In 1987, the United Nations Brundtland Commission defined sustainability as “meeting the needs of the present without compromising the ability of future generations to meet their own needs” (Brundtland Commission, 1987). Nearly four decades on, that definition has become a widely referenced benchmark against which states, capital, and policy instruments are being assessed.

Investment migration is increasingly becoming a key mechanism for attracting foreign direct investment, particularly in smaller economies. Sovereign states, ranging from the largest and most powerful economies to smaller peripheral ones, run citizenship and residency programs to attract talent, experience, and capital. As this research highlights in the following sections, the programs were originally designed around fiscal need, not for developmental purposes. Yet a growing body of practice and analysis suggests they now contribute, directly and measurably, to the United Nations Sustainable Development Goals.

This briefing examines investment migration through the lens of sustainability, tracing how the sector has evolved, and introduces the concept of sustainable citizenship.

The central argument of the briefing is twofold. First, investment migration programs increasingly mirror the broader sustainability commitments the international community has formalized, and they do so with measurable fiscal effect. Second, the sector is moving away from its original capital-only model and toward purpose-driven citizenship, in which qualifying capital is channeled into legislated funds, regulated investment vehicles, and earmarked donations tied to defined developmental outcomes.

What follows is an account of how that shift has taken shape, where it is most advanced, and what it implies for the future of citizenship as a category.

Defining Citizenship

Kochenov (2019) argues that citizenship is essentially arbitrary, assigned at birth without consent yet shaping lifelong opportunities, rights, and freedoms. Building on this, Kochenov (2021) introduces the concept of “victims of citizenship” to describe the majority of the world’s population who are constrained by a status they did not choose. A parallel argument frames birthright citizenship in affluent states as inherited property: a valuable bundle of entitlements transmitted by law on grounds (place of birth) that would be indefensible in almost any other legal domain (Shachar, 2009).

This arbitrariness has, in recent decades, been challenged by new mechanisms. Surak (2023) argues that citizenship is no longer strictly tied to blood (jus sanguinis) or soil (jus soli). Individuals can now expand their opportunities through legal and financial means, captured by the term jus pecuniae, originally coined by Stern (2012) and later expanded to encompass citizenship acquired through substantial financial contributions. These programs enable governments to attract foreign capital while individuals gain access to greater stability, security, and mobility.

Jus Pecuniae or Investment Migration

The institutional expression of jus pecuniae is the investment migration sector. Since the 2008 financial crisis, an increasing number of states have offered citizenship, and residence permits in exchange for qualifying investments. The exchange rests on two corresponding interests: the individual obtains status, mobility, and jurisdictional optionality; the state obtains fiscal revenue and foreign direct investment. The structure of qualifying investment has evolved. Early programs relied predominantly on passive real estate acquisition. More recent program design has shifted capital toward channeled, regulated vehicles: legislated national development funds in the Caribbean and regulated alternative investment funds with explicit sectoral mandates in Europe. This shift brings investment migration into direct contact with the regulatory infrastructure that governs sustainable finance more broadly.

ESG-Linked Funds and Sustainable Finance

Environmental, Social, and Governance (ESG) investing has grown from a niche strategy into a mainstream framework that integrates non-financial criteria into investment decision-making (Sciarelli, Cosimato, Landi, & Iandolo, 2021). In the European Union, the Sustainable Finance Disclosure Regulation (SFDR) imposes mandatory sustainability disclosure obligations on financial market participants, distinguishing baseline Article 6 products from Article 8 (products promoting environmental or social characteristics) and Article 9 (products with sustainable investment as their objective). As investment migration shifts toward fund-based routes, most visibly in Portugal, the eligible vehicles operate within the SFDR disclosure perimeter, with a growing share positioning themselves under Article 8 or Article 9 classifications. SFDR gives this convergence a regulatory anchor, allowing sustainability claims attached to fund-based programs to be classified, disclosed, and assessed against a common standard.

Impact investing has emerged as a significant segment of global finance, enabling investors to generate positive social and environmental outcomes alongside financial returns. According to the Global Impact Investing Network (GIIN), more than 3,900 organizations managed an estimated US$1.57 trillion in impact investing assets worldwide in 2024, reflecting a 21% compound annual growth rate since 2019 (GIIN, 2024). The sector is driven by increasing investor interest in addressing challenges such as climate change, affordable housing, healthcare, education, and sustainable infrastructure while achieving competitive financial performance.

The investor demand for this convergence is supported by broader wealth management research. In the United States, the US SIF Foundation’s 2025/2026 Trends Report placed total US sustainable investment assets at $6.6 trillion, with 46% of surveyed institutions expecting to increase their impact investing activities over the next three years (US SIF, 2025). A Standard Chartered Private Bank survey of HNW and affluent investors across Hong Kong, Singapore, the UAE, and the UK found that 84% of HNW investors were open to shifting funds from philanthropy to sustainable investing, with affordable and clean energy, clean water and sanitation, and good health and well-being identified as the three SDGs of greatest importance (Standard Chartered Private Bank, 2019). More recently, Standard Chartered’s Sustainable Banking Report 2025 found that 87% of UAE HNW investors expressed interest in transition investing, with UAE investors allocating 27% of their portfolios to sustainable investments, the highest share among the eight markets surveyed (Standard Chartered, 2025). This demand is particularly pronounced among younger investors. Morgan Stanley’s Sustainable Signals: Individual Investors 2025 report, surveying 1,765 investors across North America, Europe, and Asia-Pacific, found that 99% of Gen Z and 97% of Millennial investors expressed interest in sustainable investing, with nearly 80% indicating they would choose a financial adviser based on sustainable investing offerings (Morgan Stanley Institute for Sustainable Investing, 2025).

Sustainable Citizenship

These trajectories, the legal acquisition of citizenship, the fund-based reorientation of investment migration, and the mainstreaming of ESG-aligned capital, converge to make sustainable citizenship analytically distinct from other available citizenship or residence program logic such as the ones that require direct investment to real estate.

Sustainable citizenship refers to investment migration programs in which qualifying capital is earmarked, legislated, or fund-channeled toward outcomes that map to recognized sustainability frameworks: climate adaptation, renewable energy transition, sustainable infrastructure, and social development priorities consistent with the Sustainable Development Goals or the European Union sustainable finance taxonomy. The category is distinguished by a deliberate, traceable link between the investment route and a defined developmental outcome, supported either by statute or by regulatory classification.

According to the Investment Migration Council, as of 2024, the investment migration sector generated approximately €20 billion in annual revenue and operated across more than 80 sovereign jurisdictions, with citizenship and residency programs contributing between 10% and 40% of GDP in several microstate economies (Investment Migration Council, 2024).

Between 2023 and 2026, investment migration programs across multiple regions restructured around traceable, channeled capital. The pivot is consistent: programs are moving toward regulated investment vehicles and legislated funds with defined developmental outcomes. The shift is driven by several reinforcing forces:

- Governments are aligning their programs with national development priorities

- Strengthening regional cooperation

- Maturation of sustainable finance frameworks that programs can now plug into.

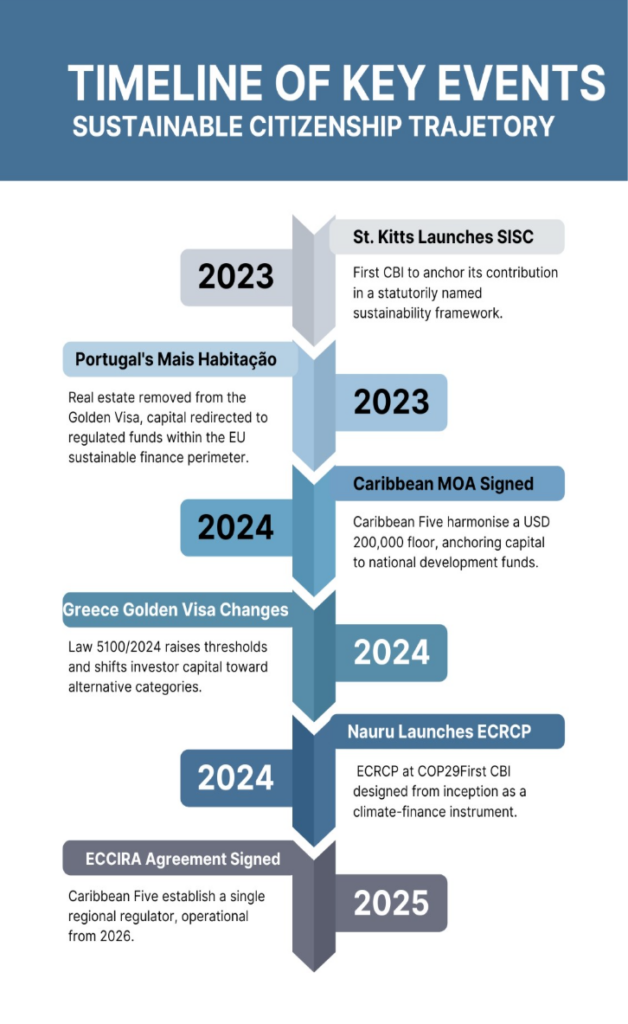

The timeline below traces the key recent events (2023-2026).

The Caribbean’s SISC model and Nauru’s climate-resilience program represent the sovereign-fund version of this evolution. Portugal’s fund route represents the regulated-private-fund version. Both converge on the same logic: capital should be traceable, productive, and tied to a national priority, and this is the institutional foundation on which sustainable citizenship is being built.

It is worth exploring the region that hosts the most investment migration programs offering funds directly linked to sustainability. The structures differ and so do the approaches, and both are worth unpacking.

- St. Kitts and Nevis moved first and went furthest. On 27 July 2023, the older Sustainable Growth Fund was replaced by the Sustainable Island State Contribution (SISC), restructured around seven legislated pillars: local food production, green energy transition, economic diversification, sustainable industries, the creative economy, Covid-19 recovery, and social protections. It remains the only Caribbean program with sustainability written into the contribution route as the organizing principle.

- Dominica took a different route to the same destination. Rather than legislating pillars, it tied its Economic Diversification Fund (EDF) to a single national commitment, namely Prime Minister Skerrit’s September 2017 pledge at the UN General Assembly to make Dominica the world’s first climate-resilient nation by 2030. The 2018 Climate Resilience Act and the National Resilience Development Strategy 2020-2030 turned the pledge into 43 resilience goals and 20 climate targets, with EDF revenue funding resilient housing, the geothermal plant, and the new international airport.

- Grenada pairs development with mobility. The National Transformation Fund (NTF), established under the Grenada Citizenship by Investment Act No. 15 of 2013, channels capital into tourism, agriculture, alternative energy, infrastructure, and education.

- Antigua and Barbuda is the only program with two doors. The National Development Fund (NDF) functions as a general-purpose national fund, while the parallel UWI Fund channels capital directly into regional higher education and includes a one-year University of the West Indies tuition scholarship, the cleanest explicit social-development link anywhere in the bloc.

- Saint Lucia is at the other end of the spectrum. The National Economic Fund (NEF), established under Section 33 of the Citizenship by Investment Act No. 14 of 2015, finances broad national infrastructure such as port expansion, airport redevelopment, and hospital reconstruction, but does not frame these statutorily as sustainability investments.

As Joe Rice, Head of Citizenship Programs at Global Citizen Solutions, observes:

“The framing is shifting from ‘we want your capital’ to ‘we want your contribution.'” The next generation of programs, in his view, will be “purpose-driven, with measurable outcomes attached to the contribution itself.”

Caribbean Programs Through an Analytical Lens

What ties these five programs together, despite their structural differences, is that the capital they channel ends up aligning with the same set of development priorities the international community has formally agreed to pursue. Climate adaptation, clean energy, food security, education, social protection, resilient infrastructure, all map onto specific UN Sustainable Development Goals, and each of the Caribbean Five connects to several of them through its fund architecture. The alignment is uneven, sometimes deliberate, and sometimes a by-product of how the capital is spent, but it is consistent enough to matter. Where multilateral climate finance has consistently under-delivered for Small Island Developing States, CBI revenue has become a parallel channel for the same outcomes the SDG framework was built to deliver.

That parallel channel exists because the official one has not closed the gap. Modelled adaptation costs for SIDS are estimated at USD 5.1 billion per year, but actual public adaptation finance flows to SIDS are only about USD 1.4 billion per year, covering less than one-third of needs. On average, SIDS require 3.4% of GDP annually for climate adaptation, far exceeding the 1.4% required by other developing countries (Grantham Research Institute, 2024). In the Caribbean alone, damage caused by climate-related and earth-related hazards is estimated at USD 12.6 billion per year, and SIDS now experience around 20 major natural disasters per year, compared with fewer than 10 per year before the 2000s (UNCTAD, 2024). Against a shortfall of that scale, investment migration revenue is not a peripheral contribution. For several of these states, it is the fiscal capacity that turns adaptation plans into reality.

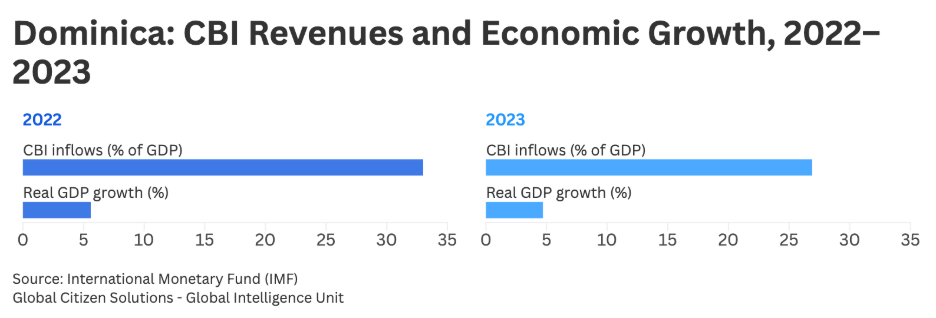

Moreover, the macroeconomic significance is unambiguous. The IMF’s 2024 Article IV consultation for Dominica reports CBI inflows of 33% of GDP in 2022 and 26.9% in 2023, supporting public investment in disaster reconstruction, climate-resilient infrastructure, and the geothermal transition (IMF, 2024). The same consultation attributes the post-pandemic recovery, with real GDP growth of 5.6% in 2022 and 4.7% in 2023, to a rebound in tourism “supported by public investment and buoyant Citizenship by Investment revenues” (IMF, 2024). CBI inflows, equivalent to over a quarter of GDP in both years, directly supported real GDP growth through public investment in climate-resilient infrastructure and tourism recovery, as shown below.

When it comes to St. Kitts and Nevis, the island illustrates the same dependency from the opposite direction. Its 2025 Article IV consultation shows the fiscal deficit widening to -11% of GDP in 2024, driven mainly by a sharp decline in CBI revenue following program reforms (IMF, 2025). Both cases confirm that CBI is not a supplementary revenue stream but an essential one, especially for small-island states.

Europe presents a different picture, built around regulated private funds and earmarked donations. Portugal is the case that drives the shift.

In October 2023, Portugal’s Mais Habitação law removed direct real estate and capital transfer routes from the Golden Visa and restructured qualifying capital around five productive channels (Law 56/2023, Diário da República). Three are recoverable investments: subscription in a CMVM-supervised venture capital or alternative investment fund, capital injection into a Portuguese company combined with job creation, and a standalone job-creation route. The remaining two are non-refundable donations earmarked for specific sectors: cultural production and heritage preservation projects, and public or private scientific research institutions.

The fund route is what brings Portugal into direct contact with European sustainable finance regulation. Funds marketed within the European Union fall under the Sustainable Finance Disclosure Regulation (European Parliament and Council, 2019), which requires financial market participants to disclose how environmental and social characteristics shape their investment strategies. Articles 8 and 9 of the regulation define the classifications used to identify funds that promote ESG characteristics or pursue sustainable investment as their objective. As the Golden Visa fund route has expanded, qualifying vehicles with mandates in renewables, regenerative agriculture, forestry, and the circular economy have proliferated within this disclosure framework. The cultural and research donation routes sit outside the SFDR perimeter but align with other Sustainable Development Goals, including quality education and sustainable cities.

To give a broader context, as Vera Avidano, a product specialist at Global Citizen Solutions, notes: “Even though the fund investment route remains the most popular choice, we are seeing a growing interest in the cultural donation route as well.”

Other European programs follow comparable logic. Italy’s investor visa supports innovative startups and includes a philanthropic donation route covering culture, education, scientific research, and heritage. Hungary’s Guest Investor Program channels capital into MNB-registered funds or university donations, though it retains a direct property route that gives it a more hybrid character than the Portuguese model. Greece’s tiered Golden Visa retains alternative investment fund routes alongside real estate, with the 2024 threshold increases in high-demand zones reflecting housing market pressures rather than a sustainability rationale. None of these programs are framed as sustainability initiatives, but each reflects a broader directional shift in European residency by investment, away from purely real estate-driven structures and toward more institutionally mediated capital flows.

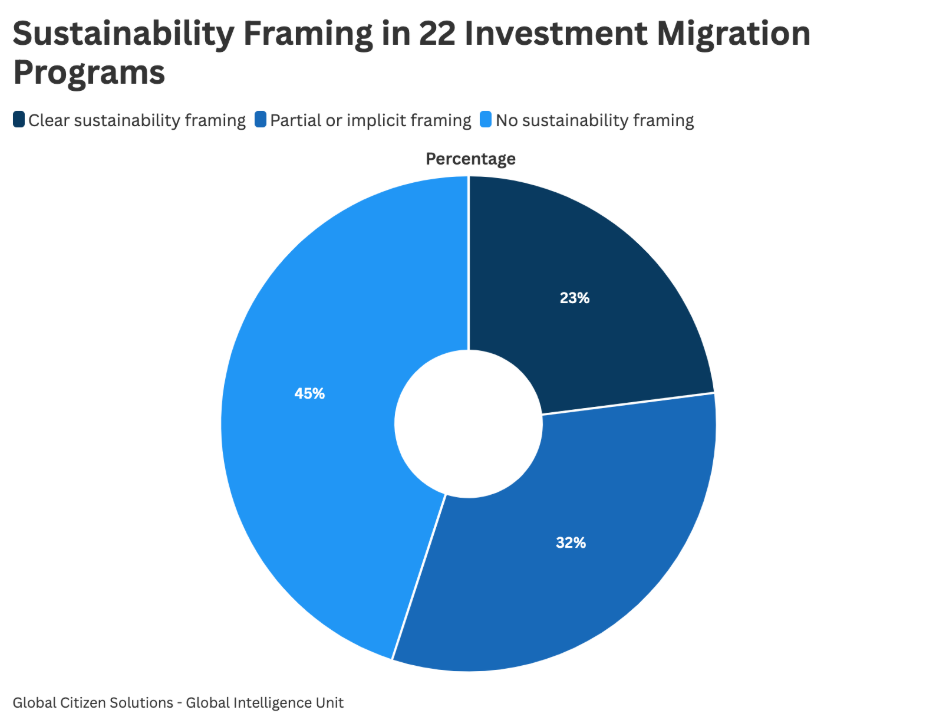

The classification below treats sustainability framing as a spectrum. Some programs have sustainability anchored in the language of the primary statute. Others have it in subsidiary regulations. Others operate sustainability framing through administrative pre-approval lists or allocation decisions. A few establish a statutory route for capital with a developmental purpose without using sustainability language at all. The strength and source of sustainability framing vary considerably across programs that, at first glance, appear to be doing similar things.

Of the twenty-two programs in this sample, around half carry some form of sustainability framing once these distinctions are applied carefully.

Regional and Structural Patterns

Two programs embed climate or sustainability language directly in the title or stated objective of their primary law: Nauru’s Economic and Climate Resilience Citizenship Act 2024, and St. Kitts and Nevis’s Citizenship by Investment Unit Act 2024 read together with the Citizenship by Substantial Investment Regulations No. 26 of 2023. Several others channel capital into government funds with broad statutory purposes that are then deployed against climate and developmental priorities through policy and allocation decisions. Portugal and New Zealand sit at the intersection of investment migration and regulated sustainable finance. Panama’s Reforestation Visa stands apart as a program where the underlying investment is environmental by statute, predating the entire ESG label by decades.

Regionally, the strongest concentration of sustainability framing is in the Small Island Developing States. The Caribbean programs generally fall under the sustainability-framed cluster (four with stated framing, one without). Nauru in the Pacific and São Tomé and Príncipe in the Atlantic extend the SIDS pattern across the Caribbean, Pacific, and Atlantic.

Europe shows a slower convergence driven by EU-wide sustainable finance regulation rather than by program-level design. Portugal’s Golden Visa fund route operates within the SFDR perimeter without sustainability being a Golden Visa eligibility requirement. Italy, Hungary, and Greece carry implicit framing through specific qualifying routes (philanthropic donations, university donations, startup investment) rather than through statutory sustainability mandates. Cyprus and Latvia, both inside the EU’s regulatory perimeter, have not yet translated that proximity into sustainability framing within their investment migration architecture.

Outside SIDS and Europe, the picture is uneven. Panama stands as Latin America’s longest-established environmentally framed RBI, operating under Law 24 of 1992. New Zealand represents the only high-income Anglosphere program with administrative pre-approval of climate-impact funds. Some Gulf programs (UAE), the higher-income Asian programs (Singapore), and the high-threshold North American program (US Gold Card) operate outside the sustainability cluster, structured as financial, talent, mobility, or fiscal-revenue instruments. Turkey, Egypt, and Jordan, the three Middle East and North Africa programs in the sample, are similarly outside the sustainability framing pattern.

Strongest statutory sustainability anchoring. In the examined countries, Nauru’s ECRCP stands out for embedding climate resilience in the title and stated objective of the establishing Act (Act No. 15/2024). St. Kitts and Nevis stands out for having structured its primary contribution mechanism, the Sustainable Island State Contribution, as a statutorily named instrument under Act 11/2024 with the seven pillars elaborated in subsidiary regulations.

Strongest convergence with regulated sustainable finance. Portugal’s Golden Visa fund route is the clearest case in the examined sample of an investment migration program operating within the European SFDR regulatory perimeter, even though SFDR classification is not a Golden Visa eligibility requirement. New Zealand’s Active Investor Plus Visa is the clearest example in this analysis of a high-income Anglosphere program that pre-approves dedicated climate-impact venture capital funds, though this is by Invest NZ administrative decision rather than statutory mandate.

Strongest explicit social development link. Antigua and Barbuda’s UWI Fund channels capital directly into regional higher education with a one-year tuition scholarship at the University of the West Indies, making it the most structurally explicit social-development route in the Caribbean sample. Hungary’s university donation route operates similarly, channeling capital to public-interest higher-education foundations.

Strongest historical environmental design. Panama’s Reforestation Visa, operating under Law 24 of 1992, is the longest-established environmentally-framed residency-by-investment program in this analysis. The investment itself is environmental by statute: capital is required to be deployed in MiAmbiente-approved tropical reforestation projects. It is a useful reminder that sustainability framing in investment migration is not a recent phenomenon and has been operationally tested for over thirty years.

Most recently designed sustainability frameworks. São Tomé and Príncipe’s National Transformation Fund, launched in August 2025 under Decreto-Lei n.º 07/2025, prioritizes renewable energy in its initial allocation focus and represents the newest entrant to the sustainability-framed cluster in this analysis. Nauru’s ECRCP, launched at COP29 in November 2024, was the first CBI program in this sample to be explicitly designed and marketed from inception as a climate-finance instrument.

Five years ago, sustainability claims in citizenship and residency programs were largely rhetorical. Today, in this sample, climate or sustainability language appears in the title or stated objective of two programs’ primary law, in the structural design of several development funds, in the regulatory regime that overlays at least two programs’ fund routes, and in the administrative pre-approval criteria of one. The structural foundation for sustainable citizenship is in place, but it does not yet exist as a single, uniform standard.

Across regions, the underlying logic of the shift is consistent. Caribbean sovereign funds and European regulated private funds operate through entirely different mechanisms, but both channel qualifying capital into vehicles where the use is traceable and the alignment with developmental or sustainability outcomes is, at minimum, disclosable. The Caribbean works through statute, Europe through regulation.

The sector is in the middle of a real but uneven transition. Sustainability framing exists in roughly half of the active market, with significant variation in how robust the framing is. Some are in primary law, some in subsidiary regulations, some in administrative pre-approval, and some in allocation practice. Outcome reporting and impact measurement remain underdeveloped. SFDR classification depends on fund-manager self-designation rather than regulator certification. The Caribbean programs await the operational rollout of ECCIRA in 2026 before achieving harmonized regulatory oversight. None of this undermines the direction of travel, but it does temper claims about how complete the transition is.

Across the Caribbean, Europe, and the Pacific, programs have been redesigned around a common logic: qualifying capital should be traceable, productive, and tied to a national priority. The mechanism differs – sovereign statute in the Caribbean, regulatory frameworks and fund architecture in Europe. However, the direction is the same. Investor demand reinforces this shift, with younger and high-net-worth investors increasingly allocating capital toward sustainability-aligned vehicles. The sector is responding.

This reorientation carries real fiscal weight. Where multilateral climate finance has consistently fallen short for Small Island Developing States, CBI revenue has emerged as a parallel channel for the same outcomes the SDG framework was built to deliver. For economies like Dominica and St. Kitts and Nevis, it is the fiscal capacity that turns adaptation plans into a funded reality.

Thus, sustainable citizenship emerges as an analytically distinct category, defined by a deliberate and traceable link between the investment route and a recognized sustainability outcome that is supported by statute, regulation, or fund classification in a meaningful share of the active market. The evidence points to a sector in transition. Sustainability framing has moved from the periphery to the mainstream of program design, but the transition is incomplete, and the active market still reflects both directions.

References

Diário da República. (2023, October 6). Lei n.º 56/2023: Mais Habitação. Diário da República, 1.ª série, n.º 194. https://diariodarepublica.pt/dr/detalhe/lei/-222477692-222515894

European Parliament and Council of the European Union. (2019, November 27). Regulation (EU) 2019/2088 of the European Parliament and of the Council on sustainability-related disclosures in the financial services sector. Official Journal of the European Union L 317. https://eur-lex.europa.eu/eli/reg/2019/2088/oj/eng

Global Impact Investing Network. (2024). Sizing the impact investing market 2024. https://thegiin.org/publication/research/sizing-the-impact-investing-market-2024/

Global Impact Investing Network. (2024). What you need to know about impact investing. https://thegiin.org/publication/post/about-impact-investing/

Grantham Research Institute on Climate Change and the Environment. (2024). Small island developing states need innovative forms of finance to bridge the devastating adaptation gap. London School of Economics and Political Science. https://www.lse.ac.uk/granthaminstitute/news/small-island-developing-states-need-innovative-forms-of-finance-to-bridge-the-devastating-adaptation-gap/

International Monetary Fund. (2024, June 27). IMF Executive Board concludes 2024 Article IV consultation with Dominica (Press Release No. 24/247). https://www.imf.org/en/news/articles/2024/06/27/pr-24247-dominica-imf-executive-board-concludes-2024-article-iv-consultation

International Monetary Fund. (2025, May 12). IMF Executive Board concludes 2025 Article IV consultation with St. Kitts and Nevis (Press Release No. 25/139). https://www.imf.org/en/news/articles/2025/05/12/pr-25139-st-kitts-and-nevis-imf-executive-board-concludes-2025-article-iv-consultation

Kochenov, D. (2019). Citizenship. MIT Press. https://mitpress.mit.edu/9780262537797/citizenship/

Kochenov, D. (2023). Victims of citizenship: Feudal statuses for sale in the hypocrisy republic. In D. Kochenov & K. Surak (Eds.), Citizenship and residence sales: Rethinking the boundaries of belonging (pp. 27–48). Cambridge University Press.

L’Ecuyer, B. (2024). Reimagining investment migration: Redefining narratives and remodelling pathways. Investment Migration Council. https://investmentmigration.org/articles/reimagining-investment-migration-redefining-narratives-and-remodelling-pathways/

Morgan Stanley Institute for Sustainable Investing. (2025). Sustainable signals: Individual investors 2025. Morgan Stanley. https://www.morganstanley.com/content/dam/msdotcom/en/assets/pdfs/2025_Sustainable_Signals_Individual_Investors_2025_report.pdf

Sciarelli, M., Cosimato, S., Landi, G., & Iandolo, F. (2021). Socially responsible investment strategies for the transition towards sustainable development: The importance of integrating and communicating ESG. The TQM Journal, 33(7), 39–56. https://doi.org/10.1108/TQM-08-2020-0180

Shachar, A. (2009). The birthright lottery: Citizenship and global inequality. Harvard University Press.

Standard Chartered. (2025). Sustainable Banking Report 2025: Transition investing — the next wealth frontier? Standard Chartered.

Standard Chartered Private Bank. (2019). Affordable and clean energy tops list of Sustainable Development Goals supported by wealthy investors. https://www.sc.com/en/press-release/affordable-and-clean-energy-tops-list-of-sustainable-development-goals-supported-by-wealthy-investors/

Stern, J. (2012). Ius pecuniae – Staatsbürgerschaft zwischen ausreichendem Lebensunterhalt, Mindestsicherung und Menschenwürde. In J. Dahlvik, H. Fassmann, & W. Sievers (Eds.), Migration und Integration: Wissenschaftliche Perspektiven aus Österreich (pp. 55–74). Vienna University Press.

Surak, K. (2016). Global citizenship 2.0: The growth of citizenship by investment programs (IMC Research Paper 2016/3). Investment Migration Council. https://investmentmigration.org/wp-content/uploads/2020/10/Surak-IMC-RP3-2016.pdf

UNCTAD. (2024). Climate finance for SIDS is shockingly low: Why this needs to change. United Nations Conference on Trade and Development. https://unctad.org/news/blog-climate-finance-sids-shockingly-low-why-needs-change

US SIF Foundation. (2025). Trends report 2025/2026. US SIF: The Sustainable Investment Forum. https://www.ussif.org/research/trends-reports/us-sustainable-investing-trends-2025-2026-executive-summary

World Commission on Environment and Development. (1987). Our common future. Oxford University Press. https://sustainabledevelopment.un.org/content/documents/5987our-common-future.pdf