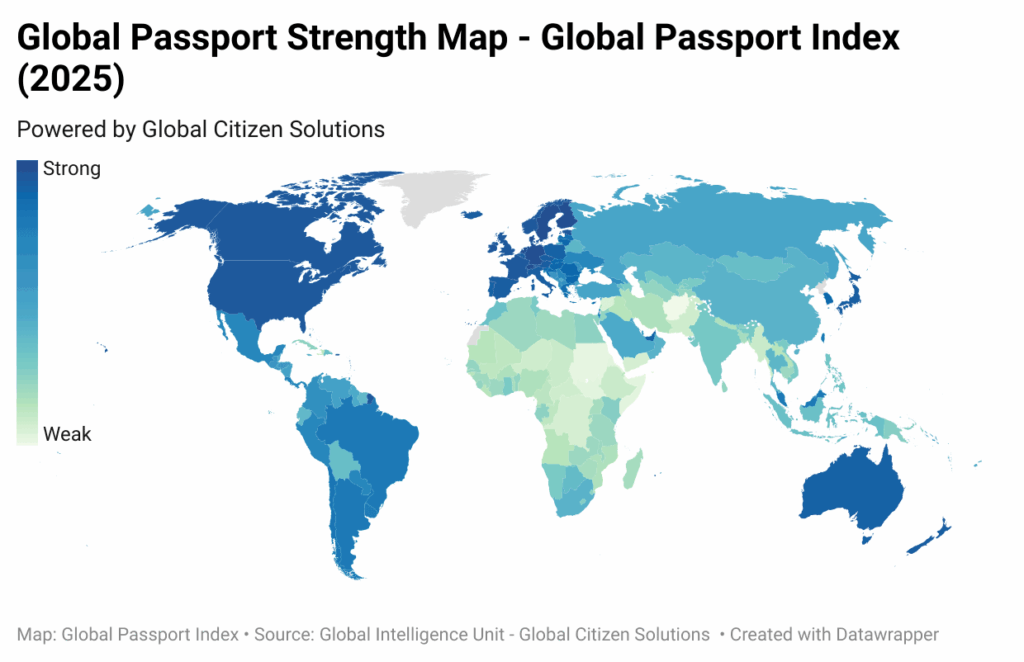

The Passport Strength Map 2025 (below) vividly illustrates the widening global divide in mobility and citizenship advantages. The darkest shades of blue (concentrated across Northern and Western Europe) signal the world’s strongest passports, anchored by countries like Sweden, Switzerland, Finland, and Germany. These nations combine high levels of institutional trust, innovation capacity, and diplomatic reach, granting their citizens access to an unparalleled range of destinations. Europe’s dominance extends beyond travel freedom: it reflects deep integration through the European Union and Schengen Area, where shared governance standards, cross-border labor mobility, and harmonized regulations reinforce both economic competitiveness and quality of life. This structural interconnectedness translates directly into high GPI scores, as European passports provide not just travel access, but also predictable environments for living, investing, and working abroad.

Beyond Europe, strong performers appear in North America and Oceania, with the United States, Canada, Australia, and New Zealand maintaining dark blue tones but no longer leading globally. Their relative lightening compared to previous years highlights a subtle but persistent erosion in competitiveness and quality-of-life dimensions. Factors such as housing bottlenecks, political polarization, and productivity slowdowns have weakened their positions. The Anglosphere’s gradual decline on the map contrasts sharply with the stability of the Nordics and Central Europe, where long-term policy coherence continues to compound advantages.

Singapore emerges as a bright beacon in Asia, maintaining a strong hue that reflects its exceptional balance of mobility access, regulatory predictability, and innovation leadership, making it the only non-European country to reach the global top ten. In contrast, most of Asia displays lighter tones, particularly in South and Central Asia, where institutional weaknesses, demographic pressures, and limited diplomatic networks constrain mobility strength.

Latin America presents a more varied picture, with mid-blue shades concentrated in Chile, Uruguay, and Costa Rica, where governance quality and education investments have lifted overall standing. Yet the region’s larger economies (Brazil, Mexico, and Argentina) remain lighter, reflecting stagnation in institutional reforms and limited diversification of global ties. The Caribbean, while geographically small, appears as pockets of moderate blue, representing nations that have leveraged citizenship-by-investment programs to improve fiscal resilience and expand diplomatic access. However, these gains remain volatile, dependent on global regulatory acceptance and external demand for CBI schemes.

Africa and parts of the Middle East remain the lightest areas on the map, underscoring enduring challenges in governance, infrastructure, and economic diversification. Although a few outliers such as Mauritius, Seychelles, and Rwanda show progress, most of the continent continues to face barriers to international integration and regional mobility. High levels of informality, security concerns, and limited bilateral visa agreements keep much of Africa in the lower tiers of the GPI.

Ultimately, the map encapsulates a world divided not only by borders but by the capacity of nations to generate and sustain trust, opportunity, and mobility. It shows that passport power is no longer a static privilege, it is the cumulative outcome of decades of governance quality, social investment, and strategic openness.

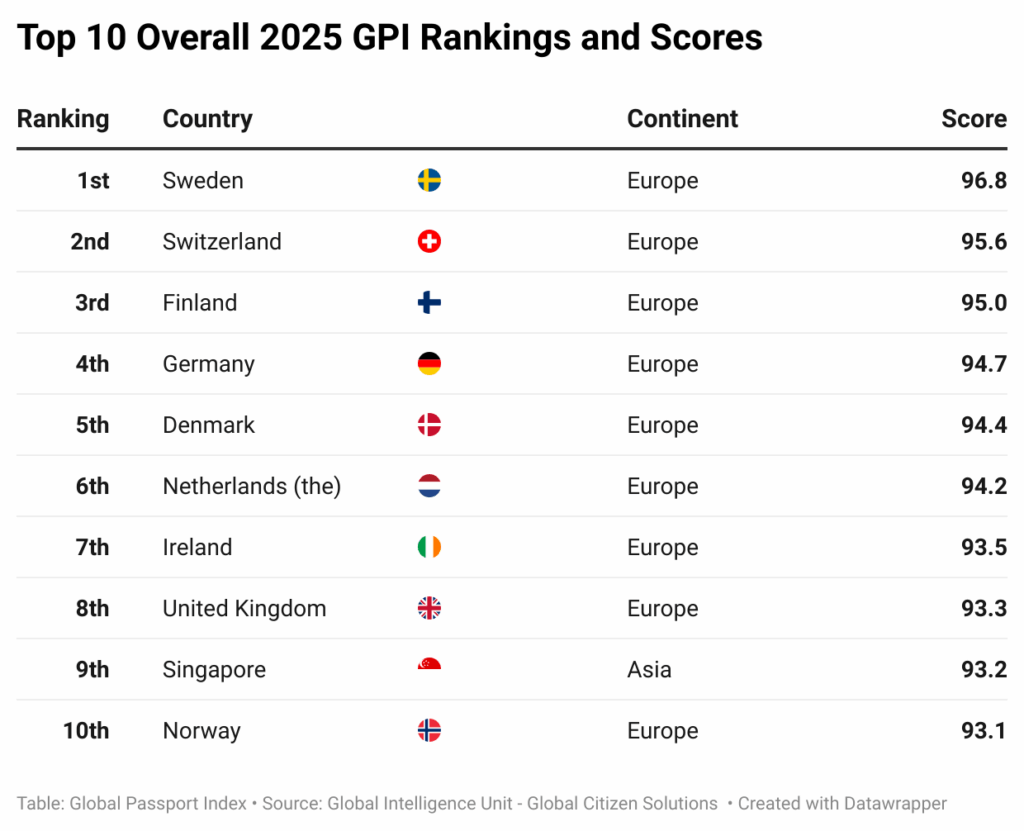

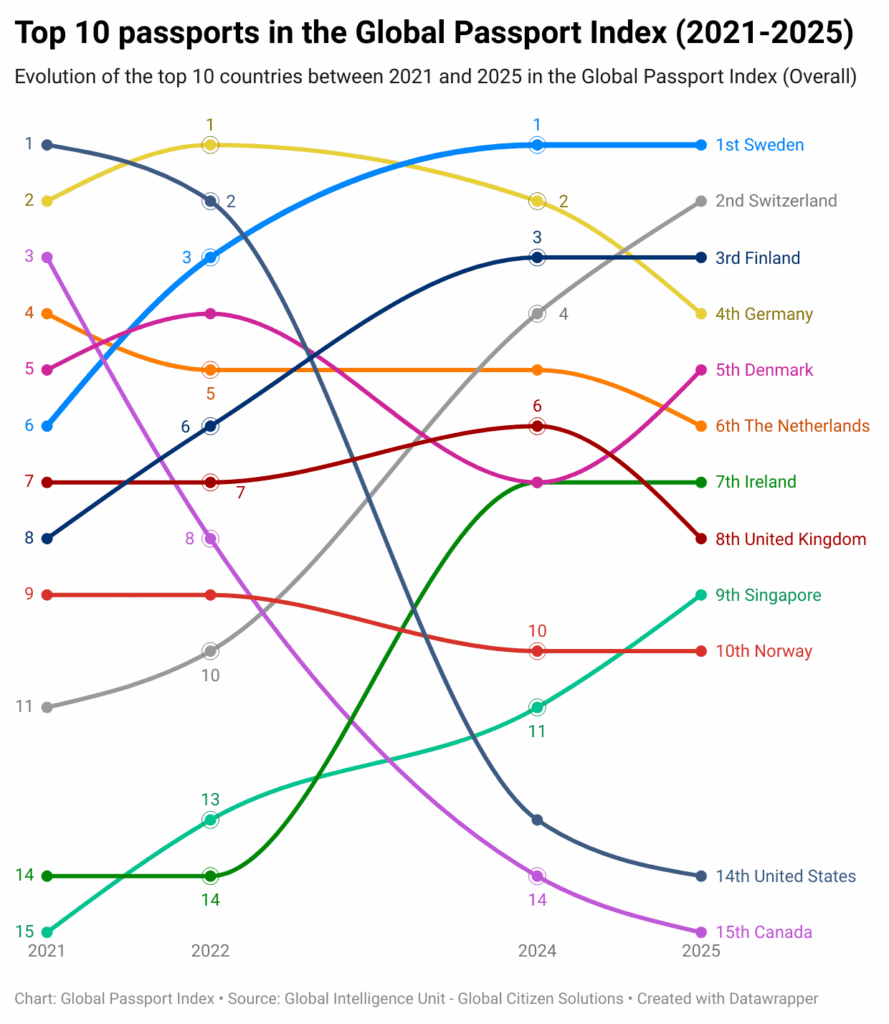

Between 2021 and 2025, the Global Passport Index shows a dynamic reshuffling among the world’s strongest passports, with Sweden emerging as the consistent leader, with Finland (3rd) and Denmark (5th) in the top 5, solidifying the Nordic region’s dominance. These countries have steadily climbed or maintained top positions thanks to their exceptional mobility access, high quality of life, and strong investment environments. Switzerland (2nd) and Germany (4th) remain stable within the top five, while the Netherlands (6th) and Ireland (7th) have gained ground, reflecting robust economic and social frameworks.

Singapore (9th) continues to represent Asia as the only non-European country in the top ten, underlining its global connectivity and business competitiveness. In contrast, the United States (14th) and Canada (15th) have gradually declined in ranking, signalling stagnation in mobility and quality-of-life indicators. Continent-wise, Europe overwhelmingly leads with nine of the top ten passports, reaffirming its global edge in freedom of movement, stability, and overall citizen welfare

The GPI 2025 highlights how global performance is far from evenly distributed, with Europe holding nine of the top ten positions, a clear sign of the continent’s entrenched advantages in governance, human capital, and innovation ecosystems.

Despite the rise of other regions as new geopolitical and economic powerhouses, what the index captures is Europe’s durable infrastructure of trust: predictable rule of law and contract enforcement; high institutional quality across courts, regulators, and central banks; dense human-capital pipelines fed by universities and intra-EU mobility, with research systems that translate public science into private innovation via clusters in life sciences, green tech, advanced manufacturing, and software. Layered on top is a powerful set of network effects that reinforce Europe’s lead: Schengen-wide travel freedom, integrated capital markets and payment rails, interoperable standards, and social safety nets that reduce entrepreneurial risk while bolstering household resilience.

Even where growth is slower and defense or energy dependencies are debated, the continent’s combination of governance quality, mobility, education, health, and environmental performance continues to produce superior overall outcomes: safer cities, cleaner environments, higher life expectancy, and passports that unlock both movement and market access.

The only non-European country to break into the top tier is Singapore, reflecting Asia’s capacity to produce exceptional performers under the right conditions. Meanwhile, the Anglosphere (U.S. and Canada) has suffered significant declines, suggesting that structural bottlenecks are outweighing traditional strengths. Latin America and Africa remain somehow stagnant, with some success stories, while the Caribbean and smaller states show selective gains often tied to tourism or niche investment programs. A closer analisys of regional patterns shows that integration, reform, and governance quality explain much of the divergence in trajectories between 2021 and 2025.

Europe

Europe’s overwhelming presence in the global top ten is anchored by Sweden, Switzerland, Finland, Germany, Denmark, the Netherlands, Ireland, the United Kingdom, and Norway. These countries continue to deliver high levels of prosperity and mobility opportunities thanks to stable institutions, welfare-state resilience, and a strong innovation base.

The European Union plays a central role in sustaining this dominance by providing a framework for integration, cross-border collaboration, and regulatory predictability. Yet the picture is more nuanced when looking eastward. Estonia has been the standout performer, climbing sixteen places since 2021, driven by its pioneering digital governance model. Croatia’s entry into the euro area and Schengen in 2023 translated into a seven-place jump, proving how integration milestones can rapidly improve global standing. However, Romania and Slovakia declined modestly, while Latvia and Lithuania stagnated, highlighting some governance gaps and uneven productivity diffusion.

Nordic Exceptionalism in the GPI 2025

Global Citizen Solutions has tracked mobility and state capacity through a methodology that has matured into today’s GPI: a composite score that blends three dimensions: Enhanced Mobility, Investment & Innovation, and Quality of Living into a single comparative lens.

In the 2025, Nordic countries account for four out of the ten leading global rankings. Sweden leads the world with an overall score of 96.8, followed by Switzerland (95.6) and Finland (95.0), with Germany (94.7) and Denmark (94.4) rounding out the top five. Norway sits at #10 (93.1). These are not one-off outliers: Sweden aitis again in the pole position after several years in the top tier (6th in 2021 and 3rd in 2022, 1st in 2023 and 2024); Finland climbs steadily into the top three; Denmark and Norway remain durably inside the top ten. In other words, the Nordic result in GPI 2025 is the latest chapter in a long story of institutional strength converted into global advantage.

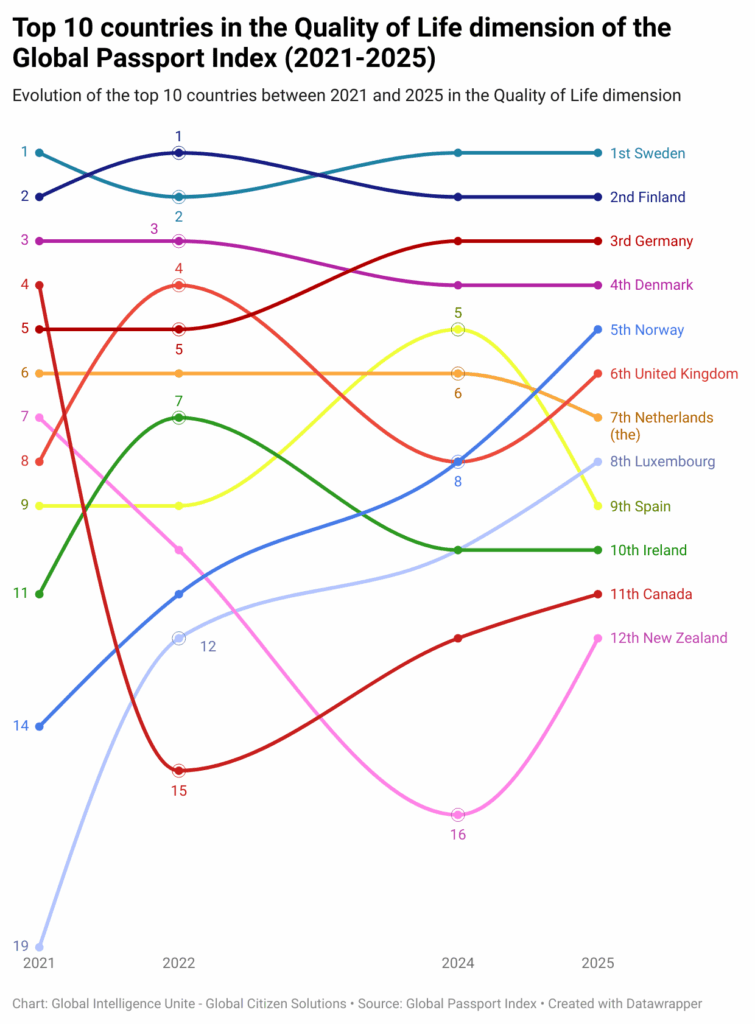

A central reason the Nordics dominate the GPI’s Quality of Living dimension is that they consistently top independent, longitudinal measures of well-being and social stability (see chart below). Their success underscores that true national strength extends beyond economic output, it lies in social trust, inclusivity, and well-being. These countries demonstrate how sustained investment in public services and social infrastructure translates into both higher life satisfaction and stronger global standing((Global Citizen Solutions. (2024). Beyond borders: How quality of life indicators shape the best places to live — 2024 global passport index. https://www.globalcitizensolutions.com/briefing/beyond-borders-how-quality-of-life-indicators-shape-the-best-places-to-live-2024-global-passport-index/)).

The World Happiness Report’s again places all five Nordic countries in the global top ten, with Finland still first and Denmark “very close,” a persistence that is unusual in cross-country indicators and points to deep institutional roots rather than cyclical luck((Helliwell, J., Layard, R., & Sachs, J. (Eds.). (2024). World Happiness Report 2024. Sustainable Development Solutions Network. https://files.worldhappiness.report/WHR24.pdf)). Those outcomes correlate with high scores on governance metrics: the World Bank’s Worldwide Governance Indicators show the Nordics clustered at the top of global distributions for rule of law, government effectiveness, and regulatory quality, precisely the institutional features that translate into predictable public services and social trust((World Bank. (2024). Worldwide Governance Indicators: 2024 update [Data set]. World Bank Group. https://data.worldbank.org/indicator/GE.EST)).

The Quality of Living data move in the same direction across 2021–2025: Sweden climbs from 87.2 to 91.5; Finland from 85.9 to 90.9; Denmark from 84.2 to 87.4; and Norway from 79.4 to 86.5. That uplift aligns with the external evidence: when rule-of-law states deliver security, health, education and environmental performance consistently, quality-of-life scores rise and stay high.

On Innovation & Investment, the Nordics are not just steady, they are structurally advantaged. In the European Commission’s European Innovation Scoreboard 2024, Sweden is profiled as an “Innovation Leader,”((European Commission, Directorate-General for Research & Innovation. (2024, July 8). European Innovation Scoreboard 2024: Main report. Publications Office of the European Union. https://research-and-innovation.ec.europa.eu/knowledge-publications-tools-and-data/publications/all-publications/european-innovation-scoreboard-2024_en)) with Denmark and Finland also in the top innovation group relative to the EU average; the scoreboard’s country profiles attribute this to science–industry linkages, digital readiness, and sustained R&D intensity. The R&D numbers themselves are telling. According to World Bank series (via World Bank–sourced dashboards), Sweden’s R&D spending stands around 3.41% of GDP (2024), Finland’s at about 2.96%, and Denmark’s roughly 2.89%, all comfortably above the OECD average and the level typically associated with frontier innovation ecosystems((International Energy Agency. (2023, December 5). Denmark 2023 – Analysis. IEA. https://www.iea.org/reports/denmark-2023/executive-summary )).

Sectorally, the green-tech lead that shows up in the Investment scores has hard infrastructure behind it: the International Energy Agency reports Denmark is doubling renewable capacity over 2022–2027 on the back of offshore wind build-out((Danish Energy Agency. (n.d.). Vesterhav Nord and Syd offshore wind project (Denmark). Power-Technology. Retrieved [date you accessed], from https://www.power-technology.com/projects/vesterhav-nord-and-syd-offshore-wind-project-north-sea-denmark/)), embedding resilience into energy-intensive industry while de-risking future costs.

In the 2025 GPI, Sweden’s Investment score rises from 63.7 (2021) to 72.9 (2025), with Denmark holding a strong 66.1 in 2025; Finland is steady at 64.6. Those trajectories are exactly what the external indicators would predict for coordinated, R&D-heavy economies that invest in grid-scale renewables, human capital, and digital state capacity.

The Enhanced Mobility dimension (where all four Nordics again post world-class results) matters for more than seamless travel. Global Citizen Solutions weights the quality and desirability of destinations, not only the count. Nordic passports unlock dense networks across the EU/EEA, North America and advanced Asian economies; that network effect is visible in your 2025 scores.

Those figures place the Nordics in the first rank of mobility worldwide, and they square with the broader literature on how small, open economies translate external access into internal prosperity. In political economy terms, this is the model Peter Katzenstein described (small states that leverage openness and corporatist coordination to turn vulnerability into competitive strength)((Katzenstein, P. J. (1985). Small states in world markets: Industrial policy in Europe. Cornell University Press.)) and one that later scholarship on “coordinated market economies” formalized as an institutional equilibrium conducive to high skills, patient capital and incremental innovation((Hall, P. A., & Soskice, D. (2001). Varieties of capitalism: The institutional foundations of comparative advantage. Oxford University Press.)).

The picture that emerges is coherent across sources and across time. Your GPI records the outcomes: Sweden’s overall score reaches 96.8 in 2025, Finland 95.0, Denmark 94.4, and Norway 93.1.

Put simply, the Nordics excel in the GPI because they score highly, year after year, on the inputs that compound: high-trust governance, human-capital formation, innovation finance, and internationally valuable mobility. Those inputs show up as rising Quality of Living, stable or improving Investment scores, and as top-end Enhanced Mobility. They are also the features most resistant to short-term shocks.

That combination (resilient institutions plus outward orientation) is why Sweden finally takes top position in 2025, why Finland keeps climbing, and why Denmark and Norway remain fixtures at the top.

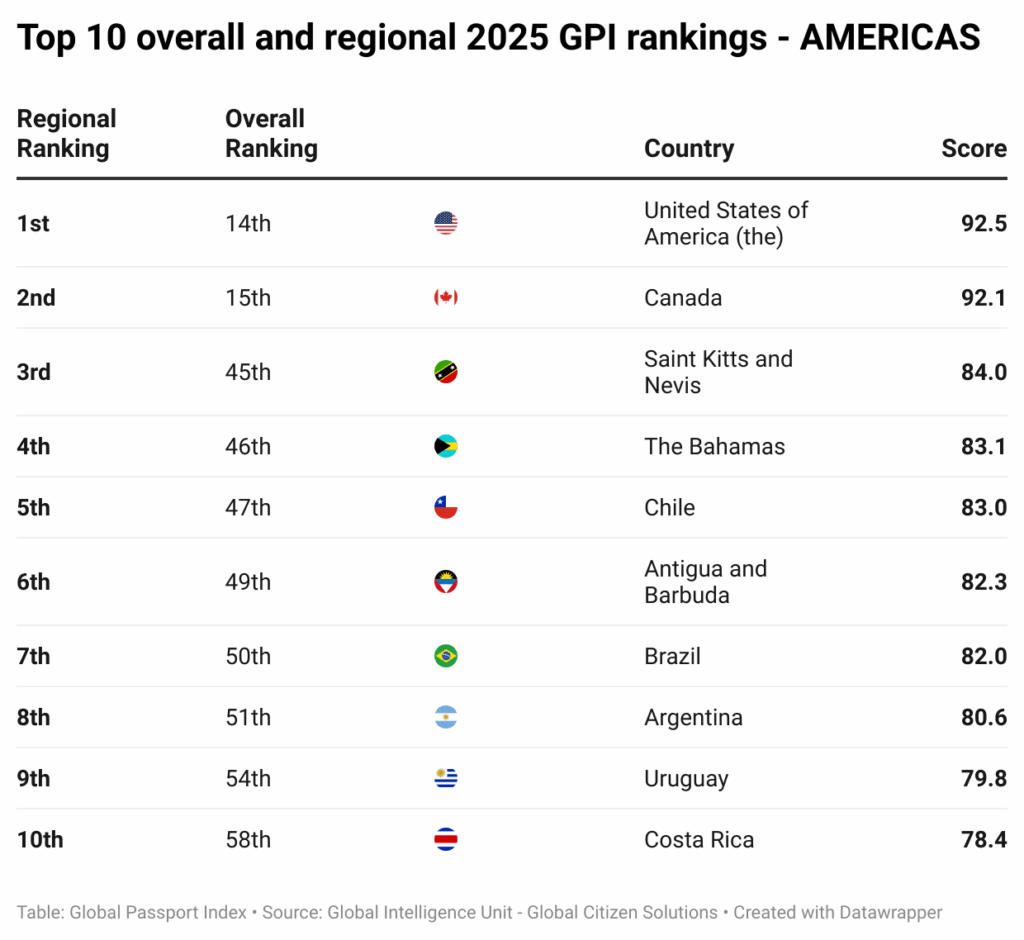

The Americas

Anglo America

The most striking downward movements are concentrated in the Anglosphere, especially the United States and Canada. The U.S., which topped the index in 2021, has dropped to fourteenth by 2025 and Canada has lost ten places. These declines do not imply a collapse in innovation or economic weight but rather the persistence of structural inefficiencies. Productivity growth outside frontier firms has been weak, housing shortages limit labor mobility, and polarized politics have weakened institutional predictability.

The common thread is a persistent productivity drag. Across both economies, the OECD’s most recent productivity compendia show weak or even negative contributions from multifactor productivity (MFP) in 2023, underscoring that the problem is structural rather than cyclical; notably, the OECD lists Canada and the United States among countries where MFP’s contribution to growth was negative, a clear warning sign for medium-term competitiveness. At the same time, the OECD’s 2024/2025 productivity work highlights the widening gap between frontier firms and the rest, evidence that diffusion is faltering, so world-class research and tech hubs aren’t translating into broad-based gains quickly enough to sustain top-tier rankings((Organisation for Economic Co-operation and Development. (2024). OECD Compendium of Productivity Indicators 2024. OECD Publishing. https://doi.org/10.1787/b96cd88a-en)).

A second shared headwind is housing supply and affordability, which shows up twice, first as a social strain, second as an economic constraint that blocks labor mobility and allocative efficiency. The US literature is unequivocal: quantify that local housing constraints in high-productivity US cities lowered aggregate US growth by 36% over 1964–2009((Hsieh, C.-T., & Moretti, E. (2019). Housing constraints and spatial misallocation. American Economic Journal: Macroeconomics, 11(2), 1–39. https://doi.org/10.1257/mac.20170388)), implying sizable ongoing costs when approvals and density remain constrained. Canada’s public bodies document similar frictions, CMHC and the Bank of Canada both link the housing bottleneck to misallocated capital and decades-long declines in labor-productivity growth, which only barely turned positive in late 2024 after three straight years of decline((Bank of Canada. (2024, March 26). Time to break the glass: Fixing Canada’s productivity problem [Speech]. https://www.bankofcanada.ca/wp-content/uploads/2024/03/remarks-2024-03-26.pdf)).

For countries that traditionally relied on their global financial reach, universities, and scientific ecosystems, the lack of diffusion of these advantages across the wider economy is proving costly in comparative terms. Without targeted reforms to unlock productivity gains, improve governance coherence, and ease labour and housing constraints, the Anglosphere risks further slippage in future editions of the index.

Bottom line for projections: without faster diffusion (from frontier firms to the median firm), housing/planning reform(to restore mobility and scale), and targeted human-capital & permitting fixes (to raise investment per worker), these four economies are likely to keep losing relative position in comprehensive, multi-pillar benchmarks like your GPI, even if headline innovation capacity remains strong. Conversely, credible moves on those three levers would mechanically lift measured productivity, ease allocative frictions, and improve governance perceptions, precisely the ingredients Europe’s top performers have sustained.

Latin America

Latin America has not produced major shifts in GPI 2025. Chile (47th) remains the highest-ranked country in the region but has slipped modestly, reflecting concerns about political uncertainty and productivity stagnation. Brazil (50th) and Argentina (51st) continue to underperform relative to their potential, weighed down by fiscal volatility and institutional instability. Mexico (62nd) remains mid-ranked, balancing economic weight with governance challenges. Smaller states provide more positive stories: Uruguay (54th) and Costa Ricam(58th) perform relatively well thanks to stability and strong investment in education and social capital. Caribbean states such as Barbados((For Barbados, this move enhances the substantive value of its passport: citizens will now enjoy indefinite stay, work and settlement rights across these states, along with access to health and education services, strengthening the “mobility” dimension beyond mere visa counts. This deeper integration not only raises Barbados’s regional standing but could also signal to multinational partners and global mobility indices that the island is evolving into a more connected, high-mobility jurisdiction. As the agreement becomes operational and potentially expands, Barbados is poised to improve its ranking in the Enhanced Mobility dimension of the Global Passport Index, provided the arrangements are smoothly implemented and documented. Caribbean Community Secretariat. (2025, September 30). Barbados, Belize, Dominica and St. Vincent and the Grenadines ready for full free movement on 1 October 2025. CARICOM. https://caricom.org/barbados-belize-dominica-and-st-vincent-and-the-grenadines-ready-for-full-free-movement-on-1-october-2025/)) (59th) and Saint Lucia (67th) benefit from niche strategies but remain vulnerable to external shocks. Overall, the region demonstrates resilience but still need structural transformations for a major leap forward.

The region shown improvements since the pandemic but are increasingly constrained by structural drag. The IMF’s Regional Economic Outlook for the Western Hemisphere estimates growth slowing from about 2.3 % in 2023 to 2.0 % in 2024 for the region, with potential growth averaging only 2.5 %, well below what’s needed to catch up with more dynamic emerging economies((International Monetary Fund. (2024, April 19). Regional Economic Outlook — Western Hemisphere, April 2024. https://www.imf.org/en/Publications/REO/WH/Issues/2024/04/19/regional-economic-outlook-western-hemisphere-april-2024)). Labor productivity growth has been particularly weak, and external challenges (commodity price volatility, weaker global demand, tighter financing) amplify internal constraints((International Monetary Fund. (2024, April 19). Regional Economic Outlook — Western Hemisphere, April 2024. https://www.imf.org/en/Publications/REO/WH/Issues/2024/04/19/regional-economic-outlook-western-hemisphere-april-2024)).

One big theme is institutional and governance weaknesses. The UNDP/CAF “Governance for Development in Latin America and the Caribbean” initiative flags that many countries face fragile legitimacy of public institutions, weak rule of law, and capacity constraints(( CAF – Development Bank of Latin America and the Caribbean, & United Nations Development Programme. (2024). Governance for Development in Latin America and the Caribbean: Recommendations from CAF and UNDP Dialogues. https://www.undp.org/sites/g/files/zskgke326/files/2024-09/governance_for_development_in_latin_america_and_the_caribbean.pdf)). Credible public administration is uneven, corruption remains a frequent friction, and the ability of governments to impose regulatory consistency is uneven across countries. According to the BTI 2024 regional data, many Latin American states suffer from what is described as “negative stagnation”, where socioeconomic development is flat or deteriorating modestly, even absent large shocks((Macias-Weller, A., & Thiery, P. (2024). BTI 2024: Regional report Latin America and the Caribbean – Lost in transformation? (Report). Bertelsmann Stiftung. https://bti-project.org/fileadmin/api/content/en/downloads/reports/global/BTI_2024_Regional_Report_LAC.pdf BTI 2024+2bertelsmann-stiftung.de+2)).

Another recurring constraint is demographics & informal labour markets. Latin America saw very strong growth in its working-age population in the two decades prior to COVID-19, but that momentum is shifting: slower workforce growth, aging in some countries, lower labour force participation (especially amongst women) are all dampening growth potential((International Monetary Fund. (2024, April 19). Regional Economic Outlook — Western Hemisphere, April 2024. https://www.imf.org/en/Publications/REO/WH/Issues/2024/04/19/regional-economic-outlook-western-hemisphere-april-2024)). For instance, the IMF in recent working papers underscores that informal firms tend to under-invest in technology, link poorly to export or global value chains, and suffer more from financing constraints((International Monetary Fund. (2024, April 19). Regional Economic Outlook — Western Hemisphere, April 2024. https://www.imf.org/en/Publications/REO/WH/Issues/2024/04/19/regional-economic-outlook-western-hemisphere-april-2024)).

There is some positive movement and opportunities, particularly among nations that manage to combine reform, better governance, and external integration or niches of excellence. Countries like Costa Rica, Uruguay, and sometimes Chile stand out in comparison to many peers, they often score better on stability, rule of law, education metrics. Also, technological adoption (e.g. in AI, digital government) is being explored as a lever: a recent IMF paper argues that Latin America could see substantial gains if more systemic adoption of AI and other advanced technologies is coupled with reforms in labour markets, formalization, access to finance, and regulatory environment((Bakker, B. B., Chen, S., Vasilyev, D., Bespalova, O., Chin, M., Kolpakova, D., Singhal, A., & Yang, Y. (2024). What can artificial intelligence do for stagnant productivity in Latin America and the Caribbean? (IMF Working Paper No. 2024/219). International Monetary Fund. https://doi.org/10.5089/9798400290770.001 )).

The Caribbean

The Caribbean presents one of the more distinctive regional profiles in GPI 2025, as a cluster of small islands developing states (SIDS) that rely heavily on tourism, services, and increasingly on niche economic models such as citizenship-by-investment (CBI) programs. Following the sharp pandemic shock of 2020–2021, the region experienced a strong rebound driven by tourism: the IMF’s Caribbean Region Outlook notes that visitor arrivals in several destinations exceeded 2019 levels by 2023, supporting GDP growth of around 9–10% annually in Antigua and Barbuda, Saint Kitts and Nevis, and Saint Lucia during the recovery phase((International Monetary Fund. (2024, April 19). Regional Economic Outlook – Western Hemisphere [Report]. https://www.imf.org/en/Publications/REO/WH/Issues/2024/04/19/regional-economic-outlook-western-hemisphere-april-2024)). This bounce is reflected in the upward movement of some Caribbean countries in the GPI, such as Antigua and Barbuda (+14 since 2021), Saint Kitts and Nevis (+10), Saint Lucia (+8), Dominica (+8) and Grenada (+4). These gains illustrate how global mobility and niche investment regimes can translate directly into improved standing in composite indices.

Governance and policy frameworks also shape outcomes. The 5 CBI states have leveraged these programs to fund infrastructure, diversify government revenue, and integrate into global networks. CBI revenues remain vital for several Caribbean economies. Antigua and Barbuda reported record-breaking sales over the same period. Dominica continues to rely heavily on its program, with CBI inflows estimated at around 35–40% of GDP, underscoring its fiscal weight. In contrast, Grenada and Saint Lucia recorded application declines, leading to lower revenues((Quinland-Donavan, C. (2024, September 12). Antigua and Barbuda reports record-breaking CBI sales as St. Kitts and Nevis programme fallout boosts rival islands. Times Caribbean Online. https://timescaribbeanonline.com/antigua-and-barbuda-reports-record-breaking-cbi-sales-as-st-kitts-and-nevis-programme-fallout-boosts-rival-islands/timescaribbeanonline.com)). Collectively, these figures highlight both the scale and volatility of CBI earnings in the region and the importance of policy reforms to ensure sustainability amid shifting global standards. Looking forward, the Caribbean’s position in the GPI will depend on how successfully it can diversify its economies, strengthen climate resilience, and align CBI programs with international norms. Countries that pair investment inflows with digital transformation, renewable energy adoption, and better disaster-risk management are more likely to sustain their improved rankings. Without such reforms, the Caribbean risks seeing its recent gains eroded by external shocks, leaving the region’s GPI trajectory highly volatile in the years ahead.

In sum, over the past years the CBI nations have shown consistent improvement across all dimensions of the GPI. Their progress reflects both targeted policy evolution and structural resilience. Initially propelled by mobility gains through expanded visa-free agreements and stronger diplomatic engagement, these countries have increasingly translated external access into internal advantages. Enhanced governance standards, macroeconomic stability, and continued investment in education, infrastructure, and sustainability have all contributed to a more balanced profile across Quality of Life, Investment, and Enhanced Mobility. CBI programs themselves have matured (focusing on transparency, due diligence, and diversification of investment inflows) thereby reinforcing economic stability and international credibility. Together, these elements have elevated the Caribbean CBI states from niche investment hubs to globally recognized jurisdictions where strategic openness, lifestyle quality, and trust in governance combine to strengthen both passport value and overall national performance.

In the long term, if Latin America is to improve or even maintain GPI-rank positions, several levers will matter such as strengthening institutions (rule of law, consistency, governance capacity), reducing informality and improving the quality of work, investing in human capital and digitalization, improving financing access for small and medium firms, and integrating more into global trade/value chains.

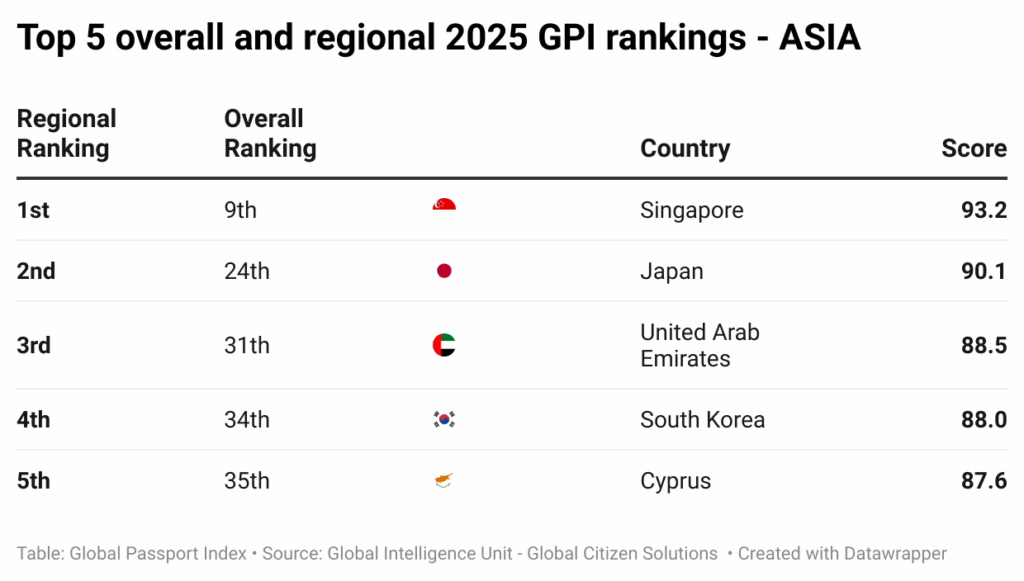

Asia

In Asia, the headline is Singapore’s (9th) steady rise into the global top ten, marking it as the sole non-European state in that elite club. Its success reflects long-term policy choices emphasizing innovation, education, and predictable regulation. However, other major Asian economies tell a different story. South Korea (34th) and Hong Kong (43rd) both slipped several positions, constrained by demographic headwinds, rising costs, and governance concerns. Japan (24th) remained in the same position as previous years, but outside the top twenty, reflecting stability rather than dynamism.

Southeast Asian countries like Malaysia (48th) remain mid-ranked, pointing to the need for deeper structural reforms to climb higher. The region overall illustrates that Asia can produce exceptional leaders but also suffers from sharp divergence depending on institutional and demographic trajectories.

Asia-Pacific remains among the fastest-growing global regions, but the region’s internal dynamics are increasingly complex, some countries are rising fast in the GPI, while others are held back by structural constraints. According to the IMF’s Regional Economic Outlook: Asia and Pacific the region’s growth rate is projected at about 4.6 % in 2024 and tapering to 4.4 % in 2025, despite headwinds((International Monetary Fund. (2024, October 31). Regional Economic Outlook: Asia and Pacific – November 2024 (IMF Staff Report). https://www.imf.org/en/Publications/REO/APAC/Issues/2024/10/31/regional-economic-outlook-for-asia-and-pacific-october-2024 [PDF].)).

Key drags include aging and demographic decline, especially in advanced economies of East Asia and in territories like Japan, South Korea, and Hong Kong. The IMF and other multilateral agencies warn that falling fertility rates are already reducing the size of the working-age population, which in turn dampens GDP per capita growth, labor force participation and raises dependency burdens((International Monetary Fund. (2024, October 31). Regional Economic Outlook: Asia and Pacific – November 2024 (IMF Staff Report). https://www.imf.org/en/Publications/REO/APAC/Issues/2024/10/31/regional-economic-outlook-for-asia-and-pacific-october-2024 [PDF] and World Bank. (2023). Falling long-term growth prospects: Trends, expectations, and policies. World Bank Group. https://doi.org/10.1596/978-1-4648-1925-5)). Meanwhile, countries which still have demographic advantage tend to face skill mismatches, informal employment, and underinvestment in human capital.

What does this imply in GPI terms? Countries like Singapore benefit from combining strong human capital, high institutional quality, good regulatory regimes, and stable demographics. These allow them to maintain or improve rankings even as innovation cycles slow globally. Meanwhile, economists warn that in countries where demographic decline, regulatory bottlenecks, or weak diffusion persist, upward mobility is harder. The World Bank’s Firm Foundations of Growth shows that constraints in bottom quartile manufacturing firms (e.g. low access to finance, inefficient infrastructure) remain a persistent drag((World Bank Group. (2025, June 2). Firm Foundations of Growth: Productivity and Technology in East Asia and Pacific(Report). https://documents.worldbank.org/en/publication/documents-reports/documentdetail/099060425124520747)). Thus in GPI 2025 we see Asia-Pacific reflecting both the upside of policy coherence (in some) and the downside of structural constraints (in others).

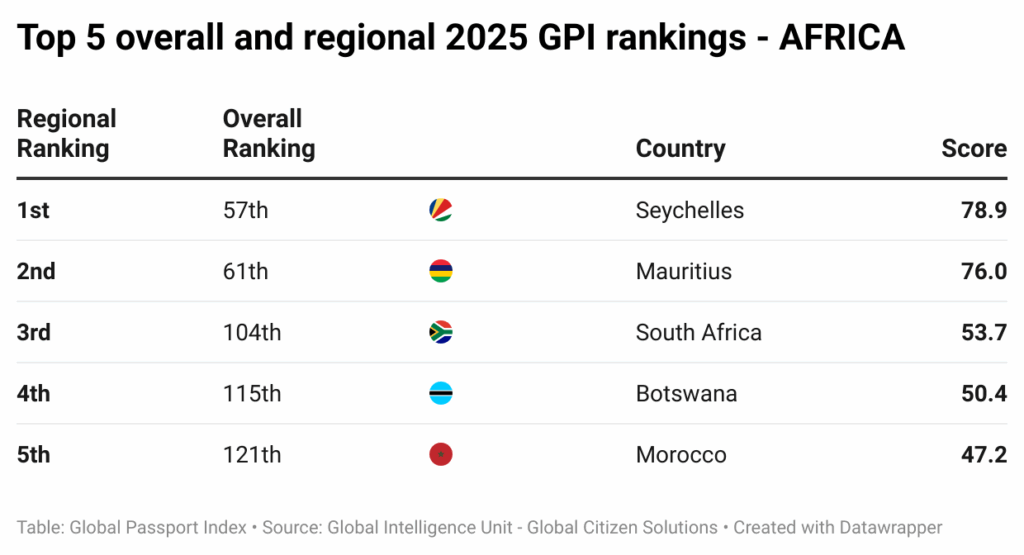

Africa

Africa continues to occupy the more modes tiers of the index, though with a few notable outliers. Mauritius and Seychelles retain comparatively high positions due to their specialization in tourism and financial services, but their progress remains fragile. South Africa leads the continent but sits outside the top 100, reflecting the tension between infrastructure strengths and governance weaknesses. North African economies such as Morocco, Tunisia, and Egypt are mid- to lower-ranked, struggling with demographic pressures and fiscal constraints. Sub-Saharan states like Nigeria, Kenya, and Ghana face persistent obstacles in institutional capacity, productivity, and exposure to climate shocks. The regional pattern is one of stability rather than transformation, underlining the scale of reforms required for upward convergence.

South Africa’s position as third in Africa and 104th globally in the 2025 GPI reflects both its enduring regional importance and its structural limitations in translating potential into passport strength. South Africa maintains a moderate level of mobility, allowing its citizens access to numerous destinations across Africa, Europe, and parts of Asia, yet it lags far behind global leaders in travel freedom and overall competitiveness. This middle-ground position mirrors the broader state of the South African economy: a country rich in infrastructure, institutional maturity, and global connections, but constrained by persistent governance challenges, inequality, and sluggish reform momentum.

In essence, South Africa’s GPI standing highlights a dual narrative: it remains one of Africa’s most globally connected nations, yet it has failed to leverage this position into sustained upward mobility. Strengthening the rule of law, modernizing infrastructure, and rebuilding investor confidence could enable South Africa to convert its latent advantages into greater global access and influence.

In general, Africa remains a region of low average performance in most global indices similar to GPI, with a few notable exceptions. According to the IMF’s Sub-Saharan Africa Regional Economic Outlook (October 2024), growth is projected at about 3.6% in 2024, roughly matching 2023; there is forecasted modest acceleration to around 4.2% in 2025((Ecofin Agency. (2024, October). Sub-Saharan Africa economic growth outlook: Moderate recovery continues amid global uncertainty. Ecofin Agency. https://www.ecofinagency.com))((International Monetary Fund (IMF). (2024, October). Regional economic outlook: Sub-Saharan Africa – Strengthening resilience in a turbulent world. Washington, DC: International Monetary Fund. https://www.imf.org/en/Publications/REO)). While positive, those growth rates are generally insufficient to close the gap with high-income countries or to deliver rapid improvements in institutional, innovation, or governance dimensions of the GPI. In per-capita terms, growth is often much slower because population growth remains high((International Monetary Fund (IMF). (2024, October). Regional economic outlook: Sub-Saharan Africa – Strengthening resilience in a turbulent world. Washington, DC: International Monetary Fund. https://www.imf.org/en/Publications/REO)).

A major constraint is employment, especially the prevalence of informal labor markets and underemployment. The IMF highlights that Sub-Saharan Africa faces an urgent job creation challenge, creating sufficient formal, higher-productivity employment to absorb a young, rapidly growing population((International Monetary Fund (IMF). (2024, October). Regional economic outlook: Sub-Saharan Africa – Strengthening resilience in a turbulent world. Washington, DC: International Monetary Fund. https://www.imf.org/en/Publications/REO)). Without raising the quality of jobs (not just the quantity), countries’ overall performance in composite indices declines or stagnates, because weak livelihoods, low productivity per worker, and high informality corrode many of the pillars used in indexes like GPI (governance, economic opportunity, human development).

Governance and public legitimacy also show mixed signals. On one hand, some countries are investing strongly in digital infrastructure, civic tech, youth engagement, and governance reforms. For example, several studies (e.g., “Challenges, Opportunities and New Trends in Governance Innovation across Africa”) point to increased adoption of digital government tools, upticks in civic oversight, and pushbacks against corruption through transparency initiatives((Public Administration Network – United Nations Department of Economic and Social Affairs (UNDESA). (2024). Challenges, opportunities and new trends in governance innovation across Africa. United Nations. https://publicadministration.desa.un.org)). On the other hand, political instability, coups, weak rule of law, and uneven accountability remain real drags. The Mo Ibrahim Index and Afrobarometer surveys show declining trust in governance in many countries, increased perception of corruption, and challenges in sustaining democratic institutions. These dynamics likely weigh heavily in composite indices((The Guardian. (2024, September). Africa’s democratic backsliding and the governance trust gap. The Guardian. https://www.theguardian.com)).

Looking ahead, if Africa is to make visible gains in the GPI, several levers matter: improving governance (rule of law, corruption controls), transforming informal sectors into more formalized, productive work, investing in human capital (education, health), boosting digital infrastructure and innovation diffusion, and anchoring economic growth in diverse, resilient sectors (not just extractives or commodities).

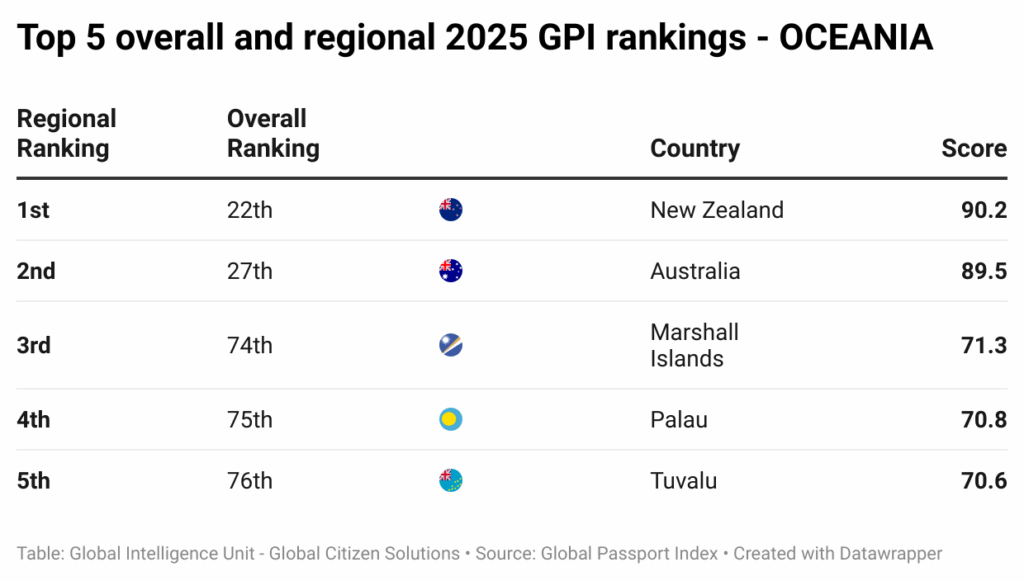

Oceania

Oceania stands out as a region of extraordinary contrasts and resilience, a vast expanse anchored by two globally integrated economies, Australia and New Zealand, surrounded by a constellation of small Pacific island states like Palau, Tuvalu, and the Marshall Islands. Together they form a region of high stability, strong human development, and enviable natural endowments. Yet, when examined through the lens of the Global Passport Index, the data reveals a story of both enduring strength and gradual drift. While Australia and New Zealand continue to dominate regionally, their global standing has slipped.

In 2025, New Zealand ranks 22nd and Australia 27th, far ahead of their Pacific neighbors but well below their 2021 positions, when New Zealand held 10th and Australia 18th place globally. This decline reflects less a loss of reputation than a shift in relative dynamism, as other nations (particularly in Europe and Asia) moved more swiftly to expand travel liberalization, deepen digital integration, and attract mobile talent in the post-pandemic years.

However, the erosion of passport power in Oceania’s leading economies parallels the emergence of deep structural constraints at home, particularly in housing. Over the past decade, housing has evolved from a cyclical market issue into a systemic brake on productivity and mobility across both Australia and New Zealand. Policy diagnostics now converge: the he OECD’s housing reviews call out restrictive planning/zoning and slow approvals as binding frictions, and Australia’s Productivity Commission makes the same point explicitly in its five-year inquiry (recommendations to relax planning constraints and replace stamp duties)((Organisation for Economic Co-operation and Development. (2021). Addressing complex housing policy challenges should be a central priority for governments [Press release]. https://www.oecd.org/about/news/press-releases/2021/06/addressing-complex-housing-policy-challenges-should-be-a-central-priority-for-governments.html and Organisation for Economic Co-operation and Development. (2023). An agenda for housing policy reform: Making housing markets work better across the OECD (OECD Publishing). https://www.oecd.org/en/publications/an-agenda-for-housing-policy-reform_ddb57031-en.htm )). Australia’s Productivity Commission goes further, advocating planning liberalization through more by-right density around jobs and transport hubs, transparent infrastructure contributions, and a replacement of stamp duties with a broad-based land tax to reduce lock-in effects and improve allocative efficiency.

In Australia, new evidence shows housing construction productivity has halved per hour worked compared to 30 years ago, amplifying the supply crunch and keeping prices elevated even as demand rotates((Tulip, P. (2024, October 15). Land use restrictions and the Australian housing policy debate. The Centre for Independent Studies. https://www.cis.org.au/publication/land-use-restrictions-and-the-australian-housing-policy-debate/))((Productivity Commission. (2025, February 16). Housing construction productivity: Can we fix it? Research paper, Canberra. https://www.pc.gov.au/research/completed/housing-construction/)). In New Zealand, IMF analysis points to similarly weak investment incentives and low diffusion, particularly among small, young, high-growth firms that face persistent financing and regulatory barriers((International Monetary Fund. (2025, June 10). New Zealand’s productivity challenge: New Zealand (Selected Issues Paper No. 2025/075). IMF. https://doi.org/10.5089/9798229012317.018)). When small and medium enterprises cannot scale into mid-sized builders or innovative prefab manufacturers, the construction ecosystem remains thin, costs stay sticky, and the pipeline from consent to completion stretches longer. Both economies have effectively trapped themselves in a low-productivity equilibrium, where strong demand collides with rigid supply and rising costs.

The macroeconomic consequences are visible in the indicators the GPI captures indirectly. Quality of life and investment dynamism decline when housing is scarce, expensive, and slow to deliver. High housing costs compress real disposable incomes, inflate business overheads, and curtail labor mobility, people cannot move to where the jobs are, so productivity gains at the frontier fail to diffuse to the wider economy. Over time, this erodes two of the three pillars that underpin passport strength: the Investment & Innovation dimension, as capital formation and firm scaling slow, and the Quality of Life dimension, as housing affordability, commuting stress, and social well-being deteriorate. In effect, housing has become a national macro constraint rather than a niche sectoral challenge, pulling down not only domestic living standards but also the global perception of competitiveness and opportunity reflected in international indices.

Unlocking progress will require more than incremental policy adjustments; it calls for a coordinated reform package that restores productivity and mobility alike. The evidence points to three interlocking levers. First, supply-side planning reform: up-zone near transit and employment centers, codify by-right mid-rise density, set statutory approval timelines, and use pattern books and pre-approved modular designs to compress delivery timeframes. Second, tax reform: replace stamp duties with annual land value taxation to reduce lock-in, encourage efficient land use, and fund local infrastructure without penalizing transactions. Third, industrial and finance policy: scale up off-site manufacturing, establish predictable demand pipelines through long-term public housing tenders, and expand patient finance for mid-tier builders to spread productivity gains across the sector. Complementary steps, digitized permitting, shared utilities corridors, and workforce training in modern construction methods, can accelerate impact.

Across the rest of Oceania, smaller island states such as the Marshall Islands, Palau, and Tuvalu remain stable but low-ranked, typically between 70th and 80th place. Their challenges (climate vulnerability, narrow economic bases, and dependence on remittances) limit progress in global mobility or investment attraction. Together, these trends highlight a broader regional pattern: while Oceania remains prosperous and secure, its two leading economies have lost some of the global momentum that once made their passports among the world’s most desirable. The 2025 snapshot thus reflects a pivot from dominance to resilience, as Australia and New Zealand adapt to a more competitive and rapidly evolving global mobility landscape.

Europe: Consolidate Leadership Through Integration and Quality of Life

- Deepen Continental Integration: Expand the Schengen area and enhance mutual recognition of professional qualifications. EU and non-EU neighbors (e.g., Western Balkans) should accelerate convergence programs to reinforce institutional stability and talent mobility.

- Invest in Social Infrastructure: Maintain Europe’s competitive edge in quality of life through robust health systems, green housing, and affordable mobility within cities. These elements feed directly into GPI’s Quality of Life dimension.

- Spread Innovation Eastward: Establish targeted funds to replicate Nordic-style R&D ecosystems in Eastern and Southern Europe. Encourage joint digital-sovereignty projects, ensuring that innovation diffusion extends beyond frontier economies.

- Governance Renewal: Address bureaucratic fragmentation through interoperable data systems and transparent procurement, raising both efficiency and trust.

Asia: Reform for Inclusivity, Demographics, and Mobility

- Institutionalize Predictable Governance: Other Asian nations can be inspired by Singapore’s regulatory stability and transparent business climate to attract talent and capital. Predictability is a key GPI differentiator.

- Demographic and Labor Policy Reform: Japan and South Korea need proactive migration and family-support policies to offset aging populations. Programs for skilled immigration and gender-inclusive labor participation will sustain innovation capacity.

- Strengthen Regional Connectivity: ASEAN should operationalize its travel-corridor initiatives (digital IDs, e-visa harmonization, and mutual skill recognition) to lift regional Enhanced Mobility scores.

- Expand Human-Capital Investment: Introduce AI-driven education reforms and vocational upskilling to align with industry demand, linking education directly to productivity growth.

Anglo America: Restore Diffusion, Housing, and Governance Coherence

- Rebuild Housing and Mobility Infrastructure: Simplify zoning, reduce permitting delays, and expand affordable housing to restore labor mobility and productivity diffusion.

- Diffuse Innovation Nationwide: Strengthen mid-sized firms through tax incentives and digital-adoption grants, ensuring frontier technologies benefit entire economies.

- Reinforce Institutional Credibility: Depoliticize fiscal planning, modernize regulatory agencies, and enhance transparency to rebuild international confidence.

- Re-energize Mobility Diplomacy: Negotiate new visa-waiver and pre-clearance arrangements with the EU, ASEAN, and Gulf Cooperation Council to regain Enhanced Mobility strength.

Latin America: Move From Resilience to Transformation

- Institutional Deepening: Implement credible judicial reforms, streamline bureaucracies, and strengthen anti-corruption mechanisms to enhance investor confidence.

- Formalize Labor Markets: Incentivize digital payrolls and social contributions for SMEs, expanding the tax base and improving Quality of Life scores through social protection.

- Harness Technological Transformation: Support AI and digital-government projects that increase transparency and reduce inefficiencies.

- Enhance Regional Integration: boost region mobility scaffolding (MERCOSUR Residency, Andean Community, Pacific Alliance, SICA/CA-4, and CARICOM/CSME) that can fast-track intra-regional travel and employment.

- Targeted Education Investment: Prioritize STEM and vocational training to raise productivity and attract knowledge-based industries.

Caribbean: Convert Mobility Gains Into Structural Strength

- Economic Diversification: Channel CBI revenues into sustainable tourism, renewable energy, education, and climate resilience. Diversified investment strengthens both the Investment & Innovation and Quality of Life pillars.

- Diplomatic Expansion: Leverage collective bargaining to secure additional visa-waiver deals with Europe’s periphery, the Middle East, and Asia.

- Fiscal Responsibility: Use CBI inflows to fund debt reduction and infrastructure, ensuring long-term stability beyond the program’s immediate fiscal returns.

Africa: Build Capacity, Trust, and Regional Integration

- Governance Reform: Strengthen rule of law, transparency, and accountability through digital governance tools and civic-tech platforms.

- Expand Regional Mobility: Fast-track the African Union e-passport and fully implement ECOWAS and EAC free-movement protocols to lift intra-continental connectivity.

- Invest in Human Capital: Increase funding for education and health; align curricula with emerging sectors like fintech and renewable energy.

- Economic Diversification: Shift from commodity dependence toward industrial and digital sectors. Create SEZs with efficient logistics and power reliability.

- Climate and Infrastructure Resilience: Integrate green energy and digital infrastructure projects to attract sustainable investment and raise Quality of Life metrics.

Oceania: Reverse Drift Through Housing and Innovation Reform

- Comprehensive Housing Reform: Liberalize zoning near employment centers, introduce land-value taxation to replace stamp duties, and expand modular construction to boost affordability and labor mobility.

- Stimulate Innovation Diffusion: Provide financing for mid-tier companies in renewable energy, digital services, and green infrastructure to expand the Investment & Innovation pillar.

- Enhance Regional and Global Mobility: Expand youth-mobility schemes and mutual visa recognition with Asia and Europe to improve Enhanced Mobility scores.

- Support Pacific Neighbors: Develop joint climate-adaptation funds and shared digital infrastructure to ensure stability and collective upward movement in GPI rankings.

The Global Passport Index 2025 confirms that the true strength of a passport is no longer defined by raw counts of visa-free entries alone.

Europe’s nine-out-of-ten dominance (anchored by Sweden’s leadership and reinforced by Finland, Denmark, Switzerland, and Germany) reflects compounding advantages: predictable rule of law, dense human-capital pipelines, interoperable markets and standards, and welfare systems that reduce risk for households and entrepreneurs alike. Singapore’s presence in the top ten illustrates that this formula can travel: coherent policy, diffusion of innovation, and regulatory predictability can elevate even small states to global standouts.

At the same time, the Anglosphere’s decline underscores how structural frictions (weak productivity diffusion beyond frontier firms, housing supply constraints, and policy unpredictability) now register visibly in comprehensive benchmarks. Asia’s mixed picture, Latin America’s resilience without transformation, and Africa’s incremental progress all point to a common lesson: upward mobility in the GPI requires both the creation of capabilities (innovation, skills, infrastructure) and their broad diffusion through effective governance and market design. Where reforms deepen capital formation, formal employment, and integrated market access, rankings improve; where they stall, position erodes despite headline strengths.

Four years of comparable data now make the trendlines clear. Countries rise and stay elevated when they invest consistently in the “inputs that compound”: trust-rich governance, human capital, R&D intensity, digital and green infrastructure, and high-value mobility networks. These fundamentals are also the most shock-resistant, explaining the Nordics’ persistent excellence and the rapid gains of EU converges such as Estonia and Croatia following concrete integration milestones. Conversely, economies that rely on narrow engines of growth or transient boosts (be it tourism cycles or financial inflows untethered to broader capability building) see more volatile trajectories.

For investors, policymakers, and globally minded individuals, the practical implications are straightforward. Use mobility strategically, but judge passports by the quality of doors they open and the stability behind them. Seek ecosystems where innovation is financed and diffused, not merely invented. Prioritize jurisdictions that de-risk life and business through reliable institutions, competitive tax and regulatory frameworks, and social infrastructure that sustains talent. For governments aiming to climb the index, three levers recur across the data: (1) accelerate diffusion, of technology, skills, and finance, beyond frontier firms; (2) unblock housing and planning to restore labor mobility and raise productivity; and (3) lock in credibility with rule-of-law reforms, predictable taxation, and transparent program design (including any investment-migration channels).

The GPI was built to track not just where countries stand, but how and why they move. In 2025, its multi-dimensional lens shows a fragmented yet legible landscape: Europe consolidates, select Asian innovators break through, and others drift depending on reform momentum. Looking ahead, the countries most likely to rise are those that match innovation with institutional depth and integration, turning access into advantage, and advantage into broad-based prosperity. The ones that do will not only climb the rankings; they will convert passport strength into lived opportunity for their citizens.